Few phrases more accurately describe Romania's structural vulnerability than the one in the opening of the Consilium Policy Advisors Group (CPAG) report: “twin deficits” — the budget deficit and the current account deficit simultaneously evolving at high levels. It is the equivalent of a household that constantly spends more than it produces and borrows for the difference, hoping that the future will be more generous.

See the full report here.

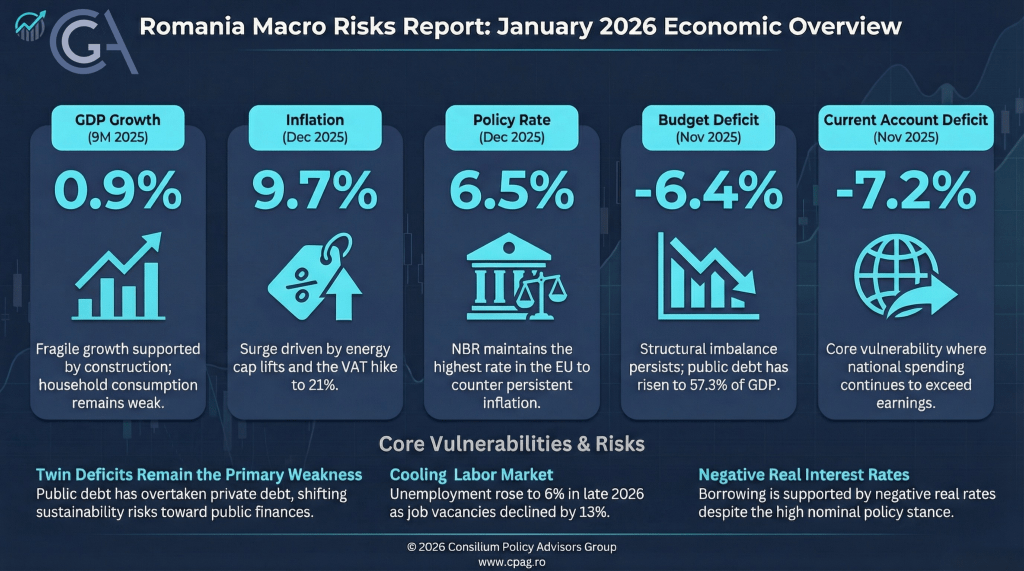

The most relevant change, noted discreetly in the report, is the inversion of the ratio between public and private debt: the state has become the main generator of debt, not the productive economy. In quarter II/2025, public debt reached 57.3% of GDP, clearly exceeding the private sector, which continues the deleveraging process.

- This shift of risk from companies to the state is essential: in an economy with increasing euroization and low confidence in the currency, state funding becomes a matter of macro security.

To finance this difference, the Romanian state borrows more and more expensively: long-term bond yields have risen to ~6.9% in 2025, a signal of a growing risk premium

Inflation: It wasn't demand that broke the peace, it was policies

Romania entered 2026 with the highest inflation in the European Union, after months in which only Hungary competed for this title. In December 2025, annual inflation reached 9.7%, i.e. 5 times more than the euro area (1.9%) and almost 4 times as much as Poland (2.4%). The cause was not an “overheated” economy or excessive consumption, but public policies: the liberalization of electricity prices in July 2025, the increase of VAT from 19% to 21% in August 2025.

- 80% of the jump in inflation between June and December 2025 came solely from energy, the report said.

This episode is a textbook lesson in how inflation can come “from above”, from administrative decisions, not domestic demand. In a country where 25% of the consumption basket is services and another 36% food (processed + unprocessed), such a combination simultaneously hits two sensitive areas: bills and the food market.

The BNR estimates a slow disinflation to 3.7% only in December 2026, so Romania will remain a country with tense prices for a long time to come

NBR between a rock and a hard place

If there is one place where Romania's contrast with the rest of Europe is striking, it is monetary policy. While the European Central Bank, Poland or the Czech Republic cut interest rates in 2025, Romania kept them at 6.5% — the highest level in the EU

This conservative choice has two explanations:

- High inflation — easing would have been impossible without losing credibility.

- The twin deficits — easing would have put pressure on the exchange rate and government funding.

Even so, the currency did not remain fully protected: the leu depreciated ~2.3% against the euro in 2025, while the real exchange rate continued to appreciate (+3.2% until October), affecting the competitiveness of exports.

There is another sensitive element, mentioned dryly in the report: growing euroizationboth in loans and in deposits, a sign of low confidence in the national currency

In short, Romania is experiencing a monetary paradox: high interest rates, low trust.

The labor market: economists look at numbers, people at jobs

If deficits are the fear of governments, unemployment is the fear of people. In 2025, the labor market changed quietly but decisively:

- Average unemployment rose to 6% (up from 5.4% in 2024)

- the number of vacancies decreased by 13%

- the tension on the labor market has decreased (from 13 to 15 unemployed per vacancy)

- wages increased by 7.1%, which is below inflation

These are not just statistics. They are the symptoms of an economy losing its consumption engine — not because people don't want to spend, but because they can't.

The report dryly notes one risk for 2026: the impact of AI technologies, possibly geared more toward automation than job creation—a rather rare warning in a macroeconomic analysis paper

Economic growth: the engine that coughs but does not stop

After three decades of almost constant growth, the Romanian economy is entering a period of “growth without satisfaction”. In the first 9 months of 2025, GDP grew by just 0.9%, slightly below the pace of 2024.

The composition of the increase, however, deserves attention:

- agriculture and construction supported supply

- investment supported demand

- population consumption has slowed

- net exports surprised positively for the first time in 7 quarters

It is an economy that is still moving forward, but not due to internal strength, but thanks to branches with a volatile profile: agriculture and externally financed investments.

For 2026, the report clearly delineates the “winds”:

Head wind:

- persistent inflation → weak consumption

- fiscal consolidation → low demand

Tailwind:

- European funds (RRF, SAFE)

- negative real interest rates that stimulate lending

Conclusion: Romania between the two worlds

Romania begins 2026 at a paradoxical point: a country with large deficits, but in the EU; with the highest inflation but stable interest rates; with high investment but low consumption; with public debt increasing, but still below the European average.

It is not a crisis: it is a normalization of vulnerability.

In simple language: Romania is not collapsing, but it is getting more expensive. The state does not go into default, but it becomes difficult to finance. The population does not go into massive unemployment, but it loses purchasing power. The economy is not going into deep recession, but it is losing its domestic fuel.