An extensive study of income taxation in Romania reaches an uncomfortable conclusion: the current tax system does not tax income, but the legal form. That is the explanation why employees with the same duties, who earn about the same, pay completely different taxes. It is not an exception. It's the rule.

In the analysis made, tax consultant Gabriel Biriș shows that the total tax burden should depend exclusively on the size of the income, not on the legal form under which it is structured. This principle – horizontal equity – is the foundation of any functional tax system and is enshrined in the unanimous practice of the member states of the OECD and the European Union, says Biriș.

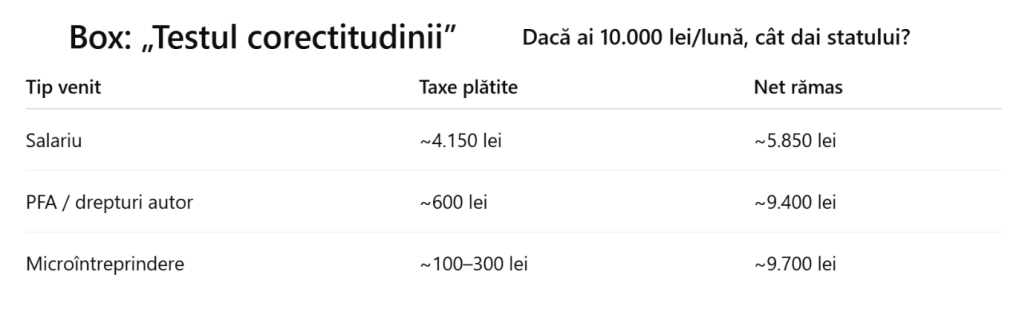

How big are the tax differences for employees with similar incomes

The analysis shows that the total tax burden varies in Romania by a factor of up to 7:1 for incomes of a comparable level:

- an employee with a gross income of 10,000 lei per month bears a total tax burden (income tax + CAS + CASS) of 41.5%. from gross income.

- a taxpayer with identical income, structured by intellectual property rights, bears a total tax burden of approximately 6%. The difference is 35.5 percentage points – the tax burden on salary is almost 7 times higher than that on royalty income

- a sole partner of a micro-enterprise with a turnover of 120,000 lei per year and minimal real expenses can reach an effective tax burden of 1–3%. (see analysis of micro-enterprise data in section 2.3.1, Table 6, which shows that 40.7% of micro-enterprises report losses comparable to turnover)

“These differences exclusively reflect the legal form under which the income is structured – a form that the taxpayer can choose and modify in order to benefit from a lower tax burden, which is natural. In a system where the tax burden depends not on how much you earn, but on how you are legally organized, the rational incentive is not compliance, but optimization,” says Biriș.

- 72% of authorized natural persons declare an average net income of 380 lei/month — below the poverty threshold, for activities performed by professionals (consultants, IT-ists, architects, accountants).

- 82% of owners who declare rental income report an average income of 160 euros/month — in a market where the average rent for a two-room apartment in Bucharest exceeds 500 euros.

- 40.7% of the 702,691 micro-enterprises with a turnover of less than 100,000 euros declare losses equal to the turnover — that is, a level of expenses twice compared to revenues, which, for a functional company, is mathematically impossible without a significant component of personal expenses of the associate (the data used by Gabriel Biriș are valid for 2024).

Chronic budget revenue deficit

These figures describe a profile of taxpayers responding to the incentives created by a fragmented and inefficient tax system, according to the analysis, and the consequence is a chronic deficit of budget revenues:

• Romania collects total tax revenues of approximately 27.3% of GDP — the penultimate place in the European Union, almost 14 percentage points below the EU average of 41.2%.

• Romania has, for salaries, one of the highest fiscal burdens in the EU (social contributions of 29.9% of the gross, the highest borne by employees in the EU, according to OECD Taxing Wages 2025).

The collection deficit is therefore not caused by low tax rates. It is the consequence of a systematically eroded tax base: the fragmentation of regimes, the arbitration between legal forms, the exemptions and exceptions granted without impact assessment and withdrawn without a transition period, and a legislative instability that makes voluntary compliance impossible – the pillar of any modern tax system.

pupdating the CAS calculation base

The reform proposed in the study is based on capping the CAS calculation base at the amount of income from work. “For income from salaries and similar to salaries, the calculation base of the CAS must be equal to the minimum between the salary or gross remuneration and the ceiling, and for income from the transfer of intellectual property rights, we consider that it is justified to keep a deduction of 20% from the gross income, to compensate for some expenses incurred in the exercise of the activity. However, we consider that the deduction of 40% can only be justified in the case of monumental works of art (as we have had until 2018)”, the document suggests.

Also, for income from self-employed activities, the basis of calculation should remain the net income calculated based on the data from single-item accounting, without the possibility of calculating the net income based on income norms, with the exception of income from agricultural activities, where taxation based on the income norms must be kept, but the income norms reassessed, at least according to inflation (these remaining unchanged from 2019), the author of the analysis proposes.

For income from sports contracts, the basis of calculation should be the gross income obtained under the contract. “Professional athletes are practically employees of the clubs where they operate,” the document states.

A proposal for taxation of pensions

Biriș proposes a technical idea: to separate the two types of pensions (Pillar I and Pillar II) and tax them differently.

“We propose the legal separation of the CAS contribution for Pillar I, which is calculated on a capped basis, from the contribution to Pillar II, which is calculated on full gross income, without a ceiling. This ensures that capping protects the sustainability of Pillar I without sacrificing the accumulation in Pillar II — the only long-term savings tool accessible to the majority of Romanians. Thus, the contribution to Pillar II will continue to be calculated on full gross income, without a ceiling, this being a contribution to one's own individual account, does not generate obligations for the state, so there is no rationale for capping”, note the authors of the analysis.

This is actually standard European practice: in Germany, private occupational pension contributions (betriebliche Altersvorsorge) operate independently of the public contribution ceiling (Beitragsbemessungsgrenze). In Sweden, the 2.5% premiepension contribution applies to the whole income, and the occupational pension compensates with additional contributions above the ceiling, up to 30% of the income above the threshold

In addition, the analysis also proposes:

- a dividend taxation system that takes into account the profit tax paid by the company distributing the dividend, by subtracting the profit tax from the dividend tax;

- the introduction of provisions of the CFC Rules focused on the UBO (OECD), by assimilating undistributed profits from companies located in poorly taxed jurisdictions (tax havens), so as to discourage the accumulation of untaxed amounts in such companies, amounts that are very rarely distributed as dividends to UBOs resident in Romania, being rather used for purchases of real estate abroad or for pleasure payments, for UBOs.

- assimilation of income from the liquidation of a legal entity with dividends. “We believe that there is no reason to tax the two types of income differently,” says the author of the analysis

- the assimilation of all expenses made by the company in favor of the associates of the income from dividends, especially in the context of the implementation of the RO e-Invoice, RO e Case de marcat fiscal systems.

Specifically, if the actual profit tax paid by the distributing company or its subsidiaries from which it received dividends is 16%, the dividend tax owed by the shareholder is 0%.

If the effective income tax is less than 16% (for example, as a result of obtaining non-taxable income)), the difference up to 16% is the dividend tax.

“Pension income represents a replacement income, obtained as a result of paying CAS during working life. We must take into account that CAS (the source of funding of the pension) was and is deductible when calculating income tax, so CAS was not taxed at the time of payment. As a result, we consider it fully justified to tax pensions under the same conditions in which the income from which CAS was paid was taxed, including with regard to the payment of CASS.

Consequently, we consider that – regarding the calculation basis of CASS, the payment of CASS only for the part of the pension that exceeds 3,000 lei/month is neither economically nor morally justified, so we propose to eliminate this threshold and replace the fixed amount of 3,000 lei with the degressive deduction taken into account when determining the salary tax. What we propose is not the “introduction” of pension taxation, but the replacement of an arbitrary fixed threshold with a degressive deduction that better protects small pensions”, the authors of the analysis sent by Gabriel Biriș also state.