The best investment specialists tell you the numbers to budget for in 2026, what the risks are and what you can expect this year

Romania's economy enters 2026 with a rare combination of anemic growth, still high inflation and rising political risk – a cocktail to be managed rather than celebrated. For an investor or an entrepreneur, the message of the CFA Romania survey is clear: 2026 is the year of lucid execution and well-calculated risk appetite.

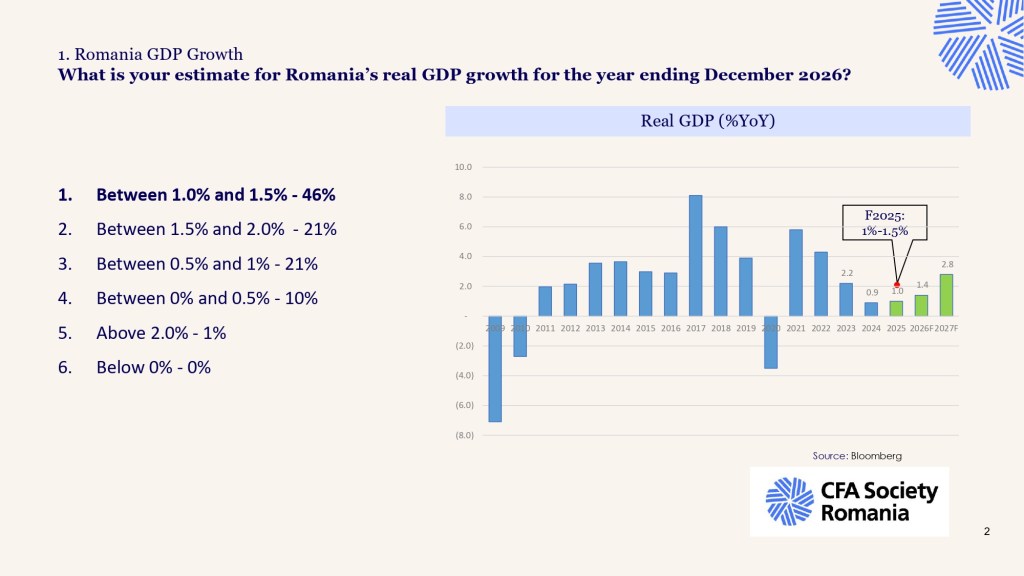

Growth below potential, economy “on the brakes”

Most investment professionals expect real GDP to advance by just 1.0–1.5% in 2026, a growth rate consistent with an economy operating below potential. Practically, Romania remains in the gray area: it avoids recession, but does not generate enough advance to reduce the imbalances accumulated during the years of relaxed fiscal policy.

For corporate budgets, this means a context where turnover is growing from inflation rather than volume, and the difficulty will not necessarily be finding demand, but defending margins. The classic example: consumer goods companies can sell roughly the same quantities, but with higher financing costs and wages.

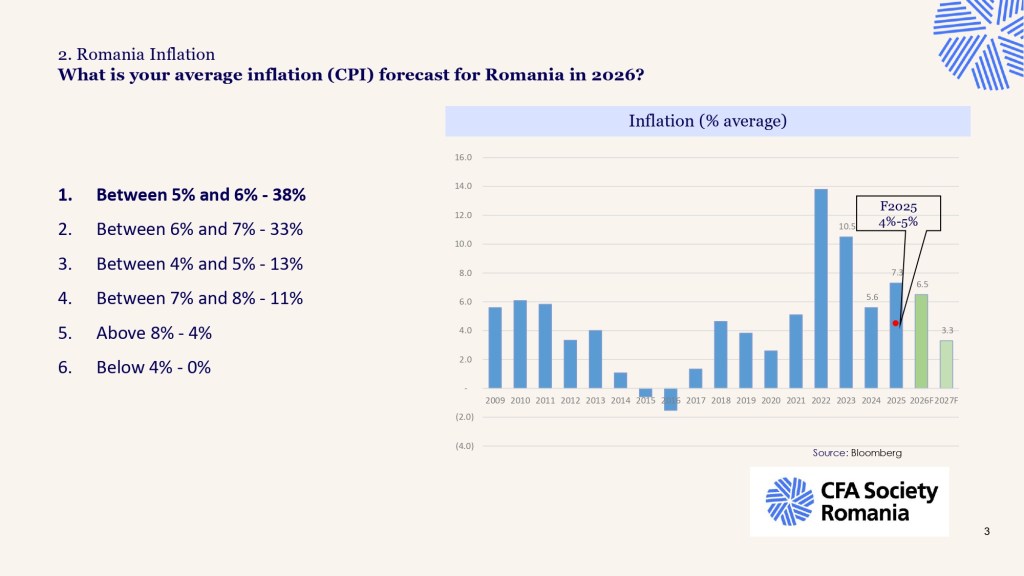

Persistent inflation and a slowly depreciating leu

Expected average inflation for 2026, in the range of 5–6%, indicates incomplete disinflation: the pressure on purchasing power is decreasing from the peak of previous years, but not disappearing. In Romanian, household budgets remain strained: wages must keep up with prices that are still rising significantly above the central bank's target.

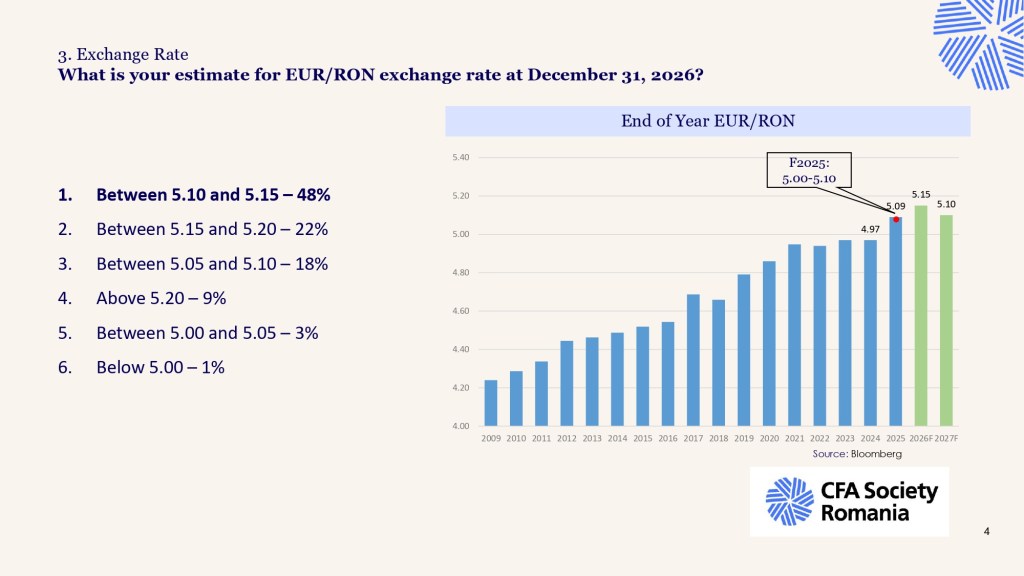

On the course, the consensus is gathering around a EUR/RON of 5.10–5.20 at the end of 2026, i.e. a slow depreciation of the leu, in line with the persistent perception of fiscal risk and modest growth prospects. For companies and investors, the implication is two-fold: foreign exchange earnings gain in nominal terms, and imports and debts in euros gradually become more expensive.

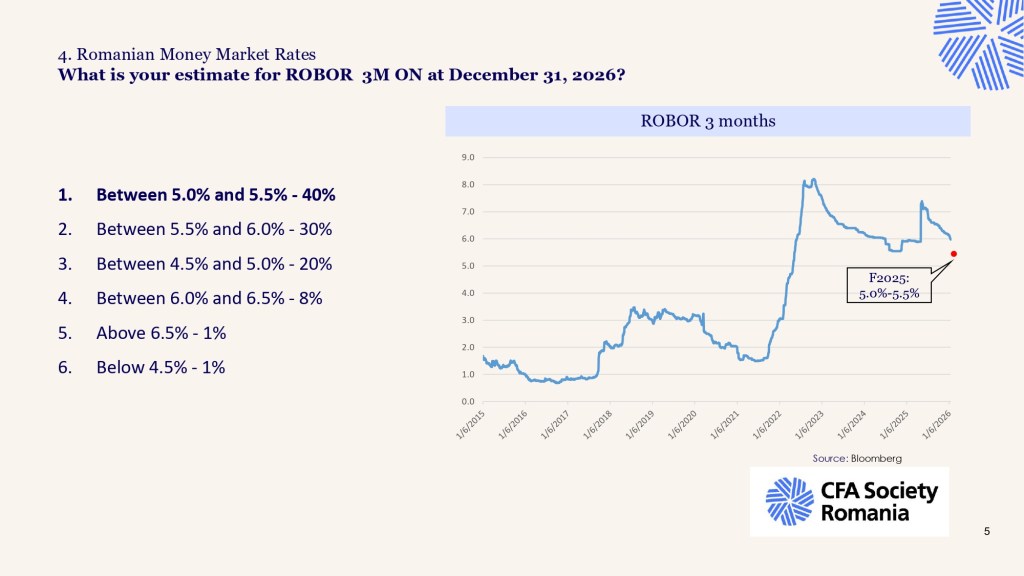

Cost of money: lower but still 'expensive'

The estimate for 3M ROBOR in the 5.0–5.5% area suggests a tight but not suffocating monetary environment, compatible with a central bank caught between the need to anchor inflation and political pressure for easing. The 5-year government bond yields in lei, projected at 6.0–6.5%, confirm the image of a still high risk premium, fueled to a large extent by the budget deficit and public debt dynamics.

For 2026 budgets, the message is simple: funding remains relatively expensive and leverage decisions need to be carefully weighed, especially in cyclical sectors. However, medium-term investors can find in the yield curve in lei an attractive carry opportunity, as long as the sovereign credit risk is perceived as manageable.

The stock market: a bet on normalization

A 10–20% increase in BET-XT for 2026, as a significant portion of respondents anticipate, would mean a good year for equity investors in a merely mediocre macro environment. The FT/WSJ reading of this contrast is intuitive: the market recovers some of the discount applied during years of macro anxiety, banking on investment grade stability and the absence of major domestic shocks.

In such a scenario, investments in Romanian shares become a bet on the resilience of the private sector and on the fact that, despite the political noise, Romania remains anchored in the economic architecture of the EU. For a diversified portfolio, exposure to local equity can work as a regional “beta” with potential return over public debt in lei.

Gold, refuge in a world of overlapping risks

The fact that gold is listed as the asset with the best expected total returns in 2026 is more a diagnosis of systemic anxiety than a simple market call. Against a backdrop of persistent inflation, a slowly depreciating local currency and regional geopolitical uncertainty, the preference for gold signals that investment professionals see 2026 as a year in which capital protection outweighs the aggressive search for yield.

This defensive orientation is consistent with the perceived risk profile: Romania remains an emerging economy exposed to both internal (fiscal, political) and external shocks (proximity war, volatility on global markets).

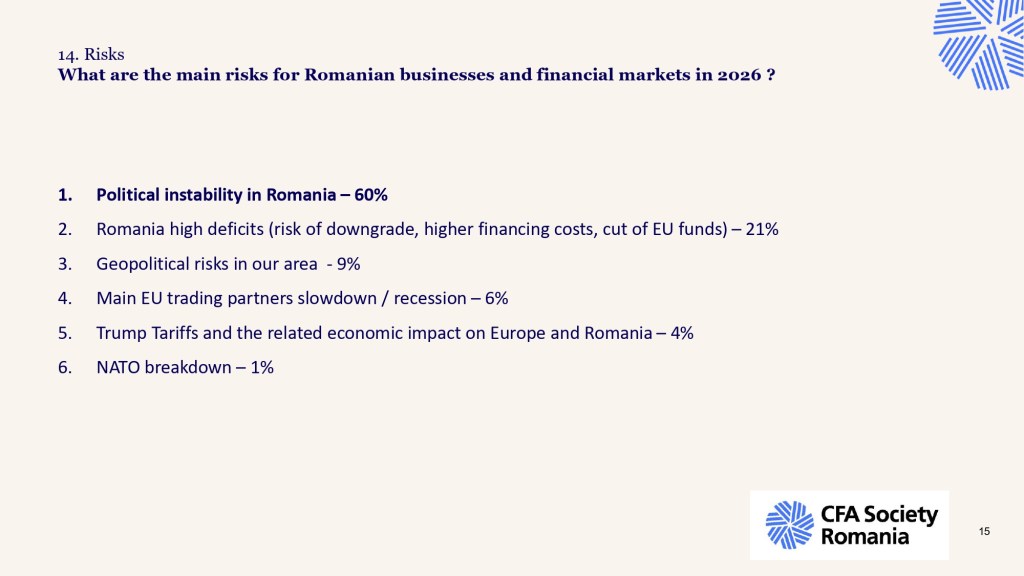

Domestic risks: Politics eclipses the economy

Political instability emerges as the main risk to business and markets in 2026, ahead of purely economic factors. This reflects a context in which fragile coalitions, the temptation of fiscal populism and the extended electoral calendar can delay or dilute any form of fiscal consolidation or structural reform.

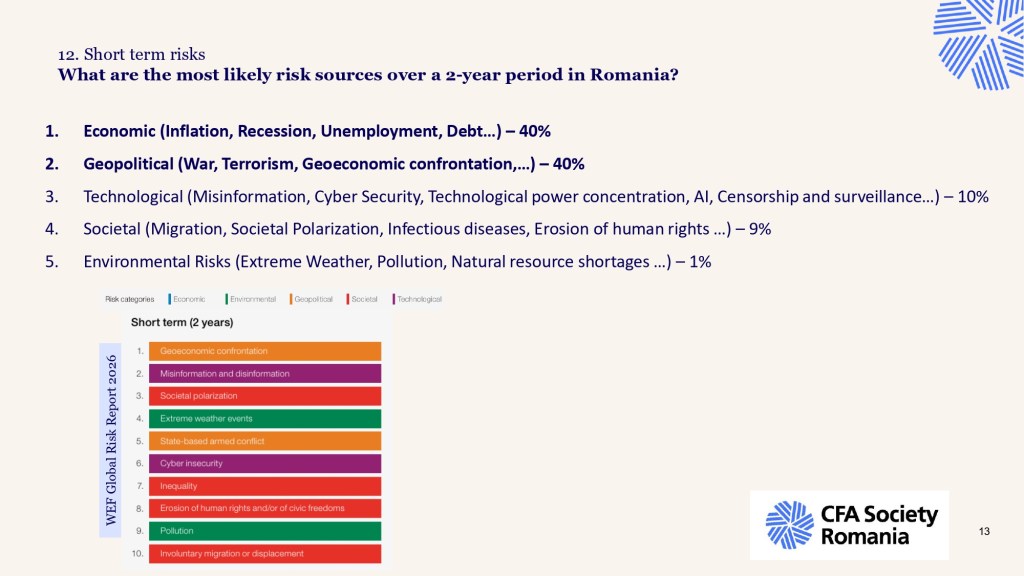

Over a two-year horizon, the respondents divide the risks almost equally between the economic sphere (inflation, recession, unemployment, debt) and the geopolitical one (war, terrorism, geoeconomic confrontation), which places Romania in an area of multiple uncertainty. For the business environment, the consequence is a higher risk premium required for long-term projects and a preference for operational flexibility at the expense of irreversible investments

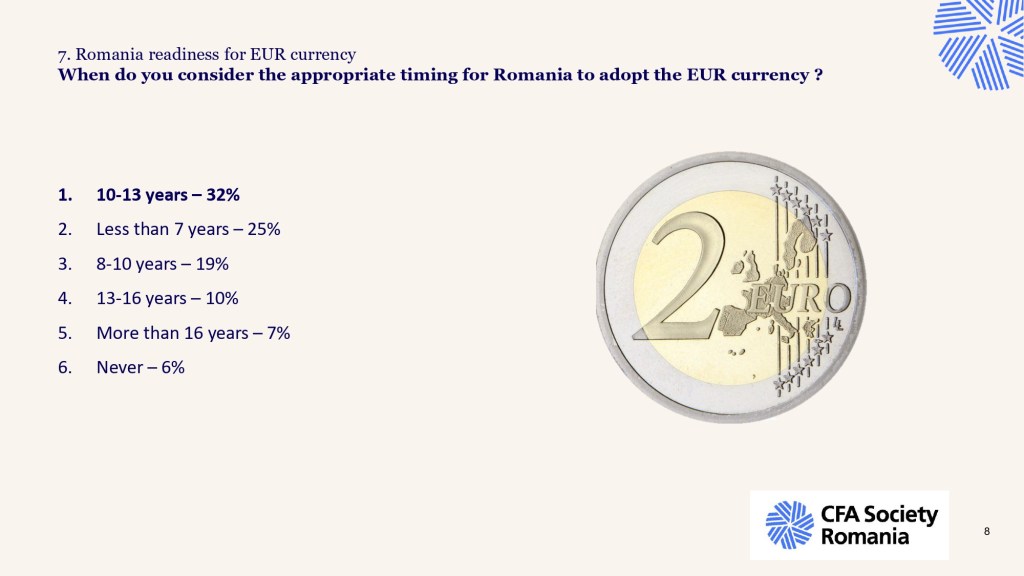

Euro, far away; IA, polarizing

The 10–13 year window indicated for the adoption of the euro is, implicitly, a critical assessment of fiscal discipline and the state's ability to converge to the Maastricht criteria. With high deficits and rising debt, the “euro in the next decade” scenario looks, in The Economist key, more like a statement of intent than a credible plan.stiripesource+3

In parallel, the expectation that artificial intelligence will have an uneven impact by 2030, favoring some groups and disadvantaging others, aligns Romania to the global discussion about technological polarization. For public policy and corporate strategy, the stake is not just AI adoption, but managing the divide between those who can monetize it and those who risk being left behind.

What a “rational” budget looks like for 2026

The cumulative reading of these estimates outlines a set of pragmatic parameters for budgets: modest revenue growth in real terms, inflation of 5–6%, cost of financing still high and a slowly depreciating leu. In such a framework, the firms and households that will perform will not be those that rely on optimistic scenarios, but those that treat these figures as an upper limit of realism, not as a promise.

See here the full results of the CFA Romania survey