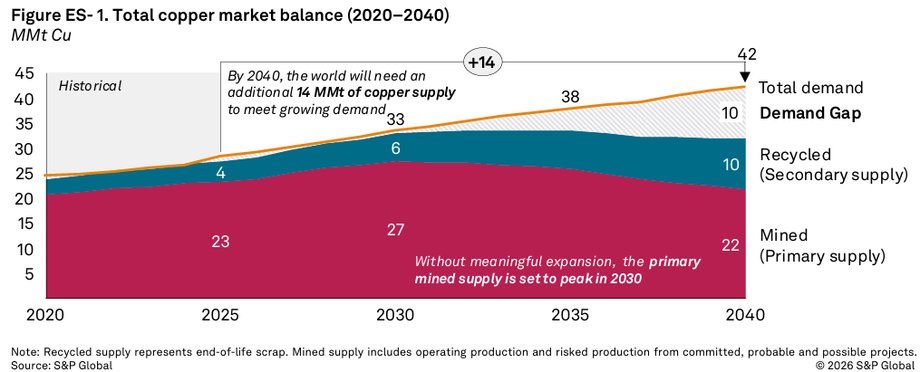

Of course, it's about copper. Due to the physical properties that make this metal an excellent conductor of electricity, the modern world's circulatory system is made of copper. However, a detailed report by S&P Global analysts expresses concerns that unless specific actions are taken, within a few years, the ever-increasing demand for this raw material will be met by its decreasing productionwhich means that in 2040 the demand for copper may exceed the supply by as much as 10 million tons, or almost 1/3 of the global production of this metal.

The S&P Global report warns of a gigantic copper shortage visible on the horizon

|

S&P Global

Sources of the growing demand for copper

The largest global consumer of copper is electrification and industrial development of the world. On a global scale, China's gigantic projects will, of course, consume this raw material particularly quickly. Developing countries will also consume a lot of copper, primarily India, but also Africa, which represents an increasing part of the world's population and still has a lot of work ahead of it related to industrialization and electrification.

Another reason for the growing demand for copper is the global energy transformation. Building more renewable energy sources, energy banks and the entire transmission infrastructure (power lines, transformers, etc.) – this cannot be done without copper. This topic is also related to the growing popularity of electric cars, which require on average almost three times more copper than their combustion counterpartsso the more popular “electrics” become, the faster the demand for copper will grow.

However, the above two factors increasing the demand for copper have been well known for many years. Lately However, two new items have appeared on the list of copper consumers with a rapidly growing appetite: data centers and the arms industry.

Technological and geopolitical changes unexpectedly come into play for copper

It is estimated that in 2022 – i.e. in year of ChatGPT's debut — data centers consumed around 100 GW. Currently, however, many data centers are being built around the world and some complexes already consume over 1 GW, and this size is soon to become a standard among the largest players on the market, such as Google, Meta, Microsoft, Amazon, OpenAI, or Oracle.

We also don't know for sure what exactly is happening in China, but we can assume that the data centers built there will be neither fewer nor smaller. The S&P Global report estimates that if economic factors do not slow down the development of AI, in 2040, data centers will consume 550 GW. This means that not only do modern AI systems themselves consume a lot of copper – the most modern equipment of this type, the Nvidia GB200 NVL72 system, has 5,000 wires with a total length of over 3 km – but a lot of copper will be needed to generate and supply the necessary electricity to them. And if there is a breakthrough in robotics, it may be only the beginning of an exponential increase in demand for copper due to AI solutions.

Each advanced AI system uses hundreds of kilograms of copper in kilometers of cables and in the chip cooling system

The second new growth vector is the arms industry. The geopolitical situation is much more unstable than, for example, a decade ago and many countries around the world is increasing its arms budget, which results in a growing demand for copper, which is used to produce ammunition, engines, rockets, vehicles, drones – in short, almost everything related to this topic.

It is true that it is estimated that the accelerating arms industry is responsible for only 4%. overall increase in copper demand, but its strategic importance will certainly cause it to push other projects out of the supply chain.

World copper production: first an increase, then a decline

On the one hand, we have demand for copper growing faster than expected, and on the other is expected to contribute to the copper shortage announced in the report decrease extraction of this raw material. S&P Global analysts assume that copper mining will peak in 2030, after which it will begin to decline.

Existing copper mines experience increasing costs and difficulty of mining, as well as a decline in the quality of the raw material, which means that more and more of it must be mined to obtain the same amount of pure copper. However, the obstacle standing in the way of creating new mining sites is time. Analysts estimate that on average, it takes 17 years — largely due to ongoing administrative processes.

Addressing this topic will therefore be crucial in the coming years if the world does not want to end up with a huge shortage of a very important raw material. The seriousness of the situation is added by the fact that currently about 50 percent of the world's copper smelting takes place in China.

Poland in a strong position in the face of the copper deficit

The analysis conducted by S&P Global is, of course, only an estimate making certain assumptions, but even if we do not end up with 10 million tons of copper missing in 2040, the trend of growing importance of this raw material is a fact.

In November 2025, copper was added to the list of critical minerals in the USA, and in 2024, copper was included on the list of strategic raw materials under the EU CRMA regulation (Critical Raw Material Act). Although China specializes in copper processing, it does not have large enough deposits itself, which is why it has the world's largest strategic reserves of this raw material.

This puts Poland in a strategic position. Poland has one of the largest copper deposits in the world and the largest in the European Union, concentrated in the Fore-Sudetic Monocline and the North Sudetes Trough, i.e. north of Lubin and north of Jelenia Góra. The State Raw Materials Policy adopted in 2022 assumes that by 2040, Poland's demand for refined copper will increase from less than 300,000. tons per year to 400-450 thousand tone.

KGHM Polska Miedź currently produces less than 600 thousand tons per year. tons of electrolytic copper obtained in the overwhelming majority from its own mining, so Poland will not run out of this raw material. The situation in our country is completely opposite to that of, for example, Germany. Germany is the EU's largest producer of refined copper, but all the raw material going to German smelters is imported or recycled.

The increasing demand for copper and the specter of potential shortages give Poland a unique position in the region and make KGHM Polska Miedź one of the key companies for the future of the Polish industry. Now this emerging opportunity on the horizon must be used effectively.