After 20 years, WIG20 is fighting for its historic maximum. The celebration will be bittersweet

It was the beginning of 2003, when the stock indices on the Warsaw Stock Exchange – after falls caused by the burst of the dotcom bubble on the American stock exchange – started to climb up. The macroeconomic situation was favorable for the Polish economy, forecasts were good (including due to joining the European Union in May 2004), and interest rates were falling. These are good conditions for improving company results and share prices. The global economic situation was also very good.

The four-year-long boom pushed up the indexes on the Warsaw Stock Exchange, and sellers in TFIs could boast of high rates of return, which attracted further capital inflows to the funds and only increased the valuation of companies on the Warsaw Stock Exchange. Although in the summer of 2007 the first signs of the upcoming global financial crisis were already appearing overseas, WIG20, an index grouping the 20 most liquid companies on the WSE (usually the largest companies in terms of capitalization), reached its peak on October 29, 2007. It then reached 3,940.5 points, which meant an increase of 235%. for four years.

To this day, the WIG20 has achieved this result – despite the ongoing bear market at ul. Książęca from autumn 2022, during which this index gained 175%. — failed to beat. WIG20 lost a lot during the financial crisis of 2008-2009, reaching a low of 1,253 points in mid-February 2009, which meant a decline from the peak by as much as 68 percent, which is more like a failed investment in a single company rather than in the main stock exchange index of a medium-sized European country.

But now there's very little missing: counting from Monday's closing – when WIG20 lost 0.9%. and amounted to 3666.9 points – the index of Polish blue chips would have to increase by 7.5% to equal the previously elusive record from 2007.

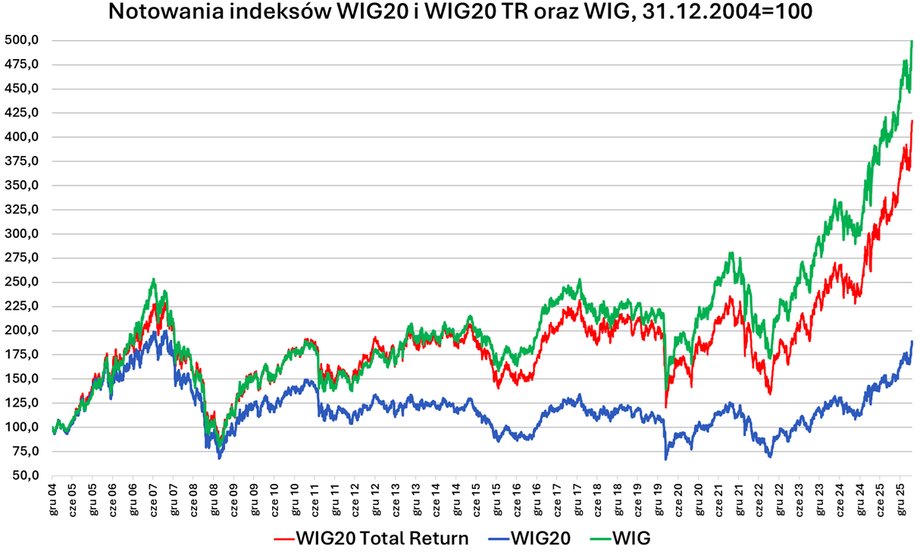

Let us remind you that WIG – the broad market index – is already several levels higher than its 2007 peaks. Although it also needed a lot of time to break this ceiling. In January 2018, it slightly exceeded the record recorded just before the global financial crisis, but still exceeded 70,000. points had to wait until the end of August 2021. And although the following months were very difficult – the outbreak of the war in Ukraine in 2022, the increase in inflation and interest rates, the flight of capital from shares and emerging markets, WIG returned to form quite quickly and from the fall of 2022 it began its upward march and a series of records: 100,000. points broke in April 2025, and last Friday the index reached a new peak at just over 135,000. points, i.e. it has gained 110 percent since the record in 2007.

WIG20 is very different from WIG. Key dividends

How is it that WIG is more than twice as high as in the fall of 2007, and WIG20 is still struggling to equal its record? The main reason is the difference in the methodology of both portfolios. WIG20 is an index pricing (i.e. only changes in company share prices are used for its quotations), and WIG profitable (i.e. its quotations include dividends paid by companies).

See also: How to safely earn dividends? A new instrument may be helpful

In other words: if a given company pays a dividend, when the right to dividend is cut off, the price of its shares is reduced by the value of the profit paid (converted into shares). In the case of WIG20, this negatively affects the index quotation on that day, while for WIG it does not matter (so de facto this index takes into account dividends accumulated over the years, which increases the rate of return).

It is worth mentioning the “profitable twin” of the WIG20 index. We are talking about WIG20 Total Return, i.e. a portfolio consisting of the same companies as WIG20, but including payments to shareholders. WIG20TR performs much better than the regular index of Polish blue chips, its quotations are much more similar to the broad WIG index. WIG20TR has grown by 82% since the end of October 2007. (i.e. the rate of return is 88 percentage points higher than the “ordinary” WIG20 and 28 percentage points lower than WIG).

The difference is not only in dividends

However, it cannot be said that only the issue of dividends is the reason for the difference in the rates of return of individual indices. The composition is also key, i.e. which companies are included in a given portfolio. This can be seen, for example, in the weaker behavior of WIG20TR than in WIG, where smaller companies are also important and the share of blue chips is more limited than in WIG20. For example, mWIG40 and sWIG80, grouping medium- and small-sized companies, respectively, which are also price indices, performed very well and regularly set new historical highs after 2021 (unlike WIG20).

This was the composition and weighting of individual companies in the WIG20 index at the end of 2007.

|

GPW.pl

Why did the Polish stock exchange in general – and WIG20 in particular – take so long to recover from the global financial crisis? It happens that the economy and the stock exchange are (contrary to appearances) two different organisms. We recently wrote that the German DAX was breaking new records as the German economy has been stagnant for several years. In our case it was the opposite: the economy was booming and the stock market was stagnant. While the growth of Polish GDP was largely driven by small and medium-sized enterprises, including exporters, WIG20 did not benefit from these positive trends and struggled with completely different problems.

For years, the composition of WIG20 was a problem. The structure of the most important Polish index was (and largely still is) its greatest burden. Companies controlled by the State Treasury dominate and have not always been managed to take care of the interests of their shareholders, which is why investors value them at a discount. The industry structure was also a problem. The American stock exchange (S&P500) has been growing in the past decade thanks to technology companies, while WIG20 is the kingdom of the “old economy”. Energy, mining and fuel companies played a major role in this index (their importance has decreased slightly over the years). The energy sector was forced by politicians to save bankrupt coal mines and at the same time faces challenges regarding large investments, which depresses results, limits dividends and valuations. The financial sector is still of great importance in WIG20, but now – unlike the problems in previous years (e.g. Swiss franc loans, bank tax) – banks are the driving force behind the boom.

WIG20, the price index, has performed much worse over the years, which is not surprising considering that this type of portfolio does not take into account dividend payments (its Total Return version does).

|

Stooq, own study

It must also be said directly: the valuations from the fall of 2007 on the WSE were not rational. It was the height of the boom, money was poured into the stock exchange in a large stream, and it was the last time Poles were so willing to buy shares (which later resulted in their burn, considering how the valuations of investment fund management companies fell). The market was pricing in a perfect future that never came. Later – in addition to remembering the painful losses – the inflow of capital from small investors to the WSE was hampered by regulations such as MIFiD. Some of the more courageous and conscious investors switched to foreign markets.

There is one more factor – technical, but very important. Open Pension Funds have been a powerful driving engine of the WSE for years. Every month they pumped a steady stream of cash from our contributions into Polish shares, creating natural demand in a sense “regardless of the economic situation.” As a result, Polish shares were on average valued at a premium to their regional counterparts. The government reform of 2014 (taking over the bond part and changing the rules for funding OFE) drastically cut off this capital inflow. This also resulted in a deterioration of liquidity, which could have resulted in foreign investors being less willing to make purchases.

See also: Surprisingly large profits on the Warsaw Stock Exchange. But experts are divided

However, what happened on emerging markets, to which we are still classified, may be crucial. After the crisis in 2008, foreign investors turned to American stock exchanges. For about a decade, entire emerging markets, including Poland, performed very poorly compared to the US. Therefore, even if we did not have internal problems with the structure of WIG20 and the OFE reform, the weak global environment could have prevented the WIG20 index from equaling the records from 2007 (on the way there was also a debt crisis in Europe, which also depressed stock indices).

A bittersweet celebration

— This is a completely different index than 19 years ago, few of the current investors were active on the market in 2007, and if they were, they remember when the records ended. Paradoxically, headlines like “It took the index 15 years to break the record from 2007.” In my opinion, they do not help the stock market and may discourage some people from investingespecially when warnings about the end of the current long-term bull market are becoming more frequent. In fact, the bittersweet celebration of the new record on WIG20 may suggest how bad it is to buy shares in the last phase of the boom and how long you have to wait for even a nominal recovery of capital. Because in order to say that WIG20 was actually profitable, it would have to increase by almost 100%. from today's level – says Marcin Materna, director of the analysis department of the Bank Millennium Brokerage Office.

In his opinion, there is a chance that WIG20 will break the record this year, although he reminds that the dividends of large companies that will generously share their profits this year (including banks) will be eliminated. However, he emphasizes that there is not that much to celebrate.

— Someone may ask the question – why did it take so long to equalize the index level from 19 years ago? It should be remembered that it is better to judge the stock exchange by the WIG index, where some time ago we beat the level from 2007. Against this background, the WIG20 record will only be a minor curiosity – points out Marcin Materna.

See also: The Warsaw Stock Exchange turns 35. Here are the key events

— Historically, there were many reasons for the weakness of the WIG20 and it seems that the current boom is due to a reversal of the situation in the case of many of them.. For example, in the face of subsequent geopolitical events in the world, the perception of geopolitical risk due to the war in Ukraine is decreasing (this has already been discounted in 2022). Inflows to PPK and high dividends balance outflows from equity funds and OFE. The share of companies controlled by the State Treasury is gradually decreasing, and cyclical sectors that are strongly represented in WIG20 – such as banks and raw materials – have had a favorable environment to improve their results in recent years – comments Michał Krajczewski, manager of the investment advisory team at the BNP Paribas Brokerage House.

He adds that foreign investors notice these changes. — As well as the low valuation of domestic companies and the good results of the Polish economy, which translates into increased inflows from abroad to our market in the last two years. Thanks to this, WIG20 is approaching the historical records of 2007. Their exceeding will be a certain symbol, but taking into account the structure of the index, because WIG20 is a price index, and WIG20TR and WIG have long been at the peak of the bull market, it should not be an event affecting the assessment/image of the market – emphasizes Michał Krajczewski.

Important: the calculations and information contained in the text are for information purposes only and do not constitute a recommendation or any other form of suggestion for the purchase or sale of financial products. Investment decisions should be preceded by your own analysis of risk and financial situation.

Author: Maciej Rudke, journalist of Business Insider Polska