publication

2025-09-17 06:00

In August, consumer bankruptcy was announced by almost 8 percent more natural persons than a year ago. Seasonal acceleration of bankruptcies does not necessarily mean that the annual record of the number of cases will be broken again.

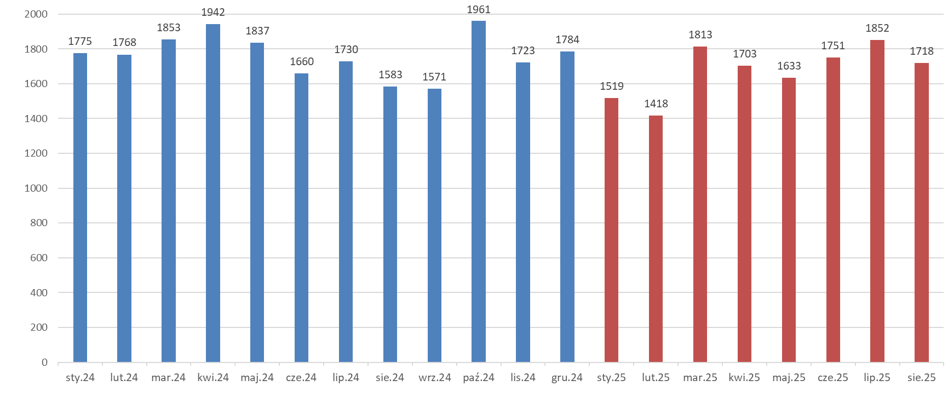

The second half of the year is under the sign of slight acceleration in consumer bankruptcies. In July, we recorded “Skokok” above the average, and the latest August data look similar. According to information collected by the Central Center for Economic Information, it shows that in the second month of holidays 1718 consumers announced bankruptcy. This means an increase of 7.8 percent compared to the same period last year.

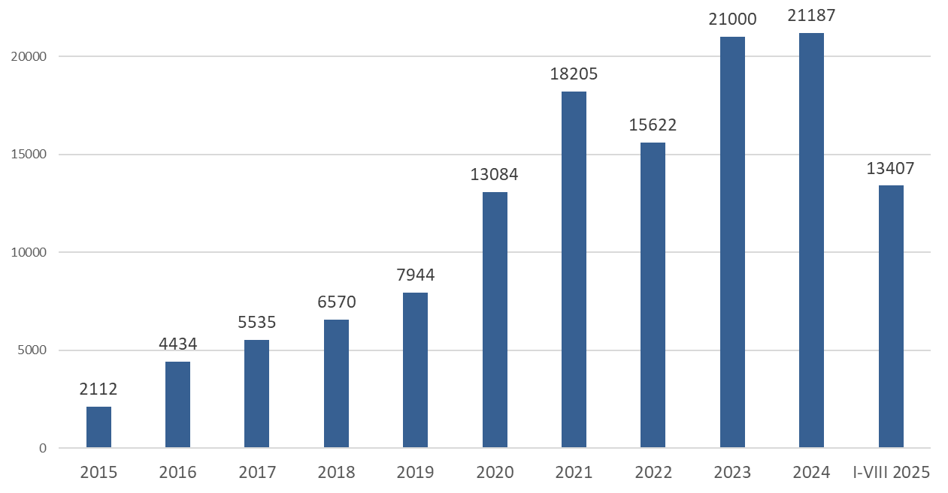

If you assume that the pace of bankruptcy listed in the last 8 months will be maintained, then only small is likely exceeding the border 20 thousand bankruptcies in 2025 This would mean a negative trend that has been going on for over 10 years. So far, it has only happened once that the result from the preceding year has not been beaten. In 2022, such a deviation was the result of changes in the procedure and digitization of the bankruptcy process, which excluded some of the debtors.

“Bankruptcy version 3.5” is coming

In Poland, significant moments for consumer bankruptcy have so far been primarily changes in legal regulations. A significant increase in the number of advertisements occurred in 2020 after the requirements for people applying for bankruptcy occurred. Earlier, people contributing to insolvency due to gross negligence could not use this institution. After legal changes, even deliberately leading to insolvency does not constitute an obstacle, while the degree of the debtor's fault is analyzed at a later stage of the proceedings and affects the terms of the repayment plan.

In July 2025, another change appeared on the horizon in legal regulations affecting falling natural persons. The corrections proposed by the Ministry of Justice mainly concern the increase in process efficiency. For the fallen, it will be important above all:

- Transfer of supervision over the implementation of the repayment plan to creditors. Failure to submit a bankrupt report within the time limit will no longer automatically mean repealing the repayment plan.

- Simplifying the procedure for redemption of liabilities after the repayment plan is carried out.

- Faster removal of information about consumer bankruptcy from the National Register of Debt.

Since a possible amendment does not introduce changes “at the entrance” (e.g. by liberalizing the preliminary requirements to the declaration of bankruptcy), it can be expected that it will not translate into expanding the group of those interested in bankruptcy. However, it is possible to speed up the processes and thus shorten the path from submitting the application to bankruptcy.

Slight deterioration in loan repayment

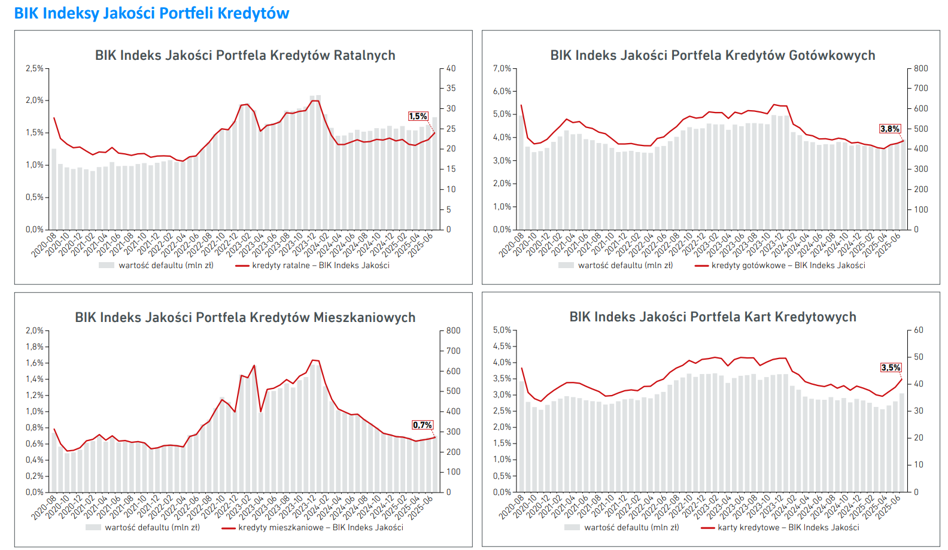

In the first months of 2025, the Credit Information Bureau regularly reported about the improvement quality of banks' credit wallets. This trend has reversed and from May indexes illustrating the timely repayments of individual clients show a slight deterioration.

The last reading of loan portfolio quality indexes includes July data. Compared to month to month, the indicator value for all four products deteriorated: Credit cards O (+0.24), cash loans (+0.11), installment loans (+0.10), housing loans (+0.02). “All four indexes still show a safe level of risk of loan portfolio granted to households. However, it is necessary to constantly observe the values of individual indexes to previously identify signals about the deterioration of the quality of the portfolio,” BIK indicates.

BIK indexes measure the value of loans entering the status of serious (over 90 days) delay in paying repayments. The higher the value, the greater the amount of liabilities changing their state to delayed (the pace of “spoiling” of bank loan wallets). The indicators constructed by the Office can be treated as a pre -overtaking signal of a possible increase in the number of consumer bankruptcy.