Two scenarios, both painful. How will the war in the Middle East hit the economy and markets

Even in the optimistic, base scenario presented by UniCredit bank analysts – assuming the end of the conflict in the Middle East at the beginning of the third quarter – the Old Continent will face an economic slowdown and a return to interest rate increases by the ECB. However, if military operations in Iran drag on for another few months, oil and gas prices may soar by several dozen percent. In this variant, the impact on economies, as well as on the wallets of consumers and investors, will be more severe.

The short military intervention that Donald Trump initially counted on turned into a conflict lasting for a fifth week. Its most serious consequence for the global economy remains the blockade of the Strait of Hormuz – a strategic route through which approximately 15 million barrels of crude oil per day (34% of global sea trade) and nearly 20% of global LNG supplies flowed until recently.

Economists and analysts The Investment Institute from the UniCredit group, one of the largest banks in Europe, presented updated macroeconomic forecasts in which they outline two paths for the development of the situation. The difference is the scale of the devastation that oil and gas prices will wreak on the global, and especially European, economy.

Who will decide about the end of the war?

The starting point for forecasts is the duration of the armed intervention in Iran and the blockade of the Strait of Hormuz. In the base scenario, analysts assume that the armed conflict will end in the summer of this year. This will allow for a slow normalization of oil flows and a gradual decline in oil prices, although a return to pre-war price lists is excluded.

The shock scenario assumes a prolonged war and long-term disruptions in supply chains, which will push up the prices of raw materials. As experts point out, the geopolitical switch for this conflict is not in Washington.

– We expect that China will ultimately put pressure on Iran to stop its actions at the right time. Beijing is extremely sensitive to supply disruptions through the Strait of Hormuz, and Tehran remains largely dependent on China for key imports, he explains. Edoardo Campanella, director and editor-in-chief of The Investment Institute at UniCredit.

Today, the war favors China's interests while weakening the position of the United States. However, the Middle Kingdom's own energy resources are limited and will be enough to survive the blockade of the Strait of Hormuz for about five months, and over time it will have to actively engage in unblocking the flows. It is worth adding that as much as 90% of the oil transported through the strait went to Asia, while exports to Europe accounted for about 4%.

Even if the above-mentioned scenario materializes, the question remains who will secure transports through the Strait of Hormuz after the war. One of the real options is to establish an international coalition for this purpose, which, however, will be a diplomatic challenge and may maintain nervousness.

Oil and gas prices will be scary. Risk premium

The effects of military operations are visible primarily on commodity exchanges. According to UniCredit analysts, we must accept that the era of cheap energy raw materials will not return soon.

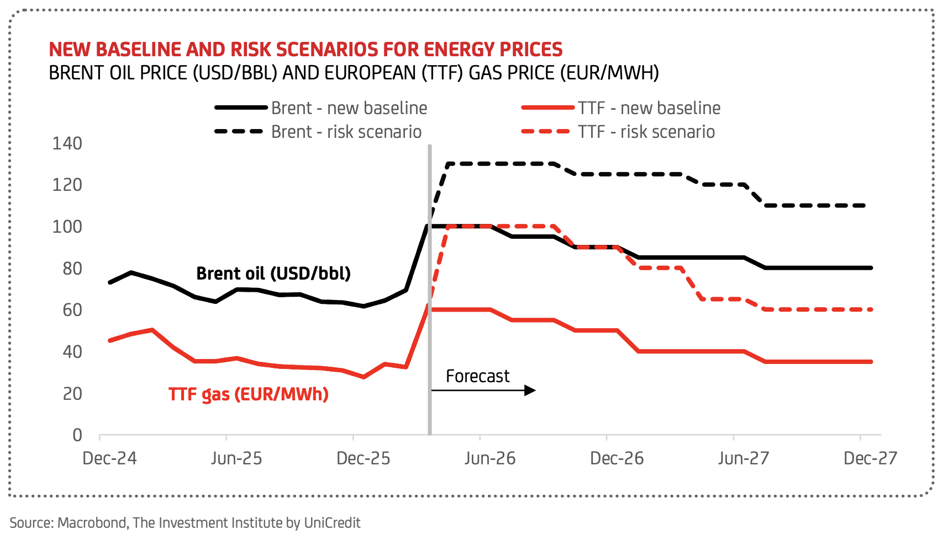

– In our baseline scenario, we expect Brent oil prices to remain close to $100 per barrel until the end of the second quarter, followed by a slow normalization. In the case of European TTF gas, we expect a price of approximately EUR 60/MWh. However, if a higher risk scenario materializes and the conflict drags on into the third quarter, oil prices may soar up to USD 130 and gas up to EUR 100/MWh – he predicts. Thomas Strobel, investment strategist of the Munich branch of UniCredit.

As he points out, the continuing uncertainty in the markets excludes oil from returning to levels of $60-65 in the near future. The baseline scenario assumes a drop in Brent oil prices to USD 90 at the end of the year and TTF gas prices to EUR 40/MWh.

The US caused the conflict, but it will hurt Europe more

Analysts emphasize that the United States, as a net energy exporter, has adequate buffers to absorb price increases. The situation in the euro zone, including Germany and Italy, which are heavily dependent on hydrocarbon imports, is much more difficult.

– This conflict will hit Europe harder, generating a much more lasting price shock than we previously expected. We expect inflation in the euro area to rise again this year to around 3% and return to target only in the second half of 2027. Higher energy costs will hit consumers' purchasing power and reduce companies' margins, he says Loredana Maria Federico, Chief Economist of UniCredit in Italy.

Such a scenario will translate into the policy of central banks. While the US Fed may ignore the inflationary impulse and still plan to cut rates at the end of the year (as the Trump administration will push ahead of the midterm elections), the European Central Bank has no such comfort. Experts forecast that in order to prevent inflation expectations from de-anchoring, the ECB will be forced to raise interest rates twice (25 basis points each), probably in June and September, after which the main rate may reach 2.5%.

This will cool Europe's already sluggish economic growth. It is forecast to amount to 0.8% this year in the euro zone, 0.9% in Germany and only 0.5% in Italy.

And all this assuming a favorable scenario, because if the war continues, the ECB will have to act more decisively (rates may reach 3-3.25%), while growth in the euro zone may amount to a measly 0.5%.

For comparison, US GDP growth this year is estimated by UniCredit at 2.3%, and in the case of an unfavorable scenario at a still very solid 2%.

What about Poland? GDP forecasts are down and the budget is worrying

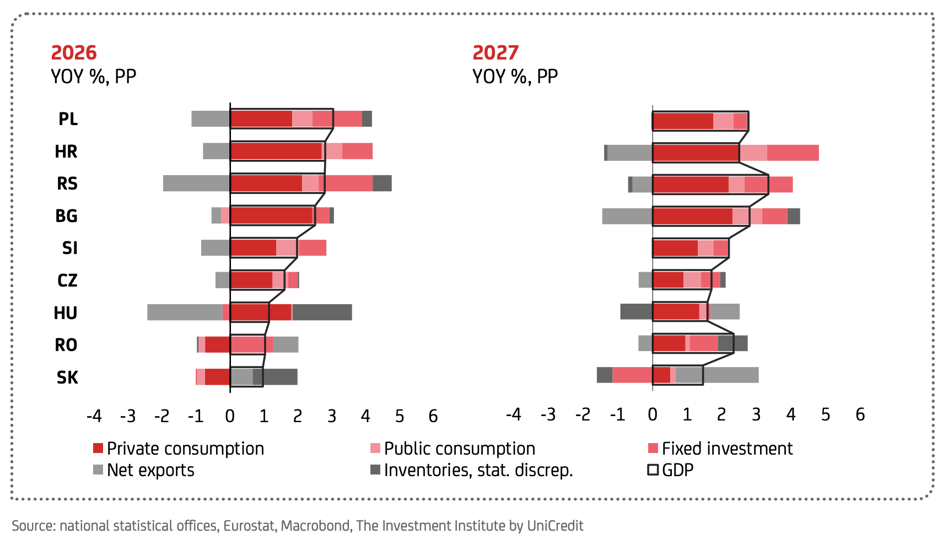

The conflict is hitting the countries of Central and Eastern Europe hard, most of which have an energy mix very much based on imported raw materials – the dependence often reaches 90-95%. Even though governments have implemented various types of protective mechanisms and shields, the costs still ultimately burden the economy.

– Governments are trying to cover some of the costs, but with current deficits reaching around 6% of GDP in Poland, Hungary and Romania, fiscal space is very limited. We revised down our growth forecasts for the region by an average of 0.3 to 0.6 points. percent for this year. The outlook for interest rates is also changing. We expect that the National Bank of Poland will keep rates at 3.75% until the second half of next year. Only then may there be room to resume policy easing, he points out Eszter Gargyan, market expert in our region from UniCredit in Munich.

UniCredit economists expect that our country's GDP will grow by 3% this year (compared to 3.6% last year). At the same time, inflation will accelerate to 3.2% (from 2.4%). The Achilles heel of the Polish economy remains the state of public finances. Although the cash gap is expected to shrink slightly (from 6.9% to 6.5% of GDP), this result will most likely ensure us the inglorious position of debt leader in the entire Central and Eastern Europe.

As analysts warn, in the case of a worst-case scenario, the space for introducing further economic protection packages is already exhausted. For countries with the highest deficits – such as Poland, Romania, Hungary and Slovakia – rising energy costs and weakening growth carry increasing risks for the budget and, consequently, a real threat of downgrades in credit ratings.

The dollar is still outclassed, gold is waiting for better times

On the wave of market anxiety, capital traditionally looks for safe havens. The US dollar is the winner again which, in conditions of strong risk aversion, is clearly gaining not only against the euro, but also, among others, yen or franc.

– If the escalation of the war continues, risk aversion will intensify and the EUR/USD rate may fall even below 1.10. However, if our base scenario comes true and the situation slowly begins to calm down in the summer, the euro has a chance to make up for the losses and approach 1.20 – says Roberto Mialich, currency market strategist at UniCredit.

Gold looks interesting against this background. The price of the precious metal dropped to around $4,500 per ounce, and according to analysts, investors fled the market due to a sharp change in expectations regarding the level of interest rates in the US (the attractiveness of interest-generating instruments increased) and the strengthening of the dollar.

However, the short-term shortness of breath does not rule out further prospects for the precious metal. Demand is still supported by central bank purchases and general global geopolitical uncertainty. According to UniCredit analysts, this year gold prices will stabilize in a wide range from $4,400 to $5,100 per ounce, and next year the upper limit of fluctuations may even move to $5,300-5,500.

Will there be a tailwind for stocks again?

How will stock markets cope in this turbulent environment? Despite the geopolitical shocks, the base scenario of the Italian giant's experts assumes the surprising resilience of parquet floors. Stock markets in the US and Europe show signs of stabilization at current levels, and investors – looking ahead and discounting better prospects for 2027 – can count on the return of market “tailwinds”.

Interestingly, analysts see the greatest potential for a strong rebound not on mature markets, but on emerging markets. As Roberto Mialich points out, it is in this segment that it is currently worth increasing the portfolio's exposure. These markets are supported by both continued global demand for raw materials and a structural shift towards companies benefiting from the AI revolution.

UniCredit experts assumed that the variant of a prolonged war may mean a regression for the stock exchanges to the levels at the end of the third quarter of 2025. The only safe haven for the fleeing capital will then be companies from the energy sector and traditional defensive industries.