The Reserve Bank of Australia was the first Western central bank to decide to increase interest rates after the monetary easing cycle. This raises the question of whether this is a matter of Australian exceptionalism or the beginning of a reversal of a global trend.

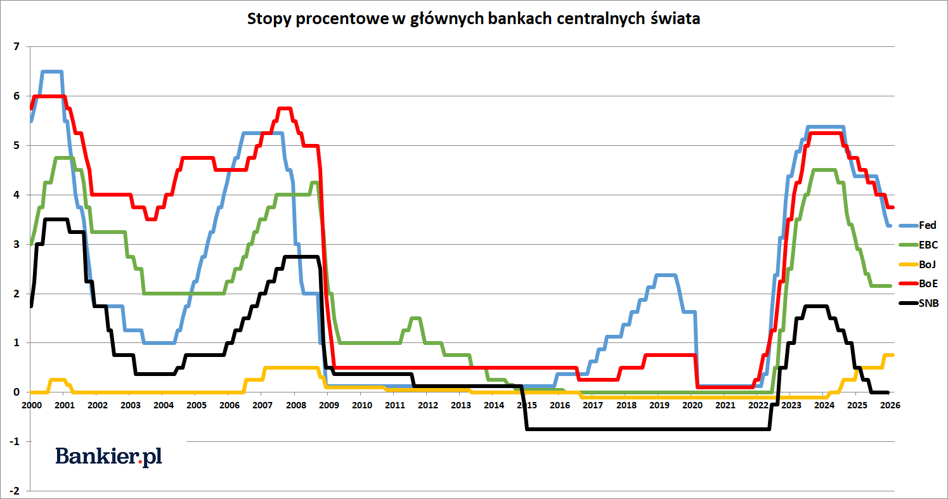

Since spring 2024, the largest developed economies (except Japan – this is a special case) have been easing monetary policy. The first to break ranks in this cycle was the Swiss National Bank, which carried out its first interest rate cut in March '24. In June it was joined by the European Central Bank, in August by the Bank of England, and in September '24 by the Federal Reserve.

At that time, these were the first reductions in borrowing costs in Western economies after the inflation wave of 2021-23 forced the world's largest central banks to abruptly move from extremely expansionary to moderately restrictive policies. As part of this reversal, interest rates in advanced economies rose from virtually zero to 4-6%, reaching the highest levels since the Great Financial Crisis of 2007-09.

Financial market participants continue to expect interest rate cuts in the world's key central banks. Primarily in the Federal Reserve, after which cuts of 50-75 bp are expected. until the end of 2026. The Bank of England is also expected to cut rates (which narrowly lost such a decision during the February meeting), although the European Central Bank and the SNB have probably ended their cycles of easing monetary policy.

Australian experiment in monetary policy

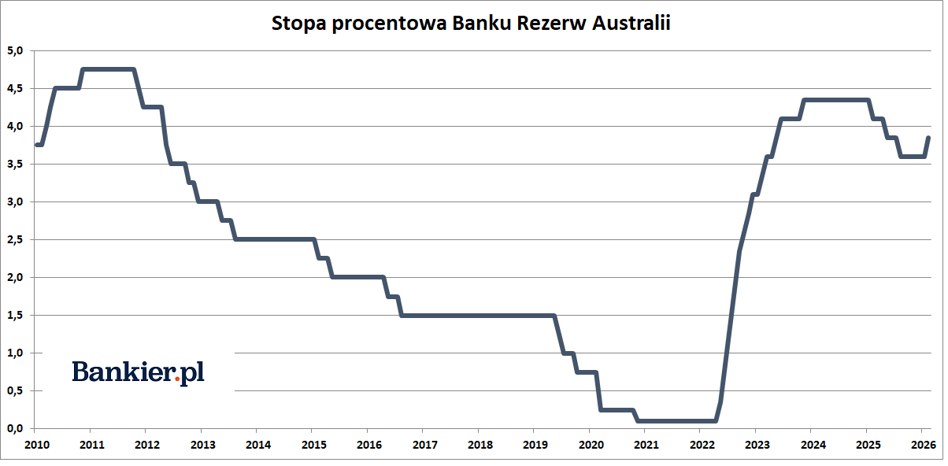

And then, on February 3, the Reserve Bank of Australia decided to… increase interest rates for the first time since 2023. The increase amounted to 25 basis points. and raised the monetary policy rate from 3.60% to 3.85%. Apart from the Bank of Japan (which “slept through” the previous cycle of increases and is only now catching up by raising interest rates, raising another 25 basis points in December)

it was the first interest rate increase in a major advanced economy since the monetary easing cycle began almost two years ago.

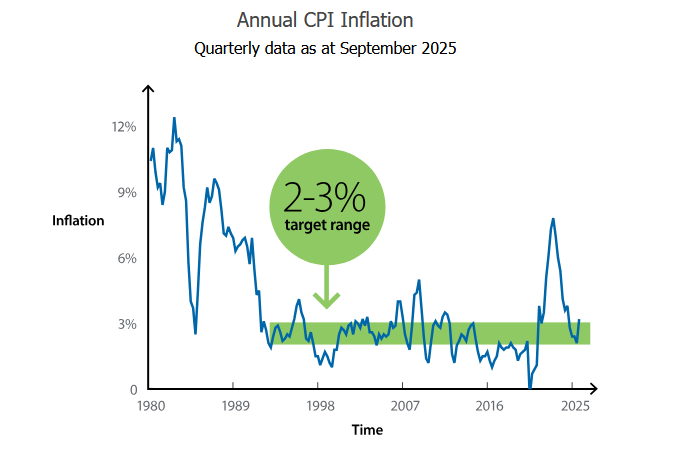

Truth be told, the RBA authorities had little choice and, as is typical for central bankers, they reacted with considerable delay. With an official inflation target of 2-3% in December 2025, Australian CPI inflation accelerated to 3.8% compared to 3.4% in November. And 1.9% recorded in June '25. The RBA therefore had to admit to the obvious mistake of last year's decisive interest rate cuts. In February 2025, the RBA made the first cut (by 25 bp) in the cycle, and then also cut it by 25 bp. in May and August. In total, it reduced the retention rate by 75 basis points.

– Private demand is growing faster than expected, the pressure on production capacity is greater than previously estimated, and conditions on the labor market are too tight – this is how the authorities of the Reserve Bank of Australia explained their February decision to increase interest rates.

“Inflation will remain well above the upper end of the inflation target until next year, after which it will begin to decline gradually,” said Sunny Nguyen of Moody's Analytics. This means that further increases in interest rates in Australia are possible. Nguyen added that Australia's economy is currently “overheated” due to rising exports to East Asia and the artificial intelligence boom.

– The idea was that they didn't have to raise interest rates as much as they had in the past. And they certainly did not raise rates as high as in other developed economies, e.g. the US, UK. Great Britain, Canada and New Zealand. They hoped this would be enough to bring inflation back to target without a recession or a large increase in unemployment. So this policy was essentially an experiment. And it was a failure, because inflation is not under control and has remained higher than the target for 5 years – said Warren Hogan, executive director at EQ Economics, quoted by news.com.au.

Was it looser already? Are we facing a monetary revolution?

– If inflation remains persistent and does not move in the direction of the inflation target, the Council may consider whether it would be appropriate to maintain interest rates at current levels or raise them at some point – said Michele Bullock, Governor of the Reserve Bank of Australia.

The prevailing opinions in the comments are that Australia is an isolated case and that the RBA's February rate increase was a consequence of last year's mistakes (i.e. an unnecessary reduction in the already excessively high interest rates) rather than the beginning of a new trend. First of all, the market still expects further interest rate cuts in the US. Especially under the new head of the Federal Reserve, as Kevin Warsh favors lower interest rates.

A distinguishing feature of Australia is the very high debt of the private sector. According to World Bank data, credit to the private sector at the end of 2024 accounted for almost 130% of GDP. Yes, in some developed economies these statistics are even higher (e.g. in the USA and Japan it is approximately 200%, and in China 194%), but Australia is not such a large country and does not have such large capital. What's more, the majority of this debt consists of household liabilities under mortgage loans (113.7% of GDP at the end of Q2 2025). In this context, the RBA became a slave to the policy of not irritating Australians who purchased absurdly expensive houses and apartments on credit.

Therefore, theoretically, the Australian interest rate increase is an isolated issue and a special case on the map of global finance. It's just that all the world's leading central banks made a fundamentally similar mistake to the RBA (although perhaps in a less drastic form). Both the Fed, the ECB, the Bank of England and the Bank of Japan raised interest rates too low (and definitely too late) in relation to the inflation wave of 2020-23. For now, everyone is happy with the disinflation that has been going on for three years, but it is based on clay foundations.

All it takes is some (even small) oil shock, a return of the boom in agricultural produce markets or another geopolitical turmoil to quickly raise inflation rates of 2-3% today to the range of 4-6% or higher. And then central bankers will have a choice of either allowing a faster loss of the purchasing power of money (i.e. higher inflation) or following in the footsteps of Australians. And this would be a disaster for the very “generous” valuations of many financial assets: from treasury bonds, through the private debt sector and ending with sky-high valuations of companies from the AI sector.