The fiesta on the Polish debt market is underway. Is it worth participating in the bond boom?

The Polish debt market is breaking new records and setting new milestones. However, observing the unwavering desire of Polish investors for securities generating fixed income, it is difficult to ignore a few at least orange warning lights.

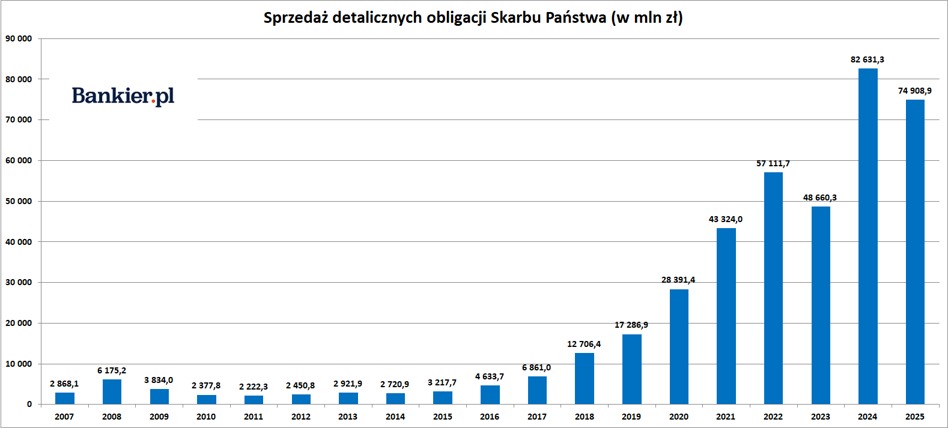

Poles love bonds. And in practically every form. In 2025, they spent almost PLN 75 billion on retail Treasury bonds. Although this is slightly less than in the record-breaking year of 2024 (PLN 82.6 billion), it is still a very strong result compared to the historical background. Let us recall that it was only 7 years ago that this previously niche product began to gain popularity, exceeding PLN 10 billion in annual sales.

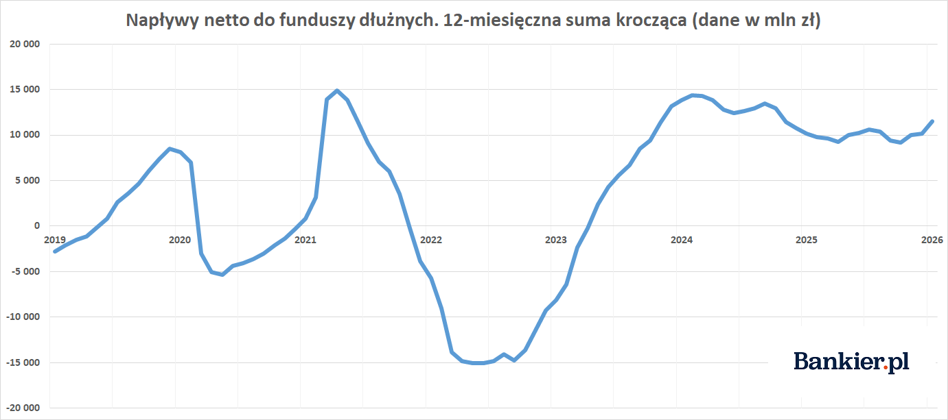

To this must be added the over PLN 51 billion that Poles paid (net) to domestic investment fund companies over the previous 12 months. According to IZFiA data, in 2025, in the segment of Polish debt securities funds, the predominance of purchases over redemptions exceeded PLN 10.1 billion. Let's add PLN 37.5 billion to short-term debt funds.

This trend was intensified in January 2026. According to data from the nazwa.pl website, a historical record was broken and PLN 8 billion was paid to national investment funds. Of this amount, as much as PLN 5.7 billion flowed to debt funds. For comparison, just under PLN 1 billion went to pure equity funds, which was a long-term record anyway. This disproportion clearly shows how much, as a nation, our portfolio is overweighted by bonds over equity instruments.

We must also add PLN 2.5 billion that Polish individual investors spent in 2025 on issues of new corporate bonds. For this amount, DM Michael/Strom analysts summarized last year's 19 issues of public bonds of enterprises – mainly developers and debt collection companies. 20.3 thousand people took part in them. investors. In some cases, demand was so strong that issuers decided to increase their issuance, sometimes even doubling the size of the offering.

Let's also not forget about the first issue of covered bonds (to put it very simply, a form of mortgage-secured bonds), which was carried out by the PKO BP bank in October. Poles signed up for securities with a nominal value of PLN 1.155 billion. This meant an increase of 15% to the original offer. However, we do not know how much was spent on bonds listed on the Catalyst market, where both treasury and corporate securities are available.

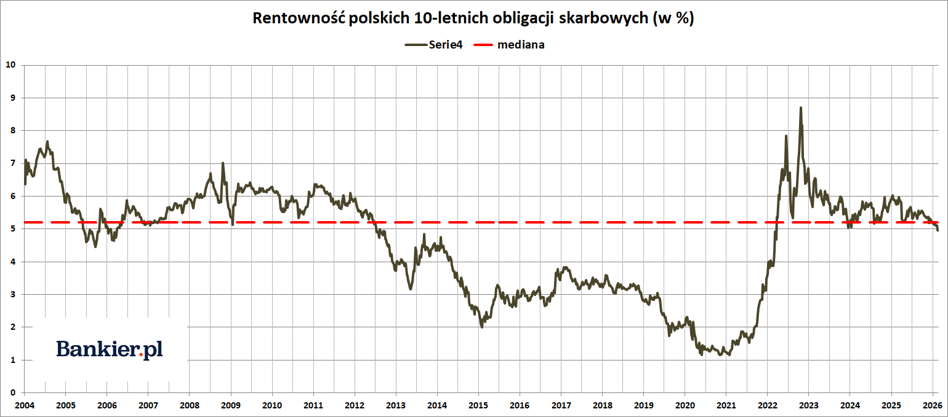

It is also worth noting that the love for Polish bonds (especially treasury bonds) also extended to professionals. The demand for Polish debt is sensationally strong, despite huge problems with excessive debt (the constitutional barrier of 60% of GDP of public debt has just been lowered) and permanently too high fiscal deficits (without any plans for their immediate and significant reduction). The result of the January auction, during which the Ministry of Finance sold bonds for PLN 12 billion with purchase offers totaling PLN 21.37 billion, is a symbol of the desirability of securities issued by the Ministry of Finance. And in February, a new record was broken in the form of PLN 25.8 billion of bonds sold during one auction.

What's driving bond sales?

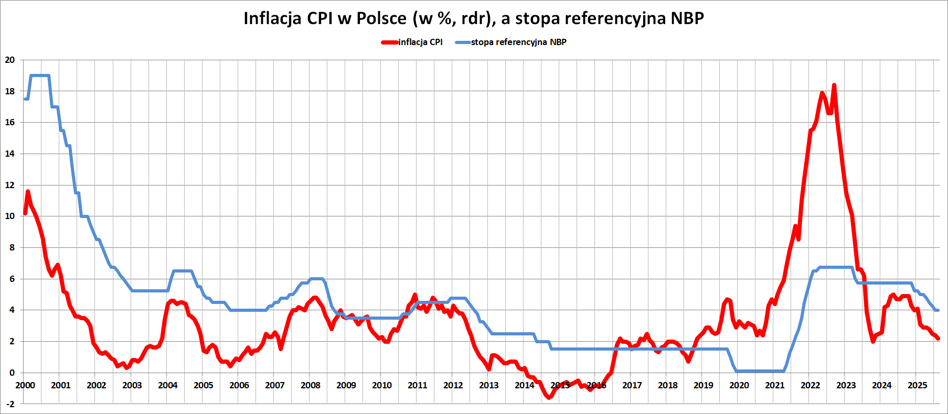

The boom in Polish bonds, which has been ongoing since spring 2023, is driven by a combination of two factors: decreasing price inflation and – at least until recently – relatively high nominal interest rates. In IZFiA data, we see that the sale of bond funds started approximately in the spring of 2023, i.e. almost three years ago. This was the time when CPI inflation in Poland set a 26-year high of 18.4% per annum. It was in February 2023.

Half a year earlier (i.e. in September 2022), the Monetary Policy Council ended the cycle of interest rate increases, raising the NBP reference rate from virtually zero to 6.75% in less than a year. At that time, we had nominally the highest interest rates in the central bank in 20 years. Later, inflation began to fall very quickly, and the NBP rates were lowered for the first time only a year later (and as it turned out later – definitely too early and too much). Then the Monetary Policy Council cut rates in October, and then refrained from further reductions until May 2025.

As a result, we had clearly positive real interest rates in Poland for the previous two years. I.e. Throughout this time, the NBP reference rate was higher than the official CPI inflation for the previous 12 months. This state of affairs favors instruments that generate fixed income, and what is more, clearly exceeding both historical and – and perhaps above all – expected inflation. It is hardly surprising that Poles blindly took 6-7% of a relatively “secure” income with CPI inflation heading towards the 2.5% target of the National Bank of Poland.

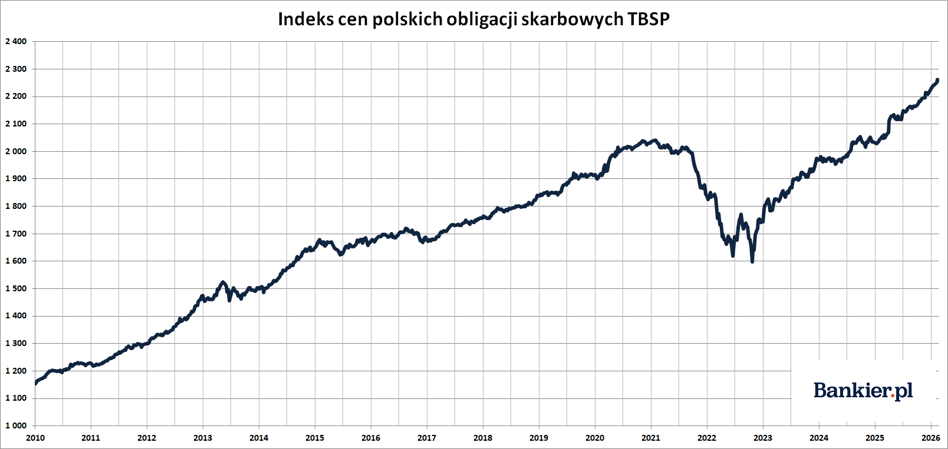

However, in my opinion, the historical rates of return played the main role. The boom in the Polish debt market started exactly at the same time as the increases on the WSE – in the fall of 2022. The TBSP index, measuring the prices of fixed-coupon Polish treasury securities, skyrocketed after the epic bear market of 2021-22 and increased by 12.8% in 2023 alone. It added another 3.3% in 2024 and a high 9.5% last year. Owners of domestic debt funds perceived as safe could count on these profits. And from the experience of the last quarter of a century, we know that nothing attracts Poles to investing like historical rates of return.

Are Polish bonds a good option now?

In less than four years, Polish fixed-coupon bonds have returned an average of over 40%, climbing almost continuously and more than making up for the unprecedented losses (-22%) of 2021-22. Let's add to this the inflation Eldorado that has happened to holders of retail “treasury bonds” with interest rates indexed to CPI inflation, which allow them to “extract” up to 20% annually on some EDO series.

It's just that every boom comes to an end and what was a great idea in times of peak inflation and relatively high interest rates no longer has to be so good. Firstly, inflation is already relatively low (2.2% in January 2026) and will probably not be much lower. However, it may increase in the next few quarters, when the current disinflationary factors fade away (cheaper fuels, industrial deflation, etc.). The cycle of reductions in short-term interest rates at the National Bank of Poland is also slowly coming to an end. The debt market has already discounted all this a long time ago and there is no longer enough fuel for a further decline in the yield (i.e. price increase) of bonds.

The business cycle was no longer favorable to bonds. The disinflationary phase of economic recovery is probably coming to an end, which is usually followed by higher inflation and then a cooling of the economic situation. Such a mix in the environment of very high state debt (the debt of the public finance sector has probably just exceeded the constitutional limit of 60%) and a record supply of securities from the Ministry of Finance is potentially dangerous for holders of Polish debt.

In such a situation, in my humble opinion, going “all-in” into bonds does not seem to be the best idea. Of course, this is not a reason to eliminate bonds from your portfolio! This is not 2019 or 2020, when holding “income-free securities” was a recipe for financial disaster. Now interest rates are still positive in real terms and nominally significantly above zero. Therefore, bonds, as an asset class, will still find their place in many long-term and diversified investment portfolios. The only question is whether predominating the portfolio with Polish bonds in the current phase of the business cycle and with clearly reduced yields is an optimal solution from the point of view of a long-term individual investor.

Yes, the fixed income and relative security offered by this asset class have always been valuable. But it doesn't have to be this way in the future. Especially if the signals of the upcoming “global reset” were confirmed, in which the monstrous debts accumulating over the previous two decades would be effectively eliminated, primarily at the expense of holders of government promises in the form of bonds, pensions and all kinds of other “benefits”.