The offer to use insurance is one of the most common situations when purchasing electronic equipment. Protection may be useful, but it turns out that the Financial Ombudsman is recording more and more complaints about electronics insurance. Only from January to October, clients submitted more cases to the Ombudsman's Office than in the entire year 2024. Complaints focus primarily on unclear definitions, refusals to pay for transport damages and misleading insurance sales.

A disturbing increase in complaints to the Financial Ombudsman

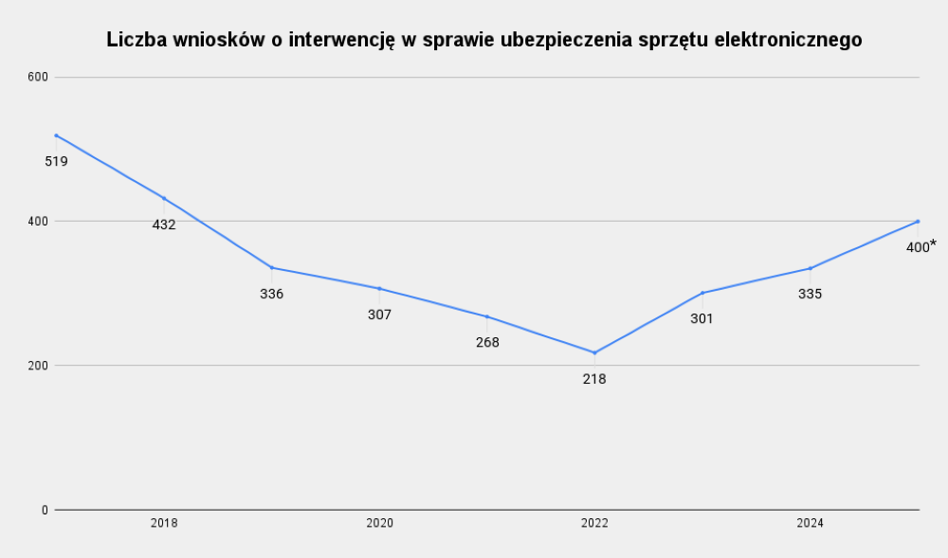

Statistics from the Office of the Financial Ombudsman show that: After several years of decline, the number of complaints about electronic equipment insurance began to increase. In 2017, there were 519 reports, and by 2022 there were fewer and fewer cases.

In 2025, by October, 341 applications for RF intervention had already been registered, and it is estimated that this number at the end of the year may amount to approximately 400 applications. The Financial Ombudsman notices a disturbing trend and announces actions to reverse it.

Advertisement

We notice a disturbing phenomenon of a renewed increase in the number of requests for intervention in matters relating to insurance of electronic equipment. After publishing the report in 2016 and the annex in 2019, as well as a number of activities and meetings with market representatives, we saw a strong downward trend until 2022. My goal is for the number of complaints to start decreasing again. Hence the appeal to entities operating in this segment to analyze procedures and processes – says Michał Ziemiak, Financial Ombudsman.

Numerous problems with electronics insurance

Consumer complaints result primarily from the structure of the General Terms and Conditions of Insurance (GTC) and problems in the claims settlement process. Reasons for making applications to the Financial Ombudsman include:

- Imprecise definitions and exclusions of liability,

- Refusal to compensate for transport damage,

- Insurers' refusal to specify the circumstances of the event,

- Treating a complaint about a defective repair as another damage,

- Misleading information when selling.

A separate group of reports concerned Apple equipment which, instead of being repaired, was replaced with recertified models, which was not mentioned in the General Terms and Conditions.

The mysterious “external factor”

Customer objections were already starting to arise at the stage of the electronics sales process itself. Employees reported that the insurance covers “all mechanical damage, unless it is intentional,” but omitted liability exclusions and definitions, notes Joanna Chmurska, an expert at the RF Office. Themselves The general terms and conditions were also not precisebecause the documents contained the terms “unhappy accident” and “external factor” which were not explained in a way that was understandable to the consumer. This leads to disputes with insurers who, for example, do not take into account events such as slipping the phone from your hand and refuse to pay benefits.

One of the reasons for complaints to the Financial Ombudsman were also the exclusions of liability of insurers, specifically transport damage. Customers pointed out that they had no knowledge of how the goods were packed, and there were situations when the equipment returned from repair damaged.

Faulty repair as further damage

Data from the Financial Ombudsman show that: Some customer reports concern repairs themselves, which often do not solve the problem and do not restore the equipment to operation. When a customer complains about a faulty repair, it is sometimes treated as a separate loss, as a result of which the insurance sum is reduced.

For example, a failure of the coffee grinder was reported, the damage was recognized, the service repaired it, but after receiving the equipment from the courier, the grinder still did not work. After the next return from the service, the equipment still did not work. Then the loss was classified as total, but in the settlement the owner was not paid the entire sum insured in the policy, but only a small amount – indicating that the sum insured for previously performed servicing activities had been exhausted. – adds Joanna Chmurska from the Office of the Financial Ombudsman.

Problems also occurred when settling damage to electronic equipment at services indicated by insurers. In accordance with the Civil Code, the insurance company itself is responsible for the quality of the repair, because it affects the content of the service provided to the customer.

Insurance of electronic equipment only in case of accidental events

If we decide to buy insurance when purchasing electronics, it is worth making sure what its scope is and who provides protection. Stores offer various products here, calling them e.g. screen protection, extended warranty, etc., but only those in which the insurance company is a party to the contract can be called insurance. The policy can protect the equipment against accidental damage, overvoltage and even theft, but what matters is what is included in the General Terms and Conditions and what are the exclusions of liability.

The practice of the Financial Ombudsman shows that electronics insurance is not a cure-all, because insurers often refuse to accept the claim, e.g. justifying the decision by saying that the consumer could have predicted that an accident would occur. Before using above-standard protection – often quite expensive – it is worth familiarizing yourself with its terms and conditions, otherwise instead of greater peace of mind, you will only gain more problems.

The publication contains affiliate links.