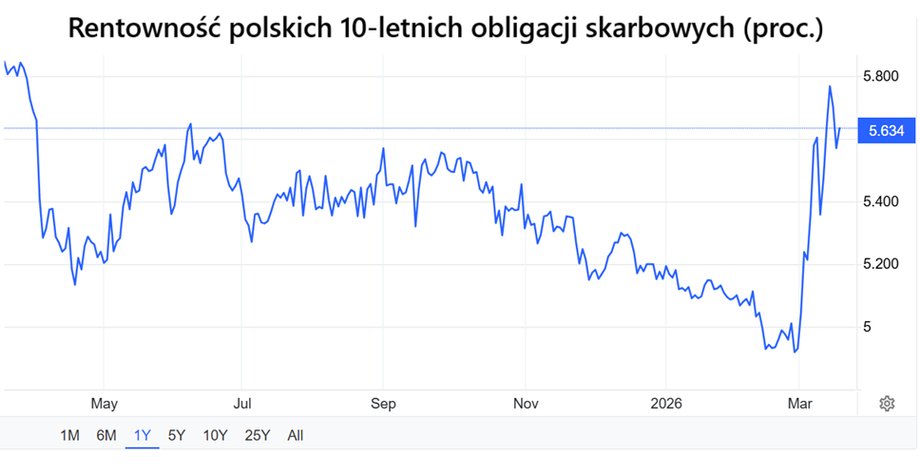

After the attack on Iran, the yield on Polish 10-year treasury bonds increased significantly and temporarily reached as much as 5.92 percent, which is the level – despite interest rate cuts by 2 percentage points. made by the Monetary Policy Council at that time – not seen for a year. Profitability increased at an extraordinary pace for several days, by almost 1 percentage point. Typically, changes of this scale take at least a few months. In recent days, this movement has corrected slightly, but the yield on our 10-year treasury securities is still elevated and on Wednesday it fluctuated around 5.66%.

An increase in yield means a decrease in the price of bonds. Although the vast majority (about 70% in the case of PLN issues) of our “treasury bonds” have a fixed interest rate, the increase in market profitability is bad news for the Ministry of Finance, because the sale of new series to investors – and these are regularly carried out two or three times a month – will be carried out with a higher coupon, which means it will be more expensive for the state. You can also look at it differently: a decline in bond prices means that to achieve the same goals, the Ministry of Finance must issue more securities.

The rest of the text below the video:

Finance Minister Andrzej Domański reassured that the yields on treasury bonds are rising in many Western and Central and Eastern European countries, and Poland is no exception, Domański said at a press conference. As he noted, this phenomenon is related to, among others, with the geopolitical situation in the Middle East and the emerging inflationary pressure resulting from the increase in oil prices. Markets are pricing in the possibility of central banks increasing interest rates if the conflict and disruptions in oil supplies are prolonged. However, Andrzej Domański emphasized that the situation of the state budget is stable and it is well prepared. However, we must remember about the significant challenge of the scale of this year's borrowing needs (PLN 423 billion net and PLN 688 billion gross).

See also: The war in Iran and Polish wallets. Economists predict a second-round effect

Piotr Arak, chief economist at VeloBank, points out that the reaction of Polish bond yields after the attack on Iran is very similar to the one we observed in the first phase of the shock after the outbreak of the war in Ukraine in 2022, although the scale is clearly smaller.

— Then the region's risk premium, measured by the increase in the spread to German Bunds, increased by 2-3 percentage points, and the pure geopolitical premium itself was estimated at approximately 0.5-1.5 percentage points. Currently, we are dealing with a movement of several dozen basis points, i.e. a classic risk-off episode, rather than a permanent overestimation of Poland's risk. – he points out.

Bartosz Sawicki, an analyst at Exante, speaks in a similar tone. – The impact of the supply shock on individual economies varies, but it is undoubtedly a global problem – says the expert, noting that this year's borrowing needs are already covered in less than 40 percent.

He emphasizes, however, that if the observed increase in yield – amounting to almost 0.70 percentage points in the case of 10-year bonds from the moment the conflict broke out – will prove to be permanent, which will translate into higher debt servicing costs.

This may make servicing Polish debt more expensive

Although last week the Ministry of Finance decided to cancel the bond swap auction, there was no change in plans on Wednesday and the transaction was completed: the Ministry of Finance sold bonds for PLN 9.48 billion at the swap auction (this is a result close to the average sale from the swap auction in 2025), and bought them back for PLN 9.17 billion with demand reaching PLN 13.7 billion.

The yield on Polish treasury bonds increased significantly despite interest rate cuts.

|

tradingeconomics

— The outbreak of the conflict in the Middle East will have a limited impact on Poland's public finances, assuming that de-escalation will occur within a few weeks. If the war had dragged on for the following months, his importance for the country would have increased noticeably. In both cases, however, the Ministry of Finance will have no reason to worry. Taking into account the record issues of treasury securities in January and February, canceling one or even several tenders does not have much significance from the point of view of meeting this year's borrowing needs – says Mirosław Budzicki, financial market strategist from the Market Strategies Office of PKO BP.

He reminds that the Ministry of Finance has a high liquidity cushion exceeding PLN 170 billion, which can be used in such an unstable situation. — For now, we do not observe any serious problems on the primary market. The result of Wednesday's change auction confirmed solid demand for Polish wholesale bonds. Although we are talking about a sharp increase in profitability, their impact on the cost of Poland's debt servicing will be moderate, I estimate it at PLN 0.3 billion in 2026. If the conflict lasted longer than a month, the state's burdens would increase, although still on a small scale – indicates the PKO BP strategist.

See also: The war changes economic forecasts. Economists warn

The increase in debt servicing costs would be a gradual and spread over time process. The government pays higher interest rates only on newly issued bonds, and the average cost of debt increases gradually as maturing securities are refinanced. New securities, issued with a higher coupon, would slowly enter the pool of debt, which amounts to approximately PLN 760 billion due to treasury bonds. The problem would be more acute if the increased yields on listed bonds lasted longer.

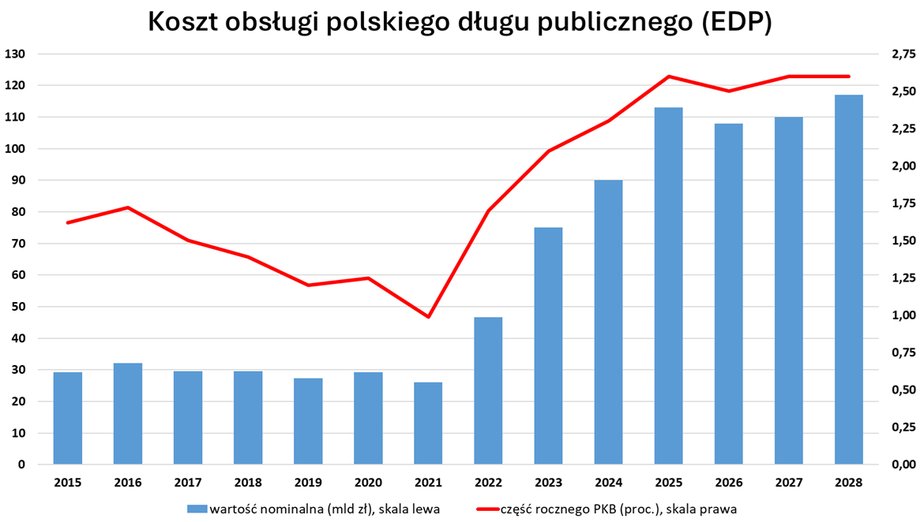

If we adopt a more pessimistic variant, in which the Ministry of Finance would have to issue treasury securities for half a year at a yield of around 5.9%, i.e. 1 percentage point. higher than at the end of February (just before the attack on Iran) and if PLN 15 billion of fixed-rate debt were placed monthly (PLN 90 billion in total), the additional cost would be approximately PLN 900 million annually until maturity. This is relatively little, for comparison, the total debt servicing costs of the public finance sector amounted to approximately PLN 113 billion (2.5% of GDP) in 2025.

In 2025-2026, the total cost of servicing the debt of the general government sector (EDP) may amount to approximately PLN 115 billion (2.5% of GDP).

|

Ministry of Finance, own calculations and estimates

— We do not know whether the next auction on March 25 will actually take place, because the switch auction is smaller than the new bond issue, the main barrier is the additional premium that the market can now expect in relation to what the State Treasury is willing to pay. It seems to me that the market today is simply afraid of inflation and interest rate increases and that is why it sees yields higher than before, says Piotr Arak.

He adds that the only real cause for concern would be if energy prices remain high, which would raise inflation and interest rates.. — The market is pricing it in today, but this is the most likely scenario wait and see for several months and a return to reductions by the National Bank of Poland – says a VeloBank economist.

The turmoil on the markets is not only about more expensive debt

Rising oil prices may spill over into the prices of other goods and services, causing the so-called second round effect. The years 2022-2023 remind us that this type of events do not go unnoticed by the authorities, who use protective tools. However, the impact on the budget would be multidimensional.

— The increase in oil and gas prices affects public finances in two ways. In the short term, higher inflation increases nominal tax revenues from VAT and excise duty, and indirectly also from PIT and CIT. In the first phase, it may even improve the budget balance. At the same time, however, more expensive energy creates political pressure to introduce protective mechanisms, such as bill subsidies or freezing prices, which significantly burdened public finances in 2022-2023, emphasizes Piotr Arak.

The longer energy prices remain elevated, the greater the chance of interest rate increases (although economists do not expect such a move for now), the slower economic growth and lower tax revenues.

— At this stage, the final impact of the conflict on the fiscal situation cannot yet be reliably assessed. Possible government protective measures, such as a temporary reduction in VAT or excise duty on fuels, remain very important in the context of the stability of public finances. – says Bartosz Sawicki from Exante.

Slightly slower economic growth resulting from higher oil prices and higher inflation (may inhibit consumption dynamics) would reduce budget revenues, e.g. from corporate taxes.

— On the other hand, the pro-inflationary impact of rising prices of energy raw materials would support consumption-related income by approximately PLN 0.5-1 billion. Without taking into account protective shields, the impact of the situation in the Middle East will be limited for public finances in Poland. However, the importance of this factor may increase non-linearly if the conflict lasts longer – summarizes Mirosław Budzicki. In addition – in conditions of increased inflation – there would be a decline in the real value of debt.

— The confusion over SAFE, increases in yields and Poland's huge borrowing needs do not escape the attention of rating agencies and Friday's decision by Moody's will certainly indicate a number of risks for Poland and maintaining a negative outlook for the Polish debt, which will not help yields – says Piotr Arak.

Author: Maciej Rudke, journalist of Business Insider Polska