Billions of zlotys invested with falling inflation and increasingly lower interest rates in mind are a thing of the past. Market turmoil turned the previous assumptions upside down. What percentage on a bank deposit should be considered good, which bonds are better and how to divide savings? We ask a professional.

Inflation was falling and with it interest rates. This translated to increasingly lower interest rates on bank deposits and deterioration of the offer of treasury bondsamong which three-year fixed-rate bonds were the most popular. This was the situation before the attack on Iran from the perspective of savers who avoid risky investments. The war in the Middle East completely changed the situation.

How to invest the free funds that remain after paying bills and other monthly expenses? If you don't like risk, don't accept losses, and at the same time want to take care of your savings in the best possible way, we have some advice and tips from an expert.

Important: the forecasts and valuations included in the text are for information purposes only and do not constitute a recommendation or any other form of suggestion for the purchase or sale of financial products. Investment decisions should be preceded by your own analysis of risk and financial situation.

Read also in BUSINESS INSIDER

Bank deposits and treasury bonds. What do they offer now?

Poles most often keep their savings in the bank. This is a simple and safe method, but this way the money does not work optimally. The latest data from the National Bank of Poland (NBP) show that the average interest rate on current deposits dropped below 0.6 percent. on an annual basis. In total, interest, e.g. on deposits, is approximately 3.3%. (lower interest rates can hardly be considered beneficial), and in 2023 they reached almost 6%.

interest rates on savings in banks have been systematically falling for several years

| NBP, own calculations

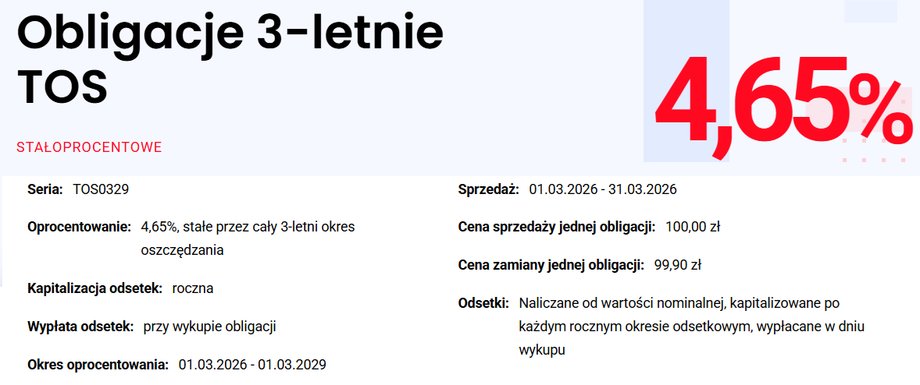

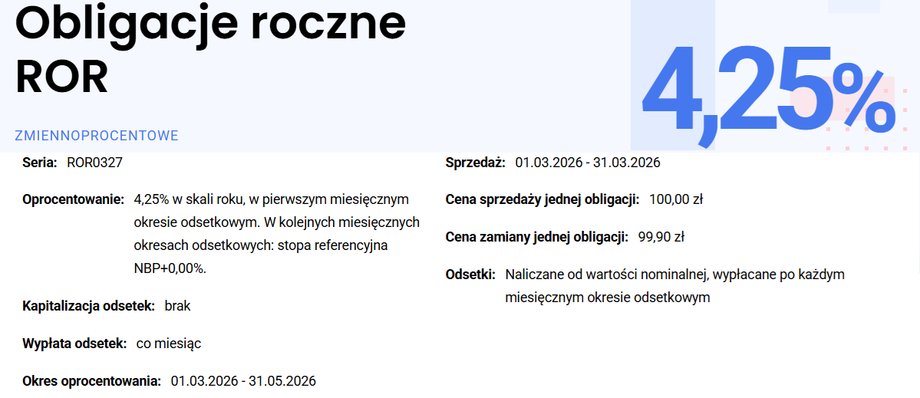

A direct alternative to bank deposits are treasury bonds, guaranteed by the state. Their design and method of purchase are very simple (we wrote more about this in the article: The state gives money to those who save money. We check how much you can gain), and the interest rates are mostly higher than those offered on standard deposits. The difference, however, is this Typically, deposits are made for several months, and savings in bonds last for more than a year (the exception are three-month bonds, but for a short period of saving their interest rates are not attractive).

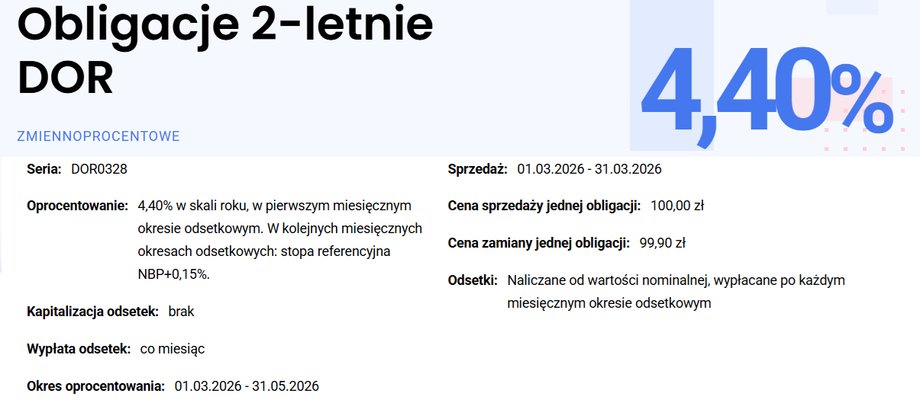

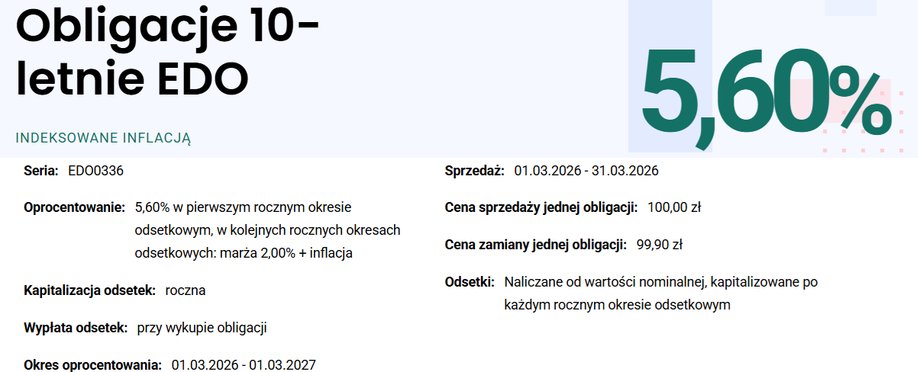

Basic types of treasury (savings) bonds. March 2026 offer

| obligacjeskarbowe.pl

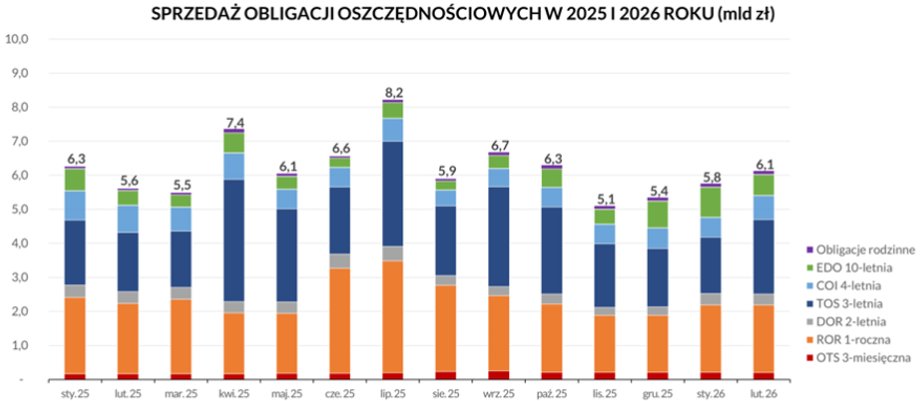

Saving the new way. The most popular bonds have lost their luster

For at least the last dozen or so months, four-year inflation bonds have not been very popular. Definitely three-year bonds with a fixed interest rate or one-year bonds dependent on NBP rates were more willingly chosen.

This way every month ordinary Poles (we ignore the massive purchases of bonds by financial institutions) invested billions of zlotys in savings.

For a long time, inflation bonds were not very popular

| Ministry of Finance, own study

Poles' preferences were justified. Since inflation was falling, inflation bonds did not offer as much potential as, for example, fixed-rate bonds, which could be frozen at a relatively high level for three years with the prospect of falling interest rates. The war in the Middle East turned these macroeconomic assumptions about inflation and interest rates upside down.

What's the best way to invest your savings in bonds now?

— The market narrative has changed. A lot depends on the situation in the Middle East and its impact on inflation in Poland. The key question is how much prices will increase and for how long – Dr. Tomasz Bursa, vice-president of Opti TFI and fund manager, comments on the situation.

In an interview with Business Insider, he admits that previous assumptions about interest rate cuts seem rather unrealistic. At the same time, the risk of a possible increase must be taken into account.

See also: Business Insider Barometer. How have the forecasts for Poland changed after the US and Israel attacked Iran?

Tomasz Bursa, taking into account current market conditions and possible scenarios of changes in interest rates and inflation, estimates that the offer of fixed-rate treasury bonds looks quite weak.

| obligacjeskarbowe.pl

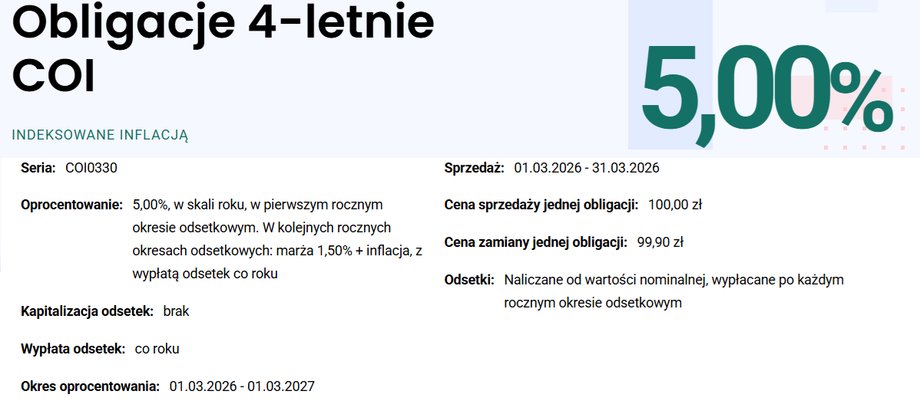

The vice-president of Opti TFI points out that the expected inflation in the following years is crucial to assess the profitability of three-year fixed-rate bonds and four-year inflation bonds. Based on the parameters of the March bond offer, he calculates that the reference point is the inflation rate of 3%.

— If we assume that in a year or two inflation will be above 3%, four-year bonds should be more profitable. This is a plausible assumption – assesses.

| obligacjeskarbowe.pl

Tomasz Bursa estimates that based on recent changes in crude oil prices on global stock exchanges and fuel prices in Poland inflation can be forecasted next year at around 3.5%. However, he stipulates that the final data will depend on how long the conflict in the Middle East lasts and how much the prices of raw materials change.

How do four-year inflation bonds compare with one-year or two-year securities, the interest of which depends on NBP interest rates? — The key question here is about the speed of the Monetary Policy Council's response to inflation. If the interest rate at the National Bank of Poland suddenly increased to 5-6 percent, bonds of this type would yield high interest. At this point, however, this seems an unlikely scenario – assesses.

| obligacjeskarbowe.pl

| obligacjeskarbowe.pl

The expert points out that the Monetary Policy Council lowered interest rates relatively slowly relative to inflation, which is now comfortable for it and constitutes a buffer. As long as inflation does not permanently exceed 3-3.2%, the Council does not have to change its stance in monetary policy.

Conclusions? — The best option at this point seems to be four-year inflation bonds, which will respond faster to the market situation – says our interlocutor.

What about 10-year inflation bonds? The interest rate in the first year is higher than in the four-year period, and there is also a higher margin. — In the case of ten-year bonds, including inflation bonds, it is more difficult to forecast due to the long period and many variables along the way – emphasizes Tomasz Bursa. For this reason, I suggest treating these types of products slightly differently.

10-year bonds may be an interesting option, e.g. in the context of additional savings for retirement.

| obligacjeskarbowe.pl

What to do with savings? It's worth sharing the risk

In investing, but also in investing savings more conservatively diversification is important. This is a rule that can be figuratively reduced to saying that you don't put all your eggs in one basket. Instead of investing all your savings in one thing, e.g. only in shares of one company, it is safer to divide them among various products: bank deposits, bonds, shares, certificates, raw materials, real estate, etc.

See also: How to make money on the stock market? Check out these five companies. There's a lot going on around them

Thanks to this, when one of the investments declines or simply brings lower profits, the others can earn better, which protects the total capital. It is also worth sticking to this rule when investing savings in treasury bonds.

— A reasonable strategy seems to be to divide the money, e.g. by investing 2/3 of the funds in four-year bonds and the rest (1/3) in one- or two-year securities. – says Tomasz Bursa.

Dr. Tomasz Bursa is a leading banking sector analyst and an expert in macroeconomic analyses.Since 2005, he has worked at Ernst & Young Polska, DMBH, Espirito Santo Investment and Ipopema Securities. Currently, he is the vice-president of Opti TFI. He is a doctor of economic sciences at the University of Łódź. He is a licensed investment advisor and broker.

Note: The information contained in the text is for informational purposes only and does not constitute an investment recommendation, information recommending or suggesting an investment strategy within the meaning of applicable regulations, or any other form of advice regarding the purchase or sale of financial products.

Author: Damian Słomski, journalist of Business Insider Polska

I’m Ashley Davis as an editor, I’m committed to upholding the highest standards of integrity and accuracy in every piece we publish. My work is driven by curiosity, a passion for truth, and a belief that journalism plays a crucial role in shaping public discourse. I strive to tell stories that not only inform but also inspire action and conversation.