The US-Israeli attack on Iran at the beginning of the weekend started a wider war conflict in the Middle East. mBank economists note that compared to the Midnight Hammer strike of June 2025. the scale and determination of the US, Israel and Iran are much greater today.

“The elimination of Ali Khamenei acts as a double-edged sword. In the short term drastically worsens stabilitybecause it disperses the decision-making process in Tehran between military factions. It also strengthens the IRGC's chaotic, yet powerful, retaliatory strikes,” mBank experts point out.

The rest of the article is below the video

See also: Not just oil. Business holds its breath after the US attack on Iran. These are three key questions [ANALIZA]

They add that in the long run this gives a chance to break up the structure of the “Axis of Resistance”. They estimate that the chance for society to take power is the highest in the history of the Islamic Republic, but carries the risk of a bloody civil war.

Strait of Hormuz closed? Options to bypass the lock are limited

They pose a key question for the global economy: Is the Strait of Hormuz closed or open? They indicate that as of March 2, 2026 we are dealing with “hybrid lock“, not a classic, physical blockade, although the economic consequences are almost identical. Iran has declared its territorial waters a “war zone”, threatening attacks on merchant ships. The real force are hidden coastal anti-ship missile launchers and deployed new generation mines. The messages themselves, supported by missile incidents, prompt insurers to withdraw guarantees, which de facto closes the movement without an open clash with the US fleet.

“Options to bypass the lock are limited: the Saudi East-West pipeline transports 5-7 million barrels a day compared to about 20 million normally through Hormuz, and the Emirate route to Fujairah is still a drop in the ocean. A key role is played by China, which is pressing Tehran to loosen the blockade, trying to negotiate safe corridors for its own units,” we read in the analysis by mBank economists.

Other supply chains are also at risk. “He is most immediately at risk LNG from Qatarwhich is responsible for approximately 20 percent. global trade in this raw material, which forces Europe to conduct expensive bidding for cargo from other directions and increases energy costs.

Experts further enumerate that there is a significant impact on the fertilizer market through restrictions on the export of ammonia and urea from the region. “Logistics paralysis in hubs such as Dubai may break the just-in-time chains in the automotive and electronics industries. Shortages of polymers and methanol from Iran affect the chemical industry and the production of packaging and household appliance parts, also in Poland. Key transshipment hubs in the Gulf, such as Jebel Ali, are no longer a breathing space for global logistics because goods inside the Gulf cannot get out. Additionally, insurance rates for the entire region are increasing dramatically,” we read.

How does the war in the Middle East affect Poland?

Currency rates are stable, the stock market opened with declines, although there is no great panic. “This is a conflict that affects Poland mainly through oil prices and other supply chain disruptions” – indicate mBank economists.

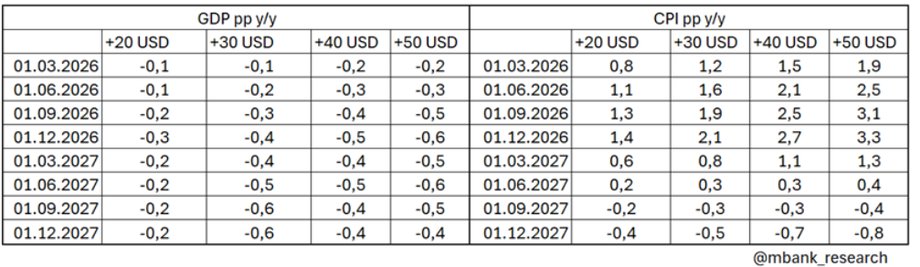

They made calculations according to the Oxford Economics model for various scenarios of oil growth (they consider a permanent increase in oil prices on various scales). From a GDP perspective, this may mean declines of a maximum of 0.6 percentage points.

Worse is the case with inflation, which could increase by as much as about 3 percentage points in the coming months.

|

mBank Research

The impact of the conflict in the Middle East on interest rates

According to economists, the most interesting thing is the impact on the Monetary Policy Council. “The escalation in the Middle East and the situation in the Strait of Hormuz are driving up oil prices, which the MPC will probably treat as a risk factor slowing down the pace of further cuts in the second quarter, but not blocking the March move based on domestic disinflation data. However, there is a (not small) possibility of an emotional reaction according to the simple heuristics offered many times by President Glapiński: “when there is a war, rates are not lowered.” In such a case, an alternative would be to wait for the cessation of hostilities, perhaps e.g. until April,” they comment.