2025-11-06 22:08

publication

2025-11-06 22:08

Thursday's session on the New York stock exchanges ended with severe declines in the main indexes. The biggest sell-off was the shares of large technology concerns, whose valuations have reached absurdly high levels in recent months.

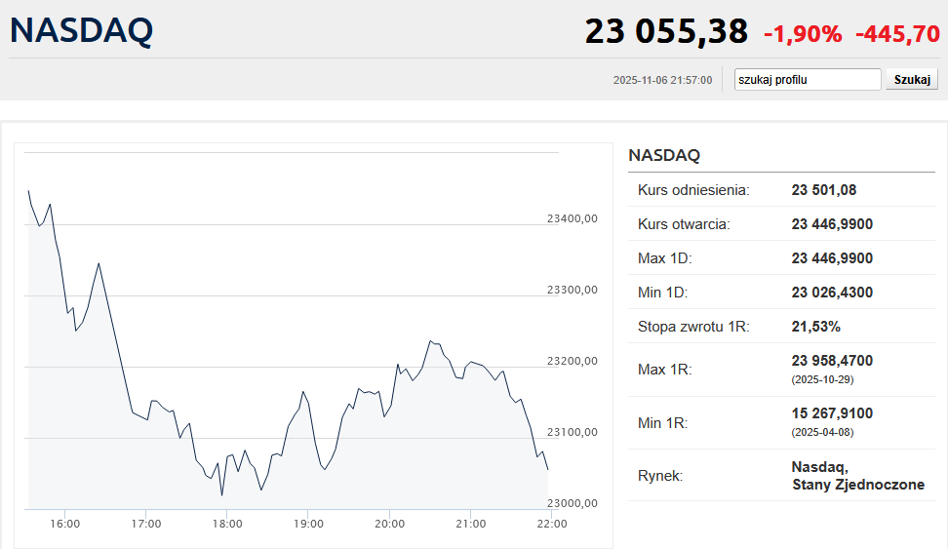

The Nasdaq Composite ended the day with a decline of 1.90% and a level of 23,053.99 points. The S&P500 gave up 1.12% and stopped at the line of 6,720.32 points. Dow Jones fell by 0.84%, finishing with 46,912.30 points. The VIX volatility index increased by over 9%, although it remains quite low – it still does not even exceed 20 points.

It was basically a continuation of what we saw on Tuesday, when the first such “severe” accusations about the creation of a speculative bubble in the AI sector appeared. Although on Wednesday it seemed that these fears were exaggerated, on Thursday they returned with a vengeance. Thus, Nvidia's shares were devalued by 3.7%, Meta's by 2.7%, Palantit's by as much as 6.8%, and AMD's by over 7%.

“From a valuation standpoint, many stocks have been so overpriced and priced to perfection that we're seeing a bit of a dichotomy in the market between companies that are beating and growing, and those that are maybe beating that mark on revenue but are offering mediocre earnings or operating profit guidance,” said Mike Mussio, president of FBB Capital Partners.

– We went through a period of very rapid growth in valuations, which concentrated on a few individual assets. Now we see indecision and capital flows between high-volatility stocks and “safe” low-volatility stocks, said Michael Green, chief strategist at Simplify Asset Management, quoted by Reuters.

Additionally, the sentiment was worsened by statistics from the American labor market. The Challenger survey found almost three times the number of announced layoffs in the corporate sector in October than in September. According to Challenger, Gray & Christmas, in October the number of layoffs amounted to over 153,000, an increase of 175%. higher than in the same period a year earlier. This is the highest level recorded in October in 22 years, in a year that is shaping up to be the worst for job losses since 2009.

A day earlier, the market received only a slightly better than already low expected ADP report and a very weak ISM reading for the manufacturing sector (on Monday). Therefore, it is difficult to claim that the world's largest economy is in great shape.

Reports from the US Supreme Court, which is considering the legality of tariffs imposed by President Trump's administration, also raise concerns. If these decisions were found to be unlawful, it would force the US government to issue refunds of the collected duties, which would increase the already huge fiscal deficit and public debt.

However, the season for publishing results for the third quarter is coming to an end – 424 companies from the S&P500 index have already presented reports. The results turned out to be sensationally good. The estimated annual growth rate of corporate profits attributable to the S&P500 was 16.8% and was more than twice as high as the 8% expected at the beginning of October. So, at least in this respect, the market has little reason to worry. However, the third quarter is history and now investors are discounting the results that listed companies will deliver in 2026.

K.K