After the recent controversy carried on Facebook by the Liberal Ciprian Ciucu with Social Democrat Victoria Stoiciu on the subject of education made by Minister Daniel David, the former professor of the two coalition colleagues, Cristian Pîrvulescu, with a text published today by HotNews.

To deliberately hold the Romanian state below the functional financing threshold is not a responsible reform, but an ideological option, anchored in fiscal dogmas that have already proved their limits in other contexts. Such an approach not only undermines social cohesion and economic development capacity but also vulnerabils critical infrastructure, essential public services and institutional resilience.

1. The facts

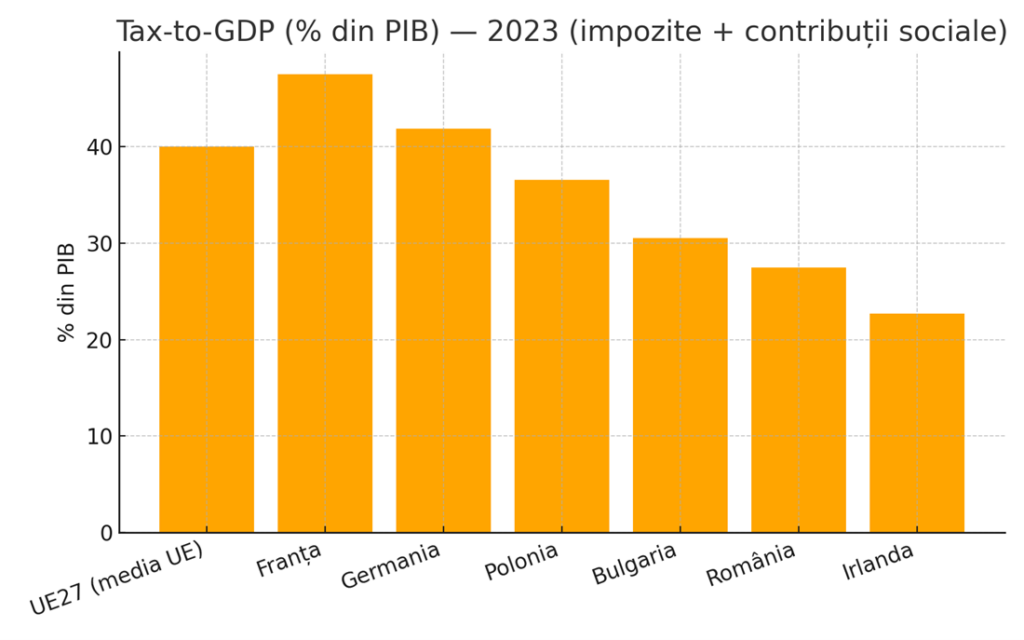

Romania currently has a level of fiscal income and social contributions of about 27.5% of GDP. The average of the European Union is around 40%, and the countries with robust economies are significantly above: France has about 47.5%, Germany 41.9%, Poland 36.6%, Bulgaria 30.5%. Only Ireland appears below us, with 22.7%, but its case is an exception with specific causes. The political target of 27% means the freezing of Romania at the tail of the Union and the perpetuation of a chronic subfinence of public services. In an economy like ours, every percentage point cut from fiscal revenues means billions lost annually for education, health, infrastructure and defense.

Graphic: tax-to-gdp, % of GDP, 2023-Romania vs. EU average, selected countries (source: Eurostat / European Commission)

But Romania does not naturally reach a level of 27% of GDP in terms of tax revenues but due to a deliberate political choice. This decrease occurs only when the government decides to reduce the share of taxes and contributions in the economy. The mechanisms by which this dissident was made are clear: reducing taxes (either VAT or income tax), extending exemptions and fiscal facilities for more and more categories, maintaining a low degree of collection through the lack of investments in the modernization of the tax administration and, last but not least, the increase of the nominal GDP.

According to the IMF data for 2023, the total revenues of the public administration in Romania represented 31.01% of GDP. This value includes both tax income (tax-to-gdp), as well as non-fiscal income (dividends, royalties, administrative taxes, European funds).

Normally, in the analysis of the fiscal capacity of a state, the budget made from taxes and taxes (Tax-to-GDP) is used, not the total revenues, because it directly reflects the state-ket fiscal relationship. Non-fiscal revenues (eg dividends, royalties) are more volatile, can be short-term and do not ensure the long-term structural basis for state financing.

The reasoning used in this demonstration is simple: even if we currently have 31% of GDP total (according to the IMF), if the fiscal policy reduces the main component (taxes + contributions) to 27% of GDP, the financing base becomes insufficient, and the difference up to 31% is not stable or guaranteed year by year.

The reduction to 27% of GDP would mean a decrease of 4 percentage points. At an estimated nominal GDP for 2024 of 1.766 billion lei ($ 403 billion according to the same source, IMF), the annual loss would be about 70.6 billion lei. This amount is equivalent to almost the entire education budget or two -thirds of the entire amount dedicated to health. If we design this policy in the medium term, with the increase of the nominal GDP, the annual loss could reach in 2025 to about 100 billion lei, money withdrawn from essential investments for the development of the country.

2. How to reduce fiscal capacity to reduce national interest

The intentional reduction of the fiscal capacity of the state, in a crucial historical context, is equivalent to a deliberate restriction of the means by which Romania can defend and promote its national interest. The specialized literature shows that the level of public income is not only an accounting indicator, but reflects the social contract between the state and the citizens (Musgrave, 1959; Stiglitz, 2015). On the other hand, according to the theory of public finances, a reduced fiscal capacity limits not only the supply of public goods, but also the resilience of the state in front of the external shocks (Besley & Person, 2011).

Under the current conditions, with a war on the border, energy transition, inflationary pressures and historical infrastructure gaps a share of fiscal income of 27% of GDP would place Romania in the area of structural vulnerability described by the IMF and OECD, where the state cannot sustainably support investments in human capital and critical infrastructure Revenue Statistics2023). Comparative studies show that savings with tax-to-gdp Under 30% tend to have underfinite public systems and increased external funding dependence, which reduces decision -making autonomy (Pricard, 2016).

Keeping below the 30% threshold does not mean a “supple and efficient” state, but a weak-institutionalized state, in the sense of Fukuyama (2014), that is, unable to exercise its fundamental functions without resorting to ad-hoc measures or politically conditioned resources. In addition, the ratio between fiscal capacity and social cohesion is extensively documented: a low level of public revenues perpetuates inequalities and fragmented the social contract (Boix, 2003; Acemoglu & Robinson, 2012).

Therefore, the deliberate reduction of the budget to 27% is not only an economic choice, but a strategic option with cumulative negative effects on sovereignty, democratic stability and development capacity. In the logic of the theory of the developing state (Evans, 1995), without a robust fiscal basis, Romania risks remaining in a “vicious circle of underdevelopment”, where the underfinancing of the state produces economic underdevelopment, which in turn limits the ability to increase public income.

3. The myth “Economy depends on the private sector”

The argument that “the economy depends on the private sector” does not resist a serious analysis. The private sector depends, in fact, on a state capable of forming competent graduates, building and maintaining modern infrastructure, ensuring a stable legal framework and security. The countries in which the prosperous business environment have a well -funded state, with revenues between 40 and 50% of GDP, not a minimal state.

As for Ireland, the example is misleading. His GDP is artificially swollen by the profits of multinational relocated there, a phenomenon known as “leprechaun economics”.* In relation to the gross national income (GNI- Gross national incomean adjusted version used by Ireland, which excludes artificial statistical effects, such as multinational transfers), the actual taxation level is much higher. In addition, Ireland benefits from an extremely productive economic base, with peak sectors such as information and communications technology or the pharmaceutical industry, which allow high revenues per capita, which allows the financing of quality public services and with an apparently low percentage of GDP.

As Paul Krugman explains, “most of what we see is, in fact, a statistical illusion: corporations use transfer prices, allocation of intangible assets, etc. to make profits appear to appear in low taxes; but there is very little real production or employment behind these profits”The New York TimesJune 15, 2018).

If Ireland has not actually attracted so much real capital, how to explain the high growth rhythms of the glory years of the “Celtic Tiger”? The answer, says Krugman, is that “much of this growth is not real: it is the savings of the spirits, in which the strategies for avoiding taxes produce a fictional growth.” In other words, much of the spectacular growth of the Irish GDP comes from tax optimizations and artificial reports, not from productive investments in the economy.

Krugman also emphasizes that “the vision of a global market in which the real capital moves much in response to the levels of taxation is completely wrong; most of what we see as a reaction to the tax differences is the transfer of profits, not the real investment.” Even though Ireland has benefited from certain advantages from attracting companies, the effects on real wages and production are not at the level suggested by “paper” productivity. It is a model built in decades, which cannot be replicated in an economy as that of Romania where such a level of taxation would mean the severe underfunding of the fundamental functions of the state.

Conclusion

To deliberately hold the Romanian state below the functional financing threshold is not a responsible reform, but an ideological option, anchored in fiscal dogmas that have already proved their limits in other contexts. Such an approach not only undermines social cohesion and economic development capacity but also vulnerabils critical infrastructure, essential public services and institutional resilience. In a context marked by geopolitical tensions, accelerated technological transitions and massive investment needs in human capital, the choice to intentionally clarify the budgetary income below the minimum operating level is equivalent to giving up the instruments by which the state can protect the strategic interests of the company.

The deliberate maintenance of taxation below the functional threshold is not only a technical option, but the expression of a cultural-institutional configuration that weakens the state's ability to deliver public goods and to protect their citizens. In such a framework, the restrictive fiscal culture and the weak institutions self-clarify, reducing the resilience of the society and blocking the adaptation to major shocks. From this perspective, the ceiling of public revenues becomes not only a policy error, but a risky bet on the structural and long -term fragility of the state.

*Text initially published on contributors.

* Leprechaun economics (Let's translate the term as the economy of the spirits) is an ironic expression launched in 2016 by Paul Krugman, Nobel laureate for the economy, to describe how Irish GDP statistics have been massively distorted by relocating multinational corporations. This expression synthesizes the absurd situation reported in 2015 by the Central Statistics Office of Ireland, which reported an economic growth of 26.3% in a single year. However, this “economic explosion” did not reflect a real increase in domestic production, but to move some assets and legal offices of some multinational companies to benefit from the advantageous fiscal regime on the emerald island.

Selective bibliography

Musgrave, RA (1959). The Theory of Public Finance

Stiglitz, J. (2015). The Great Divide.

Besley, T., & Persson, T. (2011). Pillars of Prosperity.

OECD (2023). Revenue Statistics (https://www.oecd.org/en/publications/2023/12/revenue-statistics-2023_6ee814f4.html)

Prichard, W. (2016). Taxation, Responsiveness and Accountability in Developing Countries.

Fukuyama, F. (2014). Political Order and Political Decay.

Boix, C. (2003). Democracy and redistribution.

- Acemoglu, D., & Robinson, J. (2012). Why nations fail (in Romanian, Why do nations fail. The origins of power, prosperity and poverty, The letter, 2018)

- Acemoglu, D., & Robinson, J. (2024). Culture, Institutions and Social Equilibria: Of Framework.

EVANS, P. (1995). Embedded Autonomy: States and Industrial Transformation.

Krugman, P. (1918). Tax Cuts and Leprechanes (Wonkish)