2026-04-13 15:50

publication

2026-04-13 15:50

The conflict in the Middle East changed the rules of the game on the oil market. Investors and companies now look less at oil prices in futures contracts and instead focus on physical barrels immediately available. The difference between the “paper” promise of raw material delivery and the cost of real oil to buy “for now“ has reached unprecedented proportions.

Although diplomatic maneuvers, including news of a temporary ceasefire between Washington and Tehran, have somewhat calmed down the mood among stock market speculators – as evidenced by the decline in oil futures – there is enormous tension in the world of physical commodity trading. Due to the paralysis of the key route through the Strait of Hormuz, refineries must fight hard to secure immediate supplies.

The situation is worse than after the outbreak of the war in the East

This led to a rare anomaly: stock exchange valuations (based on futures contracts) took on a life of their own, and prices on the spot market, where you pay for physical goods delivered immediately, skyrocketed. The situation is exacerbated by the fact that the weekend peace talks ended in failure, and the United States is threatening to strengthen the blockade of Iranian exports, which may include military actions in the strait area.

Advertisement

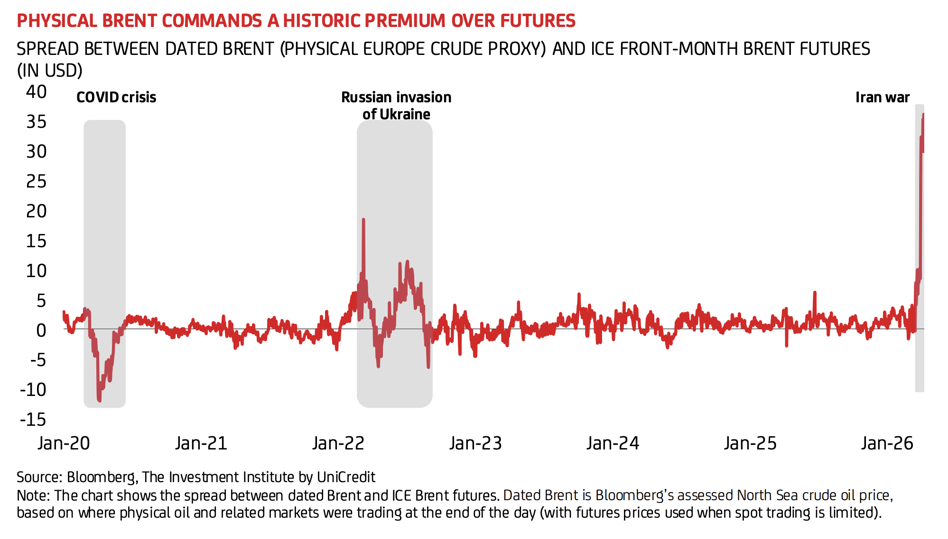

Analysts from the Investment Institute at the UniCredit bank illustrated this problem by comparing the prices of the nearest futures contracts (ICE Brent) with the prices for physical oil supplies in Northwest Europe (the so-called Dated Brent index). The difference in these prices has become unusually high in recent days.

Analysts remind us that during the COVID-19 pandemic, when the global economy froze and warehouses were bursting at the seams, physical raw materials were drastically cheaper than in futures contracts. The situation reversed after Russia's invasion of Ukraine – the fear of a collapse in supply from the east drove up the prices of raw materials with current supplies.

However, what is happening now with the war in Iran overshadows the events of recent years. Buyers on the physical market today are forced to pay a huge premium for the opportunity to receive tangible goods from the North Sea in the near future.

This situation is called backwardation in the jargon of financial markets. In stable economic conditions, the reverse phenomenon (contango) is standard, where raw material with a deferred delivery date is more expensive to compensate for the costs of its storage over time. Now, however, the extreme fear of shortages has reversed that curve. Such high premiums on the spot market limit the room for price declines on stock exchanges and make the market extremely susceptible to a return to strong backwardation should military tensions escalate again.

A hindrance to the disinflation processes

Despite Donald Trump's declaration of the imminent unblocking of the Strait of Hormuz (through which one fifth of the world's oil flowed before the escalation), the physical market does not price in this optimistic scenario at all. Possible political truces will not solve the problem overnight. Damaged infrastructure, inflated ship insurance rates and chronic logistical bottlenecks mean that physical access to oil will improve very slowly and unevenly.

The continued high tension in the instant delivery market is bad news for the fight against inflation. As UniCredit economists note, an extremely expensive raw material on the physical market increases energy costs and puts obstacles to disinflation processes in Europe

They conclude that until there is lasting and credible peace in the Middle East, the “floor” for oil prices will remain high, and the terms of the game will be dictated by the physical raw material market, not stock market speculation.

The publication contains affiliate links.