publication

2026-03-27 21:14

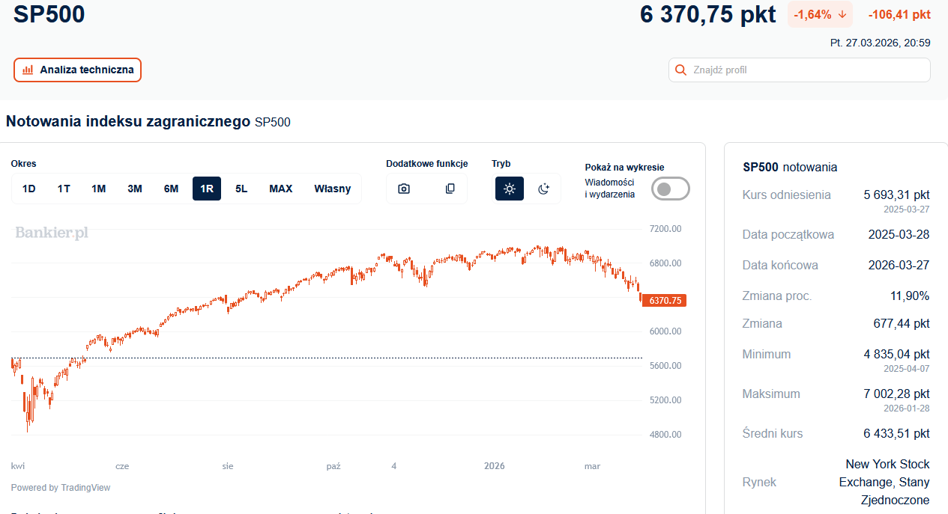

Friday's session on the New York stock exchanges brought a continuation of the significant decline in shares from the previous day. Due to stagflation concerns, the S&P500 index dropped to its lowest level in over half a year.

At the close of Friday's session, the S&P500 index was at 6,368.36 points, which meant a decline of 1.67% and the lowest closing price since September 3. Nadaq dropped by 2.15% and finished with a score of 20,948.36 points, having already lost almost 13% compared to last year's bull market peak. The Dow Jones retreated by 1.73%, to 45,166.64 points. – which is also the lowest since the beginning of September.

The reasons for the further decline in shares are quite obvious. This is about continuing the war with Iran, which has been going on for a month now. The Israeli-American blitzkrieg is slowly turning into a long war of attrition that the Yankees seem unable to win. At least not without the intervention of ground troops. Hence, President Trump's next 10-day ultimatum can probably be interpreted as a sign of weakness, not generosity, of the United States. On Friday, President Donald Trump extended the deadline for attacking Iran's energy infrastructure to April 6, just over a week after the original deadline of today.

Advertisement

– As requested by the government of Iran, please let this statement serve as proof that I am suspending the destruction of the plant,” Trump wrote in a post on the Truth Social website. – Talks are ongoing and, despite erroneous claims from the fake media and others, they are going very well. Thank you for your attention! – added the US president. However, fewer and fewer people in the markets believe that any dialogue with Tehran is being conducted at all.

And this moves us away from the imminent end of the war in the Persian Gulf, unblocking the Strait of Hormuz and restoring the missing 10-15% of global oil supplies and 20% of LNG. Also causing concern is the rising price of crude oil, which on Friday increased by another 4%, to USD 106 per barrel in the case of Brent crude.

“The war could end at any moment and the situation could return to normal within a few months, but oil could equally cost $200 a barrel in six months,” said Nicolas Domont, fund manager at Optigestion.

“The longer the Strait is closed, the worse the oil market will be,” said Jay Hatfield, founder and CEO of Infrastructure Capital Advisors. “The price will come down significantly, but there will still be an inventory problem once the Strait reopens, so if the Strait reopens for another month, the price of oil could stay around $80 for some time until we can rebuild supplies,” Hatfield added.

And this, in turn, leads to increased inflationary pressure and fears of stagflation – a period of high inflation and low (or even negative) economic growth. There is more and more talk about the threat of a repeat of the 1970s, as the world is already experiencing its second energy crisis in four years. That is why everyone is now looking at the debt market, where yields on US and German treasury bonds have approached dangerously high levels. In the case of Tresuries, the market shows behavior that last occurred together in May 2008 – just before the most severe phase of the Great Financial Crisis of 2007-09.

The futures market estimates the chances that the Federal Reserve will decide to increase interest rates at least once by the end of the year at nearly 25%, according to FedWatch Tool calculations. This is clearly less than two days ago (then it was almost 50%), but a month ago the market was discounting REDUCTIONS in the federal funds rate of 50-75 bp. The change is therefore very sudden and has a negative impact on the valuation of stocks and bonds.

In this context, the inflation expectations of consumers, producers and investors may be key. In a March report from the University of Michigan, short-term inflation expected by households rose to 3.8% from 3.4% in February. Long-term expectations decreased from 3.3% to 2.2%. But that's still well above the Federal Reserve's 2 percent target. Therefore, central bankers have no right to say that “inflation expectations are well anchored.”

The publication contains affiliate links.