Grandparents with grandchildren. Photo source: Shutterstock

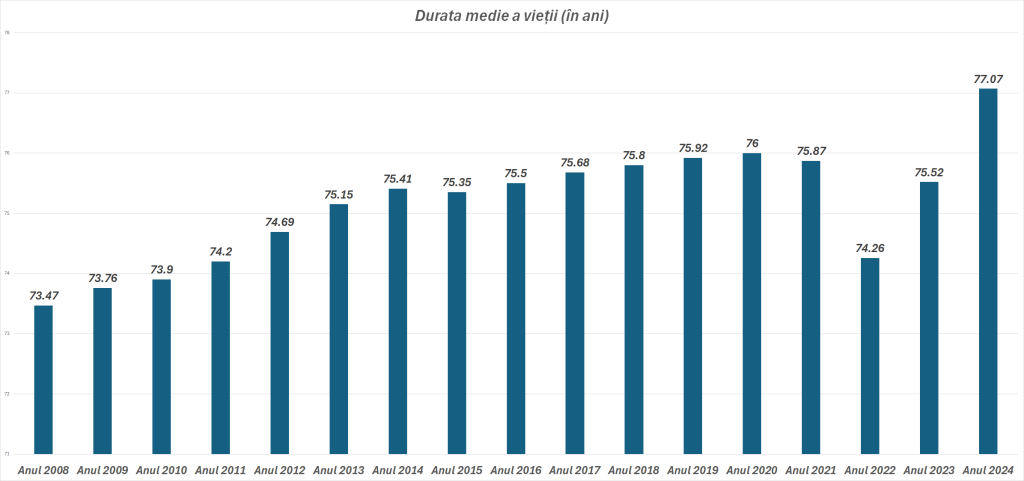

The good news is undeniable: life expectancy has reached an all-time high, exceeding 77 years, according to Statistics data.

However, behind this positive statistic hides a harsh reality: the longer we live, the more money we need. And most of us don't have them, Market Watch notes in an analysis.

One of the most common concerns in Romania is related to how much money you need in retirement to have a peaceful old age. So I looked at some data and did some calculations.

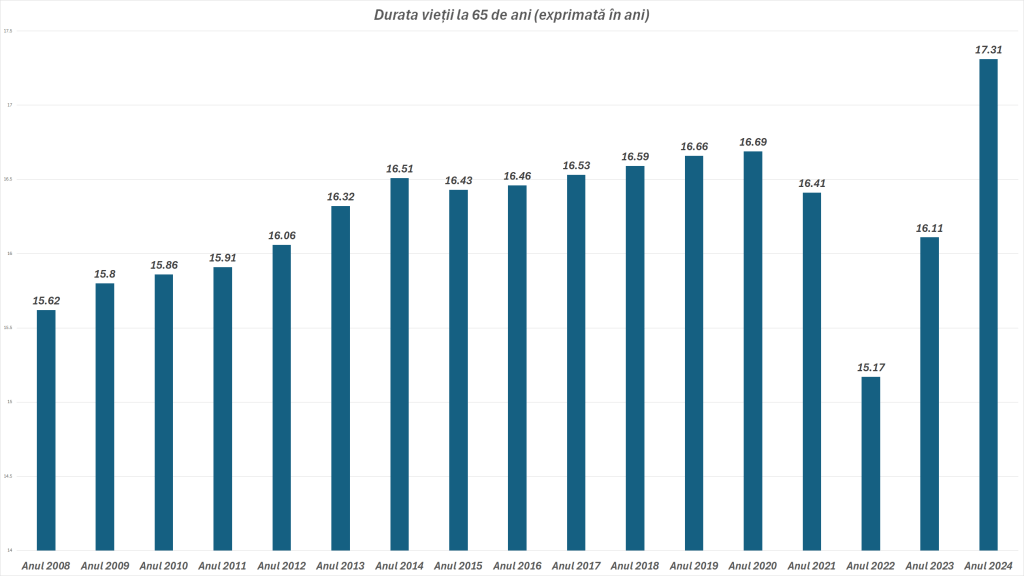

Sure, we're talking about media. We assume that you will retire in October 2025. Your monthly expenditure is around 3000 lei, according to Statistics, a level that you want to keep during the period in which you will be retired. I also took Eurostat data into account, which shows that life expectancy at the age of 65 in Romania is about 18 years. And that inflation, even if this year and next year will be higher, will finally fall within the NBR target.

Putting these data together, you will need to have around 1,000,000 lei (920,000 lei to be exact) to maintain your standard of living. If you already have that money, you can rest easy.

If you don't have them, you should think about how to get them.

Of course, the structure of consumption will be different than at present. Maybe you won't spend as much on clothes, but medicine expenses will. Maybe you will live not 18 years of retirement, but 25 or 30.

In the US, The Wall Street Journal spoke to several octogenarians and nonagenarians. Some regret that they were not more generous with themselves, others that they did not save enough.

Sue Jones thought she had more than enough money to live on in retirement. But he didn't expect to live to 90. She had $50,000 in a retirement account in addition to her pension of about $2,900 a month.

But her income no longer covered the mounting bills. Sue has been in and out of the hospital several times this year, racking up medical bills and prescription drug co-pays. Her children help her with the expenses because she wouldn't be able to cope otherwise. “I planned to die at a more normal age, but that's not what God had in store for me!” she told the Wall Street Journal.

The traditional financial planning model assumes that you would need 80% of your salary to support your lifestyle in retirement.

Ty Bernicke, in an article in the Journal of Financial Planning , a 75-year-old spends about 50% less than the average 45-54-year-old.

But even if you were to spend 25% less every 10 years as you get older, inflation should easily wipe out all of these advantages, as 3% per year will result in a much larger increase in spending over 10 years than the 25% reduction.

Tips:

- Reduce your apartment expenses. Move to a smaller apartment. That way, you also reduce utility bills

- Find a side job: from walking pets to babysitting.

- Cancel any unused subscriptions

- Try to fix things yourself. Thanks to YouTube and the internet in general, we can learn how to fix almost anything.

- Cut down on food expenses. You'll be amazed at how much you can save over the course of a few months. One of the best ways to do this is to plan your meals. This means you can calculate exactly how much you will spend before you go shopping and reduce the chances of going over budget.

- Designate a no-spend day a month where you simply don't spend a dime. This could mean preparing all your meals from ingredients you have at home, opting to socialize at the park or at home, and spending a relaxing evening reading or watching TV.

The fear that surpasses even the fear of death

Nearly two-thirds of Americans (64%) fear they will run out of money before they die. According to a study by the Allianz Center for the Future of Pensions, this fear is even greater than the fear of death.

Anxiety is most intense among Gen Xers (70%) and millennials (66%), while more than 60% of baby boomers – the youngest of whom are now 61 and about 10,000 retire every day – fear their money won't be enough.

And it's not at all unreasonable.

Increasing life expectancy is a good thing, no question. However, in a time of rising cost of living and reduced savings, this becomes an economic challenge.

Living longer is good news. Being able to afford it — that's the real challenge of our generation.