A meeting was held on Wednesday joint parliamentary committees: economy and development and justice and human rights regarding the so-called franc act. This is the first substantive meeting after the first reading, which took place two months ago, on October 16. The meeting lasted nearly three hours and showed that there was a heated dispute over the bill. This was admitted by Deputy Minister of Justice Arkadiusz Myrcha, who, however, hopes that the legislative process will be completed in spring and the act will take its optimal shape.

See also: There is a position of the Polish Financial Supervision Authority regarding billions of bank profits

Stormy session of the Sejm committee on the Swiss franc law

Rafał Komarewicz, MP from Poland 2050, chairman of the Parliamentary Committee on Economy and Development, began the meeting by emphasizing that this matter is very important because it concerns several hundred thousand borrowers. He noted that you have to balance everything wellwhen it comes to the speed of court proceedings, but remembering that borrowers who took out a loan in Swiss francs and were not treated fairly by banks must have full rights to pursue their claims.

Arkadiusz Myrcha, Deputy Minister of Justice, who presented the project, emphasized that its aim is to relieve congestion in courts, especially appellate courts, but without influencing the shape of the verdict.

— We are talking about a caseload that is about five or seven times greater than the number of divorce cases. In appellate courts, Swiss franc cases very often constitute more than half of the entire volume of proceedings in civil departments. That is why the overwhelming majority of the regulations we are talking about today concern only procedural and procedural solutions. It is not our task to act as a judge or to take sides in the dispute. Our goal is to improve those elements of the process that constitute the greatest barrier today, emphasized Myrcha.

However, the amendments submitted and the heated discussion during the meeting indicate something else. The first four amendments were submitted by Dominik Jaśkowiec, MP from the Civic Coalition. We explain what the government proposes, what the MPs propose, and what the parties' expectations are.

Read also: This CJEU judgment will affect Polish judges. Will it force banks to change their strategy?

Meeting of parliamentary committees on the draft Swiss franc law

|

Sejm

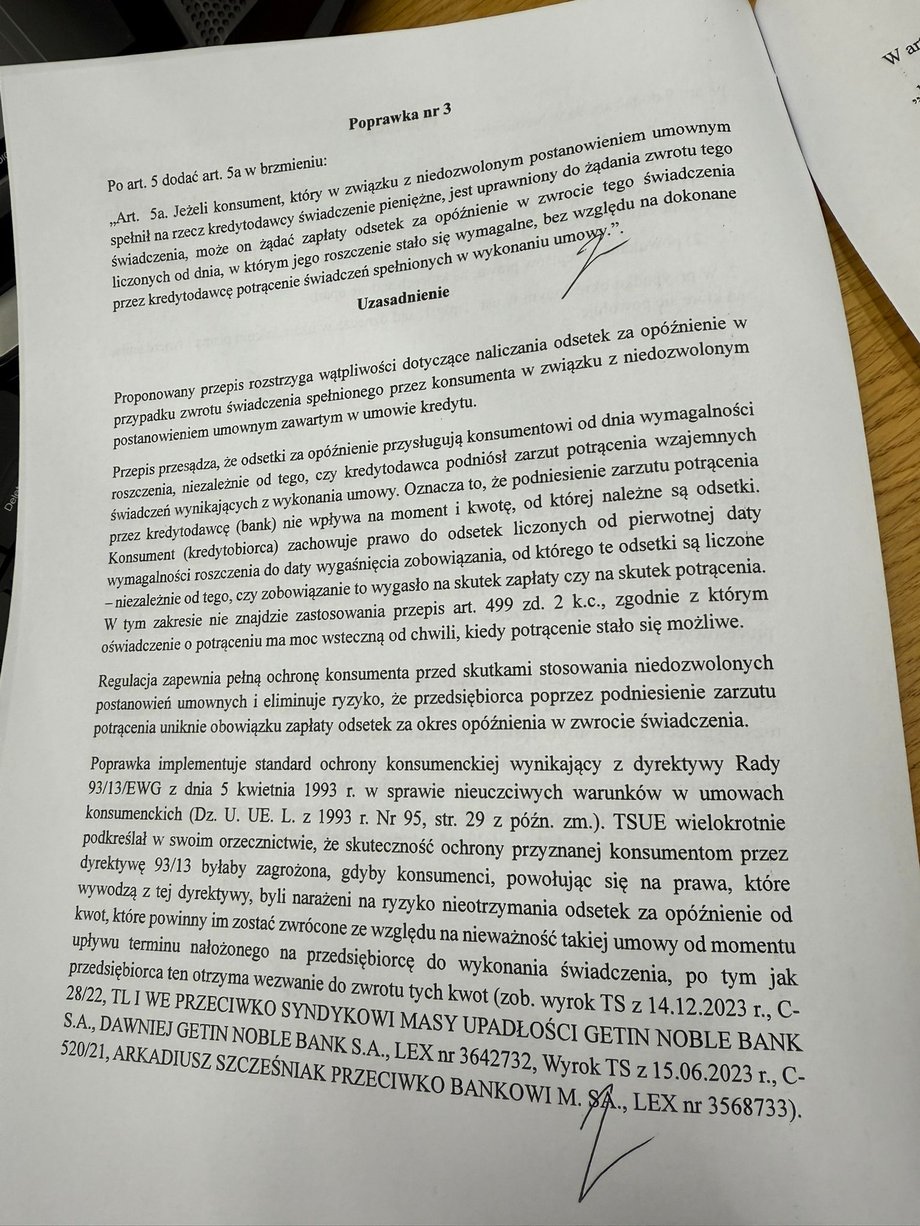

Key fix number three

The first amendment is purely editorial. The idea is to clarify the provisions on the automatic suspension of installments for the duration of the proceedings.

Second amendment states that if the circumstances of the case do not prevent this, the justification of the judgment of the first instance court may be limited to referring to the lawsuit, response to the lawsuit or further preparatory letters served on the opposing party before the close of the hearing and citing the legal provisions on which the court relied. He's got it allow the courts to prepare the justification faster, which does not raise any doubts.

The Fourth Amendment applies to Supreme Court cases. The idea is that the Supreme Court may, but is not obliged, to refuse to accept a cassation appeal unless it raises a significant legal issue.

However, amendment number 3 is crucialgiving the possibility of pursuing claims despite submitting a special procedure provided for in the draft act.

Look: Banks can no longer intimidate consumers. The CJEU changes the rules

Amendment number three on offsetting

|

Sejm

It is intended to repair art. 5 project. Pursuant to it, the allegation of set-off may be raised until the conclusion of the hearing before the second-instance court. Parties who have not filed objections on time in pending cases will also gain such a right. Currently, as a rule, there are two weeks from the date when the receivable becomes due, i.e. the deadline for its payment has passed. If, thanks to the new regulations, the bank reports the deduction later and the court recognizes it, the franc borrower may be deprived of interest for the time from the lender's request to settle the invalid contract.

The proposed amendment adds Art. 5a is intended to counteract this. In short it says that if the consumer has repaid the loan, he may demand a refund of the amount paid due to the invalidity of the contract, together with interest calculated from the date on which his claim became due.

Rafał Komarewicz believes that the proposed amendments, including one No. 3, which gives the possibility of pursuing one's claims from the beginning despite the set-off, are going in the right direction. – The issue of set-off raises the most doubts and I hope that this amendment will dispel all these doubts – emphasized Rafał Komarewicz.

Arkadiusz Szcześniak, president of the Stop Bank Lawlessness Association, called for a very thorough analysis of article five. – In our opinion, we are going far too far here – he emphasized. Why, the lawyers explained.

Amendment number three only solves one problem

Legal advisor Dominik Gluza, representing consumers, who was the first to obtain a final ruling in the Swiss franc case, said during the committee meeting that amendment number three only solves one problem, the interest problem. — This amendment does not solve the problem of excessive length, because the allegation of set-off will be used to extend the proceedingsif the act comes into force.

— Currently, in appellate courts the waiting time for a trial date ranges from one and a half to even two and a half years. Therefore, if on the day of the hearing the judge is confronted with a new charge, the only possible solution will be to postpone it. This means a further, many-month extension of the proceedings, said attorney Gluza. In his opinion, the banks' representatives will formulate the allegation of set-off ambiguously, which will make it easier to prolong the proceedings.

Representatives of Swiss franc borrowers protest

Attorney Karolina Pilarska, who has been representing Swiss franc borrowers for nine years and has handled nearly 3.5 thousand cases, believes that the Swiss franc law is not needed at all at this point.

— If this is to be an act for Swiss franc borrowers, we must listen to the voice of this community. And this community has huge concerns about this act. What happened in practice after the project saw the light of day? Most banks that have so far refrained from appealing because banks are not entitled to remuneration for the use of capital, nor indexation, or any other benefit apart from the return of pure capital. — she suddenly started filing appeals. The result is that proceedings in cases that previously ended in the first instance took longer because the bank gave up appealing. Currently, banks are waiting for Act I to come into force the possibility of raising an objection to set-off only in the second instance in order to “cancel” the interest. We are talking about people who have been waiting for a sentence for five or six years. These are not trivial amounts – said attorney Pilawska.

And she emphasized that it was not Swiss franc borrowers who clogged the justice system, but the fact that the justice system was not prepared to efficiently hear citizens' cases. – Poles have the right to a fair and reliable trial – she added.

The Polish Bank Association defends the balance theory and criticizes high interest rates

On the proposed art. 5 and the proposed amendment see differently Katarzyna Urbańska, director of the Legal and Legislative Team of the Polish Bank Association.

— JIf we remove the institution of deduction from the project, the project essentially loses its meaning. Without offsetting, the contract cannot be effectively settled in one proceeding. It can be said that the project loses its “heart” and basic function. Instead of accelerating the proceedings, we will get even greater procedural chaos, which will not allow for the streamlining, simplification and conclusion of Swiss franc cases, emphasized Urbańska. And she added that there was interest “customers are simply not entitled to this amount.”

Moreover, Katarzyna Urbańska pointed out that in order to speed up the proceedings, the best solution would be to adopt a clear sanctioning legal basis balance theory.

Rafał Komarewicz, but also his party colleague Paweł Śliz, chairman of the Parliamentary Committee for Justice and Human Rights, wanted to know why the banks did not file charges of deduction on time and why they did not propose settlements instead of arguing in the courts. However, he did not receive an unambiguous and clear answer from the ZBP representatives.

The answer was provided by legal advisor Wojciech Bochenek, who defends Swiss franc borrowers. — By offsetting its claim, the bank would admit that the consumer is right and the contract has legal defects. And only then could he settle his accounts straight. However, banks still adopt the strategy in their pleadings that the contracts are valid, said Wojciech Bochenek.

Ministry of Justice open to changes

At the end of the meeting, Arkadiusz Myrcha, Deputy Minister of Justice, emphasized that the most important thing was for the project to have a shape that would optimally satisfy all parties. — I am happy with all the arguments presented here. The project has already been modified, but I assume that it will be subject to further modifications. Clearing the courts is our priority. We need to deal with the problem as quickly as possible, but without harming the participants. We will work on this project, hopefully in January, so that the entire legislative process can be completed at the turn of winter and spring. THIS would be very advisable – emphasized Deputy Minister Myrcha.