The European real estate industry is entering 2026 with a clearly changed mindset. According to the Emerging Trends in Real Estate Europe 2026 report prepared by PwC and ULI, the dominant tone has shifted from cautious optimism towards pragmatism. The reason is growing concerns about the effects of deglobalization and escalation of conflicts.

The percentage of market leaders concerned about deglobalization has more than doubled in two years – to 70%. As much as 90 percent respondents point to growing political instability, 86 percent to the escalation of global conflicts, and 77 percent to Europe's poor economic growth prospects. As a result, the level of business confidence dropped to 45%. compared to 50 percent a year earlier, although expectations of improved profitability by the end of 2026 increased from 46 to 50 percent.

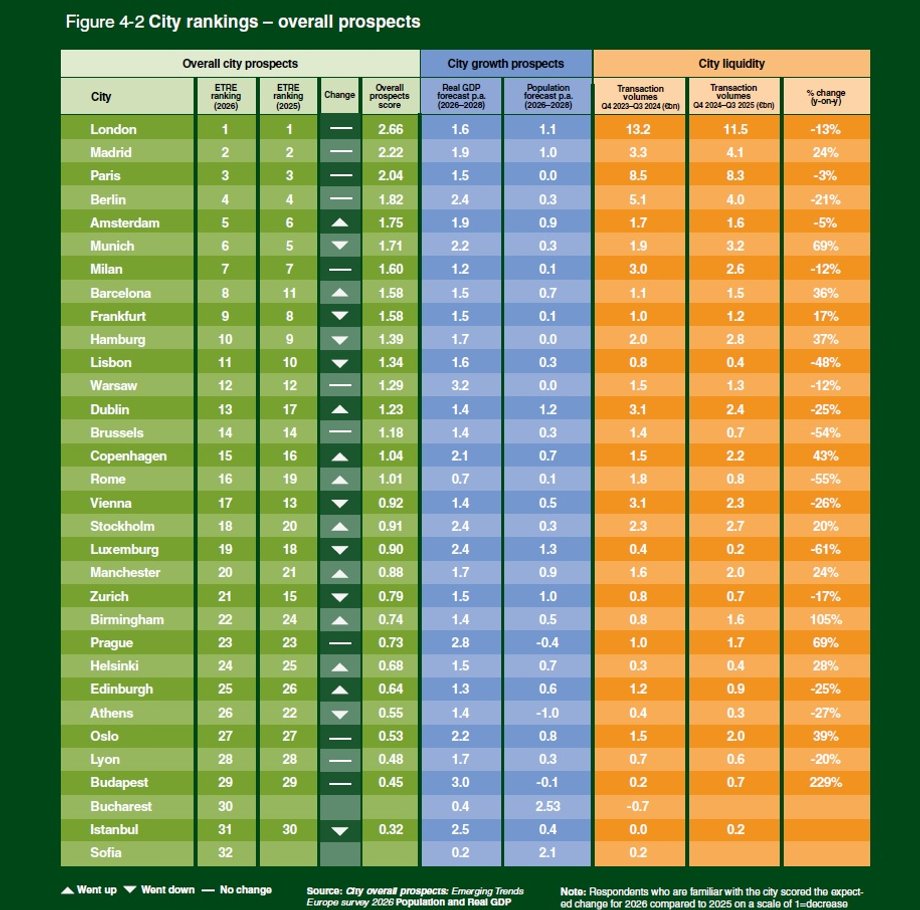

ULI ETRE 2026 – general city ranking

|

ULI

See also: The Swiss franc is losing importance. Loans in euro dominate the market

Uncertainty affects how capital is allocated. In an environment of high interest rates, real estate competes with bonds and infrastructure. An increasing part of capital chooses the “debt path”, offering a better risk-return ratio than equity investments. The share of private equity funds and family offices, which are looking for opportunities in segments with stable foundations, is also growing.

— This year's report shows a picture of a resilient industry that continues to face recovery uncertainty and a variety of operational and investment challenges – comments Simon Chinn, vice president of research and consulting at ULI Europe. “The mood of leaders has shifted towards a more practical approach, adapted to current market conditions,” he adds.

AI and ESG – between innovation and regulatory pressure

Technological transformation is becoming one of the key trends in the industry. The report shows that 75 percent respondents already use solutions based on artificial intelligence (51% a year earlier). Over the next 18 months, most plan to implement AI in marketing and leasing (90%), real estate management (87%), design (84%) and asset management (86%).

The rest of the article below the video:

AI is changing the way real estate is managed – from automating leasing processes to predictive analysis of maintenance costs. Combined with the growing role of data and digitalization, technology becomes a tool for building competitive advantage.

Simultaneously ESG remains high on the agenda, although its perception is evolving. 85 percent survey participants consider ESG to be important, but the percentage of those treating it as a key decision-making factor in the next five years dropped from 40 to 21 percent. Criticism of excessive regulations and bureaucracy is becoming more and more common. “Asset managers need to more clearly demonstrate the links between ESG and investment value,” the report's authors emphasize.

Kinga Barchoń, leader of PwC Polska Real Estate, adds: – 2025 was a transitional period – adaptation to the environment of lower interest rates and the search for a new price balance. In Poland, investment volumes rebounded in 2024 after a sharp decline in 2023.which signals the return of liquidity, albeit in a selective manner, he says.

Read also: Instead of a rental apartment, invest in REITs. Receive “rent” from the exchange without an apartment [DOCHÓD PASYWNY]

Warsaw – a stable point in the region and a leader in nearshoring

Poland was once again identified as one of the most resilient markets in Central and Eastern Europe. Warsaw maintained 12th place among 32 cities analyzed in terms of investment attractiveness, ahead of Prague and Budapest. — Warsaw is strengthening its position as the most mature investment market in the region, combining stable economic foundations with growing institutional maturity, says Marcin Juszczyk, chairman of ULI Poland.

The capital's advancement from 16th place in 2022 to 12th in 2024 is proof of its lasting presence at the European forefront. Poland was recognized as the “most liquid and open market” in the regionwhich means the highest level of transparency and accessibility of transactions. The lack of oversupply of new space, stable demand in housing and the development of the warehouse segment create solid investment foundations.

As Juszczyk emphasizes, Warsaw is also becoming a beneficiary of the nearshoring trendu — relocation of production and logistics from Asia to Europe. More and more companies choose Poland thanks to favorable energy costs, availability of qualified labor and developed infrastructure. This makes the capital gain the rank of a regional investment center, attracting capital in the sectors of logistics, production, apartments for rent and energy transformation projects.

Importantly, In the office segment in Warsaw, we observe an owner's market — limited new supply and persistent demand are leading to upward pressure on rents, especially in prime locations. — Importantly, large tenants start renegotiating contracts even three years before their expiry date – a phenomenon that we have practically not observed before – notes Marcin Juszczyk. — There is no immediate acceleration in new supply on the horizon, so this trend is unlikely to reverse in the next three to four years. This shows that the office market has entered a phase of high predictability and strategic planning on the part of tenants, he sums up.