Türkiye is lowering interest rates in October 2025. However, it has still not dealt with inflation

publication

2025-10-23 13:00

The Turkish central bank has already cut interest rates for the third time in this cycle. And although the interest rate on loans on the Bosphorus is one of the highest in the world, price inflation remains almost equally high and persistent.

The benchmark interest rate of the Central Bank of the Turkish Republic (TCMB) was reduced today by 200 basis points to 39.50%

compared to 40.50% applicable so far. This decision was in line with the expectations of most economists. The so-called the market consensus assumed a reduction to 39.50%.

– The restrictive monetary policy stance will be maintained until price stability is achieved. (…) The Committee will set the interest rate taking into account actual and expected inflation and in such a way as to ensure the appropriate restrictiveness required to maintain the projected disinflation path within the medium-term target, the Central Bank of Turkey wrote in an October statement. TCMB's inflation target is 5% (in words: five percent).

Formally speaking, this was the third consecutive interest rate cut in Turkey in the current cycle. The first one took place in July, when TCMB made a reduction of 300 bps. The second one appeared in September and amounted to -250 bp.

However, the TCMB started to ease monetary policy as early as late December 2024, when it lowered the monetary policy rate from 50% to 47.5%. Further cuts took place in January (up to 45%) and in March (up to 42.5%). But in April, the Turks unexpectedly raised their interest rate to 46%.

How the Turks fought galloping inflation

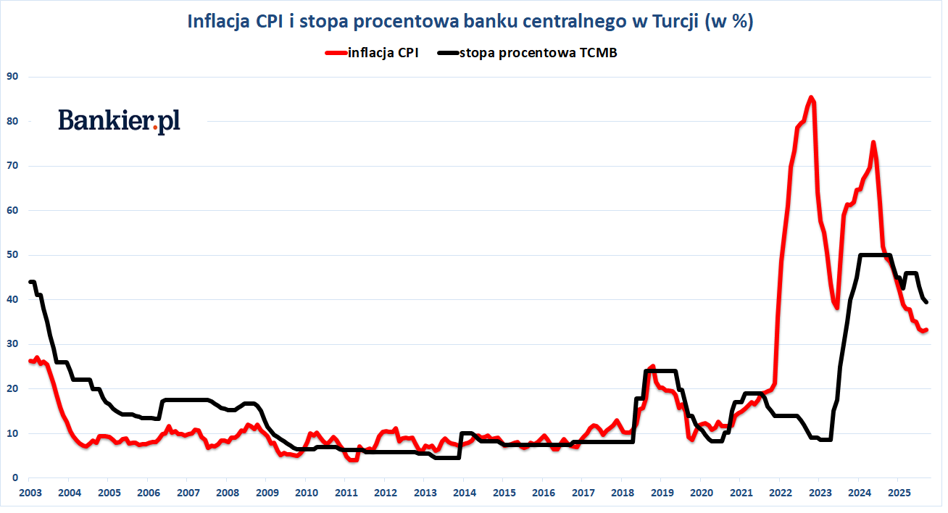

Previously, for 9 months of 2024, TCMB maintained one of the highest nominal interest rates in the world, at as much as 50%. This was the highest level of interest rates in Turkey since 2002. It was the last chord in the fight against galloping inflation, which at that time reached up to 75% (at least officially. Unofficially, there was talk of three-digit values).

Such high inflation was the result of President Erdogan's absurd policy and unfavorable global conditions. The Turkish satrap believes that high interest rates are driving price increases, which is why he does not agree to increase them. He removed disobedient bankers, ministers and statisticians from their positions. Taking advantage of the temporary stabilization of inflation – at the level of approximately 20%. – in the second half of 2023, the local central bank even reduced the “price of money”: from 19 to 14 percent. This resulted in an increase in official CPI inflation from less than 20% to 85%.

It was only two years ago that the Turks came to their senses and appointed a new head of TCMB, who dared to break with “erdoganomics” and drastically raised interest rates. Then the reference rate went up from 8.50% to 15.00%,

which was still a level clearly lower than the 20-25% expected by the market. In a year and a half, TCMB reached 50% with interest rates.

Under the influence of such a sharp tightening of monetary policy, CPI inflation in Turkey dropped from 75.45% in May 2024 to approximately 33% recorded in the previous three months. These values are still outrageously high and have little to do with “price stability” understood in any sense. But at the same time, it is worth noting that the current central bank interest rates are several percentage points higher than the official CPI inflation for the previous 12 months. Therefore, real interest rates in Turkey (calculated ex post) are positive and relatively high.

However, this does not change the fact that the Turkish lira is still in free fall, almost constantly depreciating against the US dollar. Currently, the price for a “green” one on the Bosphorus is almost 42 lira, compared to just over 35 lira at the beginning of January. Only by the beginning of 2025, the Turkish currency has weakened by almost 16%, losing 16.5% last year and 36.5% in 2023. Over the last 5 years, the Turkish lira has lost 81% of its value against the dollar and has been depreciated by 93% over the last 10 years.