They are introducing an offer without “stars”. UniCredit throws down the gauntlet to Polish banks

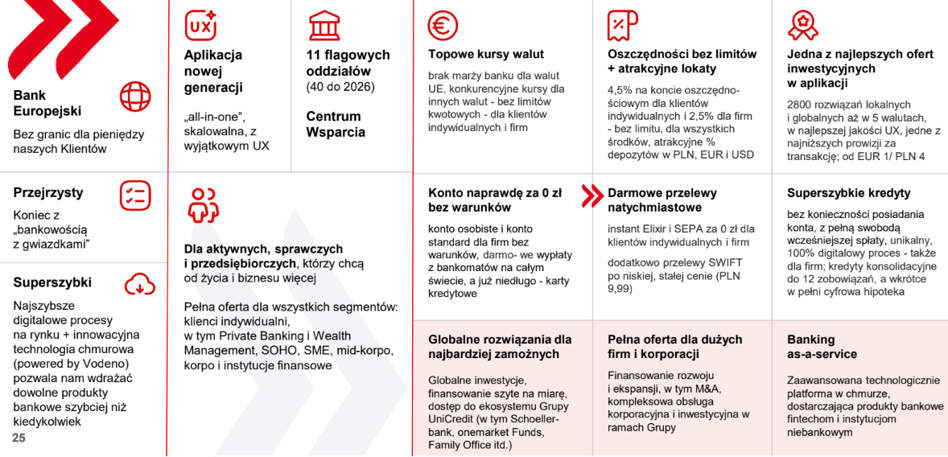

The UniCredit Group returns to the Polish retail banking market and wants to redefine the rules of the game. Bank representatives claim that the current banking model based on “stars” is a thing of the past. That's why the new bank is introducing a free account, debit card, ATMs in Poland and around the world, as well as instant and SEPA transfers. This is a permanent offer, not a promotion.

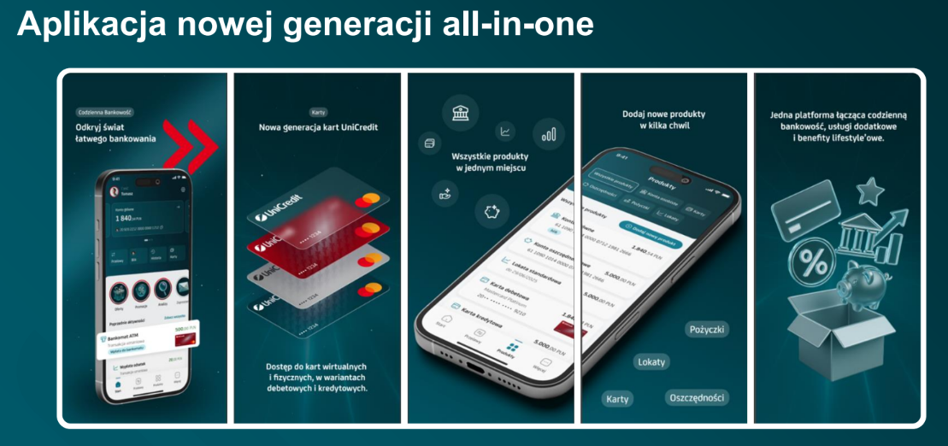

Yesterday, the bank presented its offer to journalists and revealed some of its plans for the future. UniCredit wants to use Poland as one of the key places to build a “bank for the future of Europe”. In practice, this means combining a fast, extensive mobile application with the resources of a large, pan-European group. The bank is launching as an element of a broader project that will ultimately cover many markets.

The supervisory board of UniCredit is headed by Wojciech Sobieraj – a visionary and one of the most experienced managers on the market. Let us remember that he was the one who founded Alior Bank “from scratch” years ago and was responsible for its success in the first years. At that time, he also proposed solutions that were not standard on the market. Today he says directly that the current model of price lists in Polish banks is a relic. That's why he turns the table over and makes a “new opening”.

The price list “shines” with zeros

At the conference, it was emphasized that UniCredit wants to move away from the “banking with stars” model, in which the slogan “zero account” in practice means several conditions hidden in the table of fees. A permanent “zero” fee for basic services is to be one of the pillars of the offer both in the retail segment and for the smallest companies. Maintaining an account, payment card and ATM withdrawals in Poland will be free of charge, without the need to ensure a specific monthly receipt or perform several card transactions. The price list also includes zeros for the items: instant and SEPA transfers. UniCredit also declares that it will not add its own margin for card transactions in EU currencies, and in the application it offers competitive exchange rates without any amount limits.

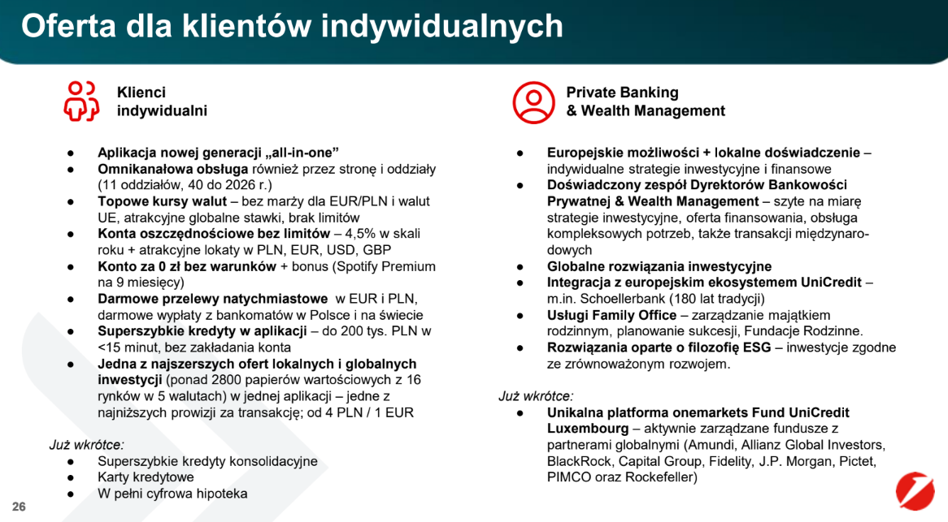

However, the proposal does not end there. The application can be used like a typical personal account, but also as a tool for saving, currency exchange and investing. UniCredit offers savings accounts with no limit – 4.5%. for individual customers and 2.5 percent for companies – regardless of whether they are new funds or money already deposited. There are also no deposit limits. Additionally, there are deposits in Polish zloty, euro, dollars and pounds. This part of the offer is addressed to people who keep savings in different currencies or plan larger foreign expenses.

Extensive investment offer

The second pillar is to be a simple investment opportunity. One application provides access to over 2,800 shares and ETF funds from Poland and foreign markets. Trade is to take place in five currencies, which allows combining Polish and foreign companies in one portfolio. The bank announces low commissions – from PLN 4 or EUR 1 per transaction – and further development of the investment offer, including making available to clients the pan-European Onemarkets Fund platform operating in the UniCredit Group. The goal is for a client who today uses separate brokerage applications to be able to transfer most of their investment activities to one tool.

Loans are also an important part of the project. Individual customers will be able to take out financing fully online, without the need to have a UniCredit account first. The application will offer quick cash loans, and for people repaying several liabilities – consolidation of up to 12 loans from other banks. In the corporate segment, the bank offers both classic financing of current operations and investment loans for small and medium-sized enterprises, also in a simplified, digital process.

The new institution is not limited to the retail segment and micro-enterprises. Right from the start, it also addresses its offer to wealthy clients within Private Banking and Wealth Management, as well as to medium and large companies. To these groups, UniCredit offers transaction advice, financing of infrastructure and real estate projects, and support in mergers and acquisitions. Polish enterprises will thus gain access to the corporate and investment banking ecosystem used by companies in Western Europe.

Faster and more efficient

In conversations with journalists, bank representatives repeatedly emphasized the pace and speed of implementation. Everything happens here just like in fintech – what takes years in traditional banks is created in UniCredit in just a few months. The cloud platform developed together with fintech Vodeno plays a key role. It is intended to enable the rapid implementation of new functions and products, as well as – in a broader perspective – the transfer of solutions developed in Poland to other markets where the Group operates.

Although the center of communication is a zero-cost account, the management's statements show that this is only the beginning of the project. In response to questions from the audience, the bank's representatives announced the development of the insurance offer, which is to appear in the application at the beginning of next year, and further expansion of the investment part. Ultimately, the customer will be able to manage daily payments, savings, investments, financing and insurance in one place, without having to use several financial institutions. By the end of the first quarter, there should also be an offer of accounts for younger customers, IKE and IKZE, and soon mortgages.

The construction of a network of branches begins

In addition to digital channels, UniCredit is also building a classic branch network. There are 11 branches at the start, and by 2026 their number is expected to increase to approximately 40. Some are to be established in smaller cities, which is intended to make it easier to reach customers who prefer personal contact with an advisor. At the same time, the bank emphasizes that digital processes will be crucial even in branches, so that most matters can be resolved quickly, without unnecessary paperwork and repeating the same data on various forms.

In the background of the launch of a new bank, a natural question arises about how the “zero” for the account, card and ATMs is financed. UniCredit representatives argued that waiving basic fees should be a permanent element of the business model, and not at the expense of a short-term marketing campaign. The source of revenue will be primarily loan margins, investment services and additional products, some of which will only be added to the offer. The bank announces a simple, transparent table of fees, so that the customer knows in advance how much he will pay for less frequently used operations. For a market where both fees and the complexity of price lists have increased in recent years, the appearance of an institution declaring a permanent “no stars” offer is a clear competitive signal.

Wojciech Sobieraj, to illustrate the new rules of the game, compared the new bank to a supermarket. The customer should not have to pay for the mere fact of being a customer, i.e. for parking in front of the store. He also recalled the case of Alior Bank, which caused quite a stir on the market by offering all ATMs for free during its debut and changing the status quo of the sector at that time. However, the head of the supervisory board avoided answering about sales goals – now the bank has only a few thousand retail customers, and an advertising campaign, which will start any moment, is to help with the acquisition.

Something finally moved

UniCredit's entry into Poland is one of the largest foreign banking initiatives in recent years. From the customers' perspective, however, what matters less are declarations of European scope and more what everyday use of the account will look like. If the announced “zero-cost account, card and ATMs” and the transparent fee structure actually hold, the new player may force the competition to review their offers and the way banks in Poland price basic services.

It is also worth paying attention to one more issue. UniCredit is another institution that has been entering the Polish market in recent months with a completely new approach to the customer. Recently, the German bank Trade Republic announced a revolution. Instead of screwing up price lists and sewing asterisks into them, new banks focus on low prices and transparent, multi-page tables. You don't need a PhD in banking to understand them. And all this is happening on the eve of the Erste group's debut. It is possible that Polish retail banking will experience a greater revolution and a change in approach to customers in the coming months.