The year 2025 brought a surprisingly lukewarm response from buyers to a series of as many as six interest rate cuts. Although financing conditions gradually improved, this did not lead to a mass return of customers to sales offices. Effect? In the largest cities, the offer of apartments reached record levels, and the sales pace – despite a slight rebound – remained moderate.

Read also: Purchase of an apartment by young Poles. Prices and stress inhibit decisions

— It was a cold shower for developers who were counting on a sharp rebound in demand after rate cuts – comments Marek Wielgo, expert of the RynekPierwotny.pl portal. As he explains, the key problem turned out to be the structure of loans. Most buyers chose financing with a periodically fixed rate, which became cheaper much slower because its interest rate is linked to bond yields and not directly to WIBOR.

Additionally, purchasing decisions were influenced by the situation on the labor market. Slower wage growth, rising unemployment and concerns about employment stability have made many potential buyers postpone the decision to buy an apartment.. Demand grew gradually, supported mainly by promotions, bonuses and developers' flexible pricing approach.

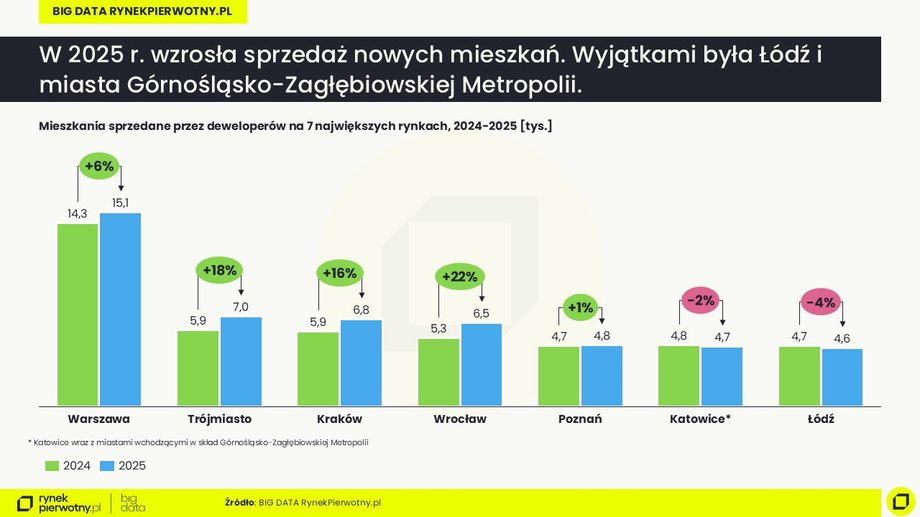

BIG DATA RynekPierwotny.pl data shows that in the seven largest metropolises – Warsaw, Kraków, Wrocław, Tricity, Łódź, Poznań and the Upper Silesian-Zagłębie Metropolis – in 2025, approx. 49.5 thousand were sold. apartments, i.e. by 8%. more than a year earlierbut as much as one fifth less than in the record-breaking year of 2023, driven by the “Safe Credit 2%” program.

Sale of apartments

|

Primary Market

See also: Pension with a bonus of several hundred thousand zlotys. Check this method

Apartment prices 2025: stabilization instead of double-digit increases

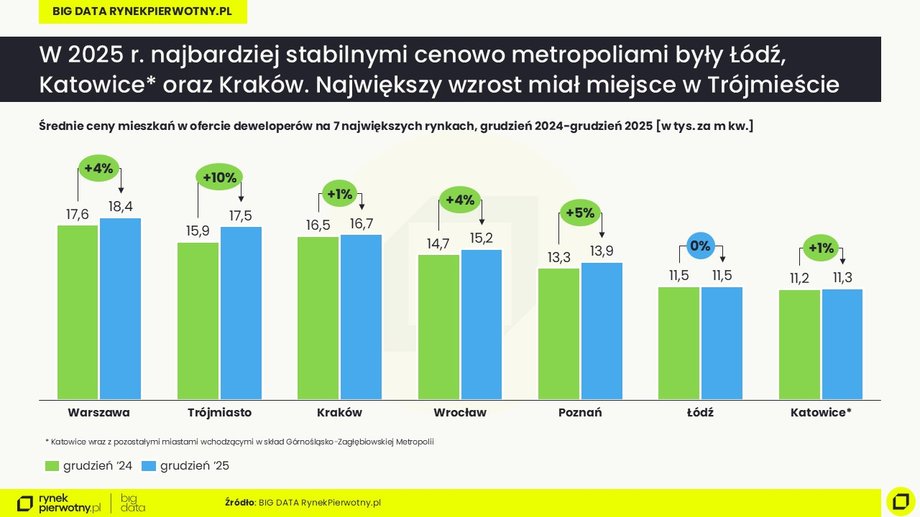

After several years of dynamic increases average prices per square meter have slowed down significantly. In most cities, the increases were symbolic, and in some markets practically invisible. Łódź turned out to be the most price-stable metropoliswhere the average price per square meter in December 2025 was almost identical to the year before. In the Upper Silesian-Zagłębie Metropolis and Kraków, the increase was approximately 1 percent, in Warsaw and Wrocław – 4 percent, in Poznań – 5 percent, and in the Tricity – 10 percent.

However, this latter result may be misleading. As Marek Wielgo emphasizes, it does not mean widespread price increases, but a change in the structure of the offer. In Gdańsk, many expensive apartments were put on the market in Śródmieście and at the Bay of Gdańsk, which automatically increased the average.

Apartment prices

|

Primary Market

Worth reading: Changes in housing in 2026. Buyers will benefit, but will pay a higher price

— Developers rarely lower prices outright. They much more often camouflage discounts in the form of promotions, discounts or additional benefits – reminds the RynekPierwotny.pl expert.

In turn, JLL Polska data shows that price pressure is even more visible in transaction prices, not offer prices. Aleksandra Gawrońska, Director, Head of Residential Research at JLL Polska, points out that in the fourth quarter of 2025 in most cities there were more decreases than increases in the prices of apartments sold.

In Wrocław, average transaction prices dropped quarter by quarter by 4.4%, in Kraków and Poznań by 2.7%. Stability or growth remained only in places where there is no excess supply – in Warsaw and Tricity. On a y/y basis, a significant price increase concerned only the capital (+7.7%).

Record-breaking offer of apartments and growing pressure on developers

From the buyers' point of view, the situation has become extremely comfortable. At the end of 2025, the offer of apartments was higher than a year earlier in all analyzed metropolisesh. In Warsaw, approx. 17.5 thousand were available. premises (+11% y/y), in Łódź 11.9 thousand (+26%), in Krakow 11.5 thousand (+21%), in the Upper Silesian-Zagłębie Metropolis 11.2 thousand (+18%), in Wrocław 10.2 thousand (+13%), in Tricity 8.7 thousand (+21%) and in Poznań 8.2 thousand. (+6%).

It draws special attention from analysts a sharp increase in the number of ready, unsold apartments. According to JLL Polska, in the fourth quarter their number in seven markets increased by as much as 46%. kdk, to over 14,000, which is already 20 percent. the entire offer. In Kraków, Poznań and Łódź, the pool of ready-made premises accounts for 43-46 percent. annual sales, and in Katowice as much as 75 percent

— These are not the levels known from the crisis of 2012–2014, but with such a ratio to sales, liquidity problems may arise for some companies. – warns Aleksandra Gawrońska.

This is confirmed by the indicators of the theoretical sale time of the offer. While in Warsaw and Tricity the market remains close to balance, in Łódź we are talking about over two years, and in Katowice even almost four years needed to sell the current offer while maintaining the current demand rate.

Price war or new normality? Forecasts for 2026

There is more and more talk about a “price war”, although developers prefer the term “price flexibility”. Tomasz Kaleta, managing director of sales and marketing at Develia, emphasizes that the scale of the promotion depends on the specific market and location.

— We assume price stabilization in 2026 with a tendency to gradually increase, especially in large cities and the best locations – by 1-2% on average. above inflation, says Kaleta. At the same time it points to the growing importance of regulations such as general plans, new technical conditions or the potential obligation to build shelterswhich increase costs and lengthen the investment process.

Experts agree that mortgage loans will remain a key factor. Further reductions in interest rates may strengthen demand, but uncertainty in the labor market and relatively high financing costs will continue to be a drag. If demand does not accelerate, developers in oversupplied markets will be forced to further make their offers more attractive.

For buyers, this means one thing: 2026 may be one of the best moments of the last decade to choose an apartment – from a wide offer, with stable prices and real possibility of negotiations. For the development industry, it will be a test of the resilience of business models in a market that has moved from a boom phase to a phase of demanding balance.