2025-04-10 22:04

publication

2025-04-10 22:04

After one day of euphoria, the depression related to the consequences of the customs wars of President Trump returned to Wall Street. The situation, however, is dynamic and in 24 hours we can as well see the traffic the other way.

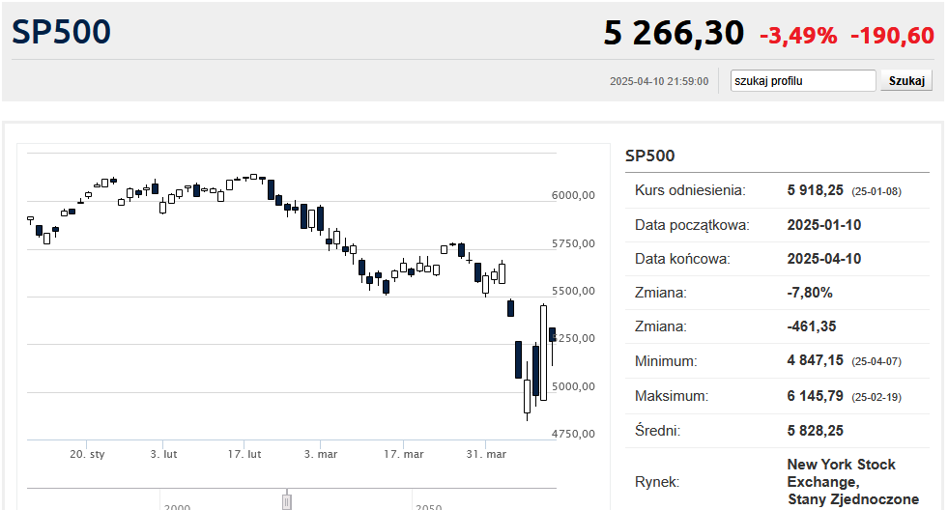

Normally you would read about strong declines, “dramatic discount” or “breakdown” on New York stock exchanges. But by standards from the last few days it was a day like every day. The S & P500 index ended with a 3.46%decrease, descending to level 5 268.05 points. Nasdaq has lowered by 4.34%, lowering to 16,387.31 points. Dow Jones scored a decrease by 2.5% and was at the ceiling of 39 593.66 points. And so anyway results after the upward end of Thursday trade, during which all these three indexes gained about 1%.

Paradoxically, it was a fairly calm session. At least by the standards of April AD 2025. After all, on Wednesday, Wall Street found itself in euphoria and Nasdaq gained over 12% after President Donald Trump under market pressure and business, however, decided to suspend the introduction of customs by 90 days. Already on Tuesday, the market tried to reflect, but without success. On Monday, he also hoped for relaxation, but it burned on the acetabulum. It happened after the S&PC fell on Friday by nearly 6% and last Thursday by almost 5%.

This Thursday, investors estimated that the glass is half empty. It is true that the high duties on the countries of Europe and Asia have been suspended for three months, but already prohibitive 145 % tariffs to China entered into force. Beijing says that he does not want a trade war, but he will not talk to a accurate pistol attached to the temple. The European Union agreed for a 90-day customs. At the same time, the US administration is conducting talks with 15 countries on new trade and customs contracts.

Therefore, the situation does not look as dramatically bad as at the beginning of the week, but the customs war between the two largest economies of the world has just become a fact. Exchange analysts began to browse statistical tables of foreign trade and discovered in them that Americans export to China mainly … raw materials. The largest export hit of the USA in the Middle Kingdom is soy, and in addition natural gas, oil or copper scrap. The list also includes semiconductors, vaccines (!), Car parts or medical devices.

A much bigger problem is what America brings from China. Here the list is opened by smartphones, computers, “various goods”, batteries, car parts, toys, art. Lighting, furniture, plastics and others. The list of these two lists makes you doubt that the US is a technological leader here. What's more, apart from soy and medical goods, none of the American export hits is the main source of supply for the Chinese.

It is also worth noting that New York stock exchanges have recorded substantial declines despite the very good CPI inflation results. This indicator in March recorded the first inheritance in 5 years in a monthly relationship (i.e. by 0.1% MDM), and its annual dynamics slowed down from 2.8% to 2.4%. The lowest in 4 years was also base inflation, which decreased from 3.1% to 2.8%. This can give hope that in the event of a recession, the federal reserve will be able to afford deeper reduction of interest rates. However, everyone knows that the data for March is the past and in the way there are significant increases in prices of goods imported from China, Canada and Mexico.

The second good (i.e. it depends for whom) the message of the Thursday session was the re -discount of oil. Brent raw material made up by 3.3%, and Texan WTI oil by 3.8%. This is not only a disinflary factor, but above all relief for consumer portfolios and producers' costs in Western countries. However Since it's so good, why was gold the second day in a row was about $ 100 on the ounce – by 3%?