The war in the Middle East increases inflation in Poland. Loan installments may increase

Initially, financial markets appeared to overreact to the war in Iran and the blockade of the Strait of Hormuz, which drove up the prices of oil, gas and some other commodities. This reaction was visible in the change in expectations regarding interest rates: previous hopes for cuts were replaced by concerns about increases.

The war continues and it is difficult to predict its end, so the market pressure does not let up. Although no increase in interest rates is expected yet at the meeting of the Monetary Policy Council, which began on Monday, analysts' forecasts for this year are clearly disturbing.

Read also in BUSINESS INSIDER

Inflation is already rising. “Legitimate concerns”

Despite the introduction of the government program Fuel Prices Lower, inflation in Poland is rising. In April, the CPI rose to 3.2 percent. year on year, although in May – according to preliminary data – it surprised positively and decreased to 3.1 percent. (3.7% was forecast, which would mean that it again exceeds the upper limit of the NBP target: the range is 1.5-3.5%). After the May reading, some economists began to soften their message regarding inflation and interest rate forecasts; the statements in this text were collected before the publication of data for May.

In January and February, i.e. before the US attack on Iran, the rate was only 2.1%. To make matters worse, core inflation is also rising, which does not take into account energy, fuel and food prices.

The longer the Strait of Hormuz remains closed, the greater the risk of more serious consequences in the form of increased inflation. “If there is no quick and significant drop in fuel prices, the 4% level may be broken this year. Although this increase is likely to be short-lived, for now inflation trends raise justified concerns,” Citi Handlowy economists point out.

|

NBP, own study

Core inflation, which is a key parameter for the Monetary Policy Council when deciding on interest rates, may also go up. Erste analysts wrote in a recent report that they believe this measure will remain in the range of 3-3.5% in the summer. year to year, and then it will increase to approx. 4%. year-on-year at the end of 2026. They noted that this forecast largely depends on the development of the situation around Iran and the oil market.

The baseline scenario is moving away, which means a growing risk of rate increases

In basic scenarios, economists forecast that NBP interest rates will remain unchanged at least until the end of this year, but under certain conditions. For example, BNP Paribas analysts are based on the assumption that exports of energy raw materials from the Middle East will be restored by summer at the latest and fuel prices will decline. This is a key assumption, because if there is no peace and the Strait of Hormuz remains closed, tightening the monetary policy by the Monetary Policy Council will, in their opinion, become a realistic option. In this case, they expect at least two rate increases this fall. In an extreme case, they do not rule out the first such move in July.

See also: WIBOR will live longer. We have learned the official date of the key indicator for borrowers

— Given the current inflation path we predict, we still see the possibility of a reduction in the middle of next year, which would complete the process of easing monetary policy started last year, anchoring the NBP reference rate at 3.50%. – reserves Michał Dybuła, chief economist of BNP Paribas Bank.

|

Citi Handlowy, Bloomberg

Citi Handlowy economists speak in a similar tone. In their opinion, the MPC's patience may be tested, and the prolonged blockade of the Strait of Hormuz shifts the balance of risks towards higher rates and inflation every day. They pointed out that possible signals of inflation spreading to other sectors of the economy could determine the need for increases, and the July NBP projection would be a convenient pretext in this situation.

“In our base scenario, we still assume that rates will remain unchanged until the end of the year. However, we see a risk that if the blockade of the Strait of Hormuz is prolonged until the end of June, the risk of persistent inflationary pressure may justify increases. In such a scenario, the scale of increases by the Monetary Policy Council could reach up to 1 percentage point in total. in the horizon of 6-12 months“- they add.

PKO BP experts also assume in the base scenario that the NBP will not raise rates this year. They are based, among others, on: on the path of crude oil prices in line with market contracts, which assume gradual normalization on the energy market in the coming months.

— This would mean that the pro-inflation impulse generated by fuel prices will fade out, inflation will no longer increase significantly in the second half of 2026, and from March 2027 it will decline significantly. In such a scenario, we would be dealing with a temporary shock, short enough not to generate the risk of strong second-round effects, says Marta Petka-Zagajewska, director of the Macroeconomic Analysis Office at PKO BP.

He adds that this would allow the NBP and other central banks to refrain from reacting by increasing rates, and in such a scenario, there could even be room to reduce interest rates at the end of next year.

Investors know: inflation will force central banks to increase rates

The market is unyielding and assumes that there will be two or three interest rate increases in Poland in the next 12 months. This would mean an increase in the reference rate from the current 3.75%. up to 4.25 percent or 4.50 percent In the case of the European Central Bank, two increases are possible this year, with the first one in two weeks. Market expectations indicate that the US Federal Reserve will make one rate hike early next year.

See also: Economists are revising forecasts of Polish GDP growth. Rates may go up

— Markets have no major doubts and have been pricing in a slight tightening of monetary policy by major central banks from the very beginning. Traditionally, raising rates in response to a negative supply shock, especially a standard one such as the one caused by the war in the Persian Gulf, does not make much sense, because such shocks are “self-suppressing”: price increases reduce the purchasing power of consumers and force them to reduce spending in areas other than fuels and other energy carriers, and also reduce the profitability of production – says Piotr Bartkiewicz, economist at Bank Pekao.

|

Citi Handlowy, Bloomberg

He adds that in certain circumstances, a negative supply shock may result in an acceleration of wages and prices of other goods and services, but these conditions are not currently met. It points out that labor markets around the world are rather weak, many economies are battered by previous shocks, and companies are less willing to raise prices.

Economists divided in interest rate forecasts

— It cannot be denied that, for now, the conflict development scenario does not fit into the previous “basic” assumptions. First of all, the unblocking of the Strait of Hormuz is delayed, which – even if oil prices do not rise significantly – prolongs their persistence at a clearly elevated level. The longer the conflict lasts, the higher the risk that its consequences will affect a wider area of the economyincluding industries without direct exposure to the fuel market. In such a scenario, rate increases aimed at limiting the spread of the inflationary effects of the conflict may turn out to be necessary, and rather in the form of several – probably two or four moves – rather than a single adjustment – says Marta Petka-Zagajewska.

He adds that However, in her opinion, the first increases would not take place earlier than after the holidays. – While the base scenario assumes the stabilization of NBP rates at the current level, the balance of risk factors is clearly tilted towards higher rates – he points out.

|

own work

— Without ignoring the increase in inflation, the central bank can wait it out without increasing rates. However, due to the oil shock, 2026 will be the sixth (!) year in a row in which major central banks will not meet their inflation target. This is a gigantic image, reputation and political problem, and the experience from 2021-2022 tells central bankers to be safe.. As a result, the standard response has become not only “hawkishness”, but even raising rates, as in Australia or Norway – says Piotr Bartkiewicz.

He points out that the NBP has a slightly better starting position compared to, for example, the ECB, which will have a hard time not meeting the expected two rate increases.

— Inflation was below target when the shock hit and interest rates were relatively high. So while the MPC's shift to a more hawkish position is understandable, taking into account the change in macroeconomic scenarios and global trends, tightening monetary policy is not necessary. Some forecasts, including ours, indicate that inflation has left the band of permissible deviations from the target, but no one, including the NBP itself, expects this to be permanent. Inflation will fall next year and return to the target. In our opinion, the NBP will not increase rates because it will not have to and the market pressure is not great – argues the Bank Pekao economist.

If rates rise, borrowers will pay more

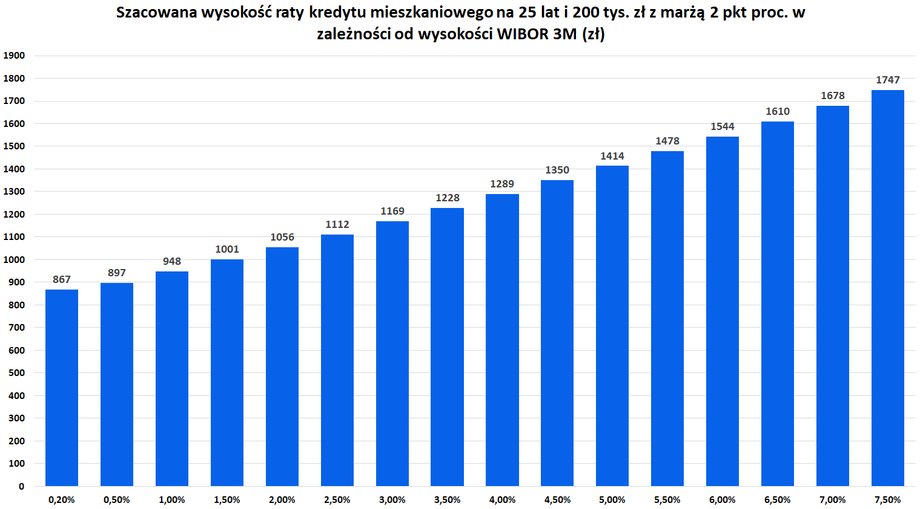

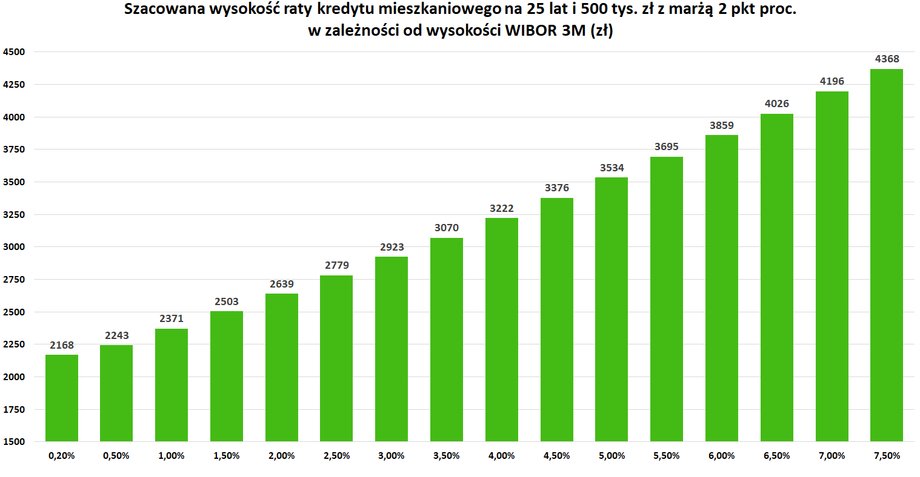

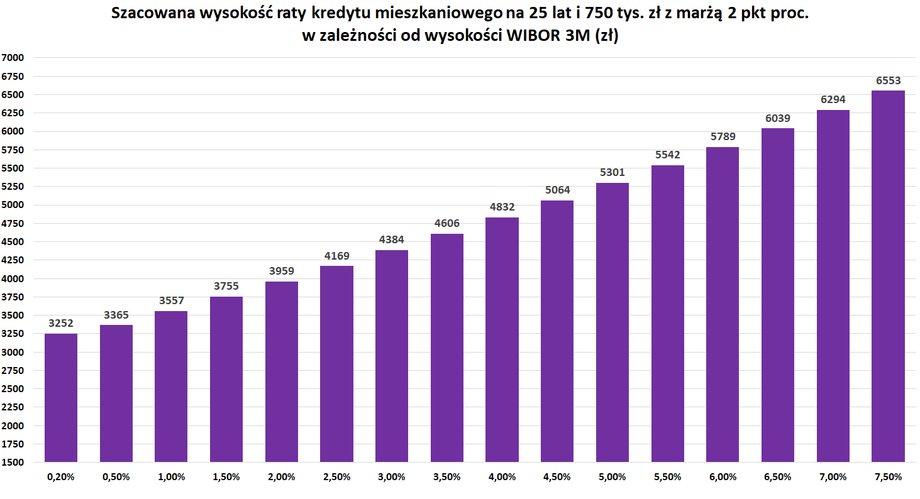

We don't know what the actual cost of money will be, but we can adopt scenarios and try to estimate what the WIBOR will be and how it will affect the installments of consumers repaying housing loans worth PLN 200,000. PLN 500 thousand PLN and 750 thousand zloty (the remaining repayment period is 25 years and the margin is 2 percentage points).

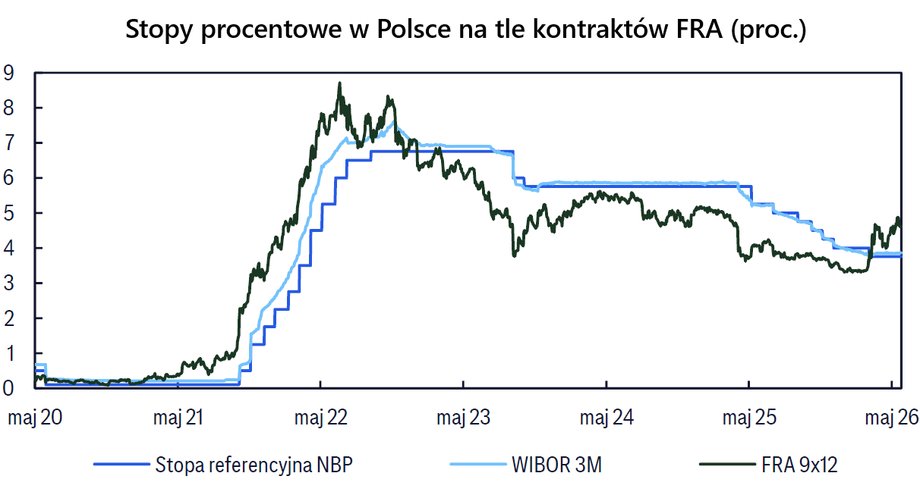

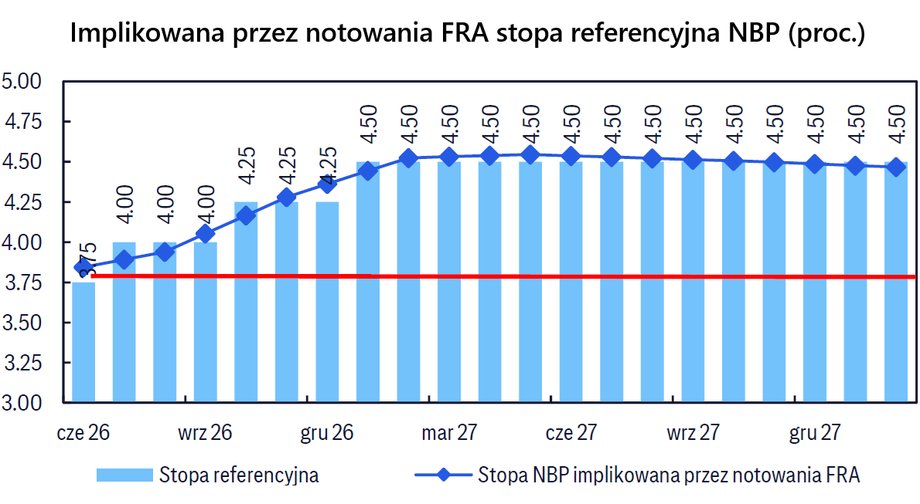

WIBOR 3M is currently approximately 3.85 percent, which is only 0.10 percentage point higher. higher than the NBP reference rate and it can be assumed that it does not take into account the change in the cost of money in the next three months. If the NBP rate increased to 4.25%. or 4.50 percent – and assuming no market expectations for further changes – WIBOR 3M rates should reach 4.35%, respectively. and 4.60 percent

|

own work

In the case of a loan with repayment capital of PLN 200,000. zloty installment at the WIBOR 3M rate of 3.85%. is approximately PLN 1,270. Increase in the market index to 4.35%. or 4.60 percent would mean an installment higher than now by PLN 62 and PLN 93, respectively.

Let's take a closer look at a loan where there is still PLN 500,000 to repay. zloty. The current installment here is PLN 3,175 per month. An increase in WIBOR rates to the above-mentioned levels means an increase in the installment by almost PLN 155 and PLN 230, respectively.

In a mortgage worth PLN 750,000. PLN installment at the WIBOR 3M rate of 3.85%. it's approx. PLN 4,765. Increase in the market cost of money index to 4.35%. or 4.60 percent would increase the monthly levy to the bank by PLN 1,818 and PLN 1,935, respectively.

|

own work

Author: Maciej Rudke, journalist of Business Insider Polska