In both personal and property insurance, after three quarters of 2025, PZU retained the largest market share. Insurance companies collected over PLN 18 billion in premiums from life insurance policies, while the write-off from Section II amounted to over PLN 47.6 billion. Year by year, the market boasts higher premiums, but there is a stronger increase in the claims calculated and paid.

Life insurance remains at the forefront

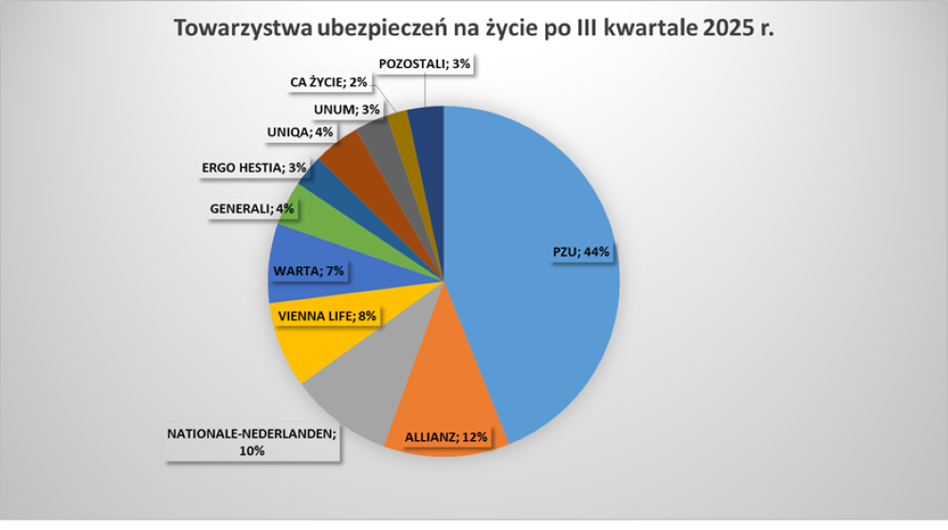

The Polish Financial Supervision Authority data shows that after 3 quarters of 2025, life insurance companies collected PLN 18.3 billion of gross written premiumwhich represented approximately a 3.5% increase year-on-year (better dynamics than in the second quarter of this year). The positive result is largely due to life insurance policies, which were concluded 5.6% more than a year ago, however, both in the scale of the entire section I and life insurance itself, a quite strong increase in awarded compensation is noticeable. Their total dynamics amounted to over 8%, of which only in group I it was approximately 11%.

PZU had the largest share in the life insurance market – 45.4%.which reported over PLN 8 billion in gross written premium. It was followed by Allianz with a share in section I of 11.6% and Nationale-Nederlanden, which is responsible for 9.8% of the entire section. Right behind them were Vienna Life, which promises to fight for the podium (8%), and Warta (7.4%).

More policies and compensation

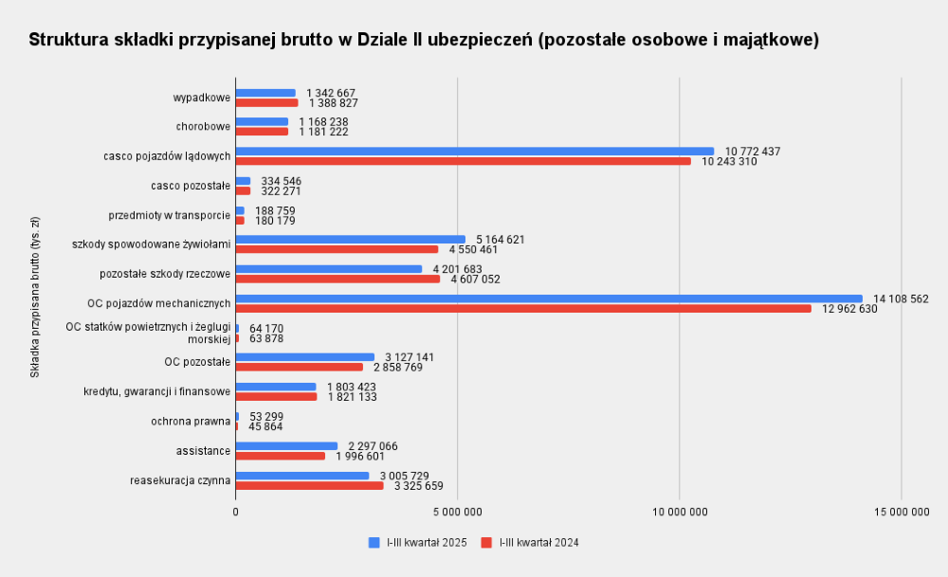

In section II insurance, i.e. other personal insurance and property insurance, insurance companies recorded PLN 47.6 billion in premiums with an increase of 4.6% y/y. The structure is not surprising: for approx. Motor insurance accounts for 52% of the write-off (third party liability insurance and general liability insurance for land vehicles), which increased by 5.2% and 8.8%, respectively, compared to the same period of the previous year. Nearly 20% of premiums were reported in property damage insurance, but year to year only those covering fire and accidental events recorded positive dynamics. It is also worth noting increase in third party liability insurance and liability insurance for aircraft – 18.7% and 22.7%, respectively – as well as a larger write-off in legal expenses and assistance insurance.

In the first three quarters, insurers awarded PLN 24.5 billion in compensation, i.e. 7.8% more than in the same period of 2024, and PLN 26.8 billion in benefits were paid. The largest amounts of payments were traffic and property damage.

The podium in property insurance remains unchanged

A glance at the written premiums of individual Branch II insurance companies allows us to conclude that compared to the period January-September 2024. domestic insurers improved their results in most cases. Warta recorded a dynamics of approximately 22%.second in this respect only to SIGNAL IDUNA Polska, where the collected premiums increased by as much as 39% year on year. PZU and Ergo Hestia reported larger amounts, but with a dynamics of less than a percent, while insurers such as Credit Agricole, Nationale-Nederlanden and UNIQA can boast of an increase of over 10% in premiums y/y. However, the increases in premiums did not change the distribution of power in property insurance: PZU retains the largest overall share in Section II, followed by Warta and Ergo Hestiafollowed by UNIQA, Compensa, Generali, Allianz and Interrisk.

|

Premiums of other personal and property insurance companies |

|||

|---|---|---|---|

|

Specification |

Q1-Q3 2025 |

Q1-Q3 2024 |

Participation |

|

AGRO INSURANCE TUW |

329,087 |

363 493 |

0.69% |

|

TUiR ALLIANZ POLSKA SA |

1,817,067 |

1,856,638 |

3.81% |

|

COMPENSA TU SA Vienna Insurance Group |

3,123,654 |

2,905,541 |

6.56% |

|

CREDIT AGRICOLE TU SA |

79,074 |

68,898 |

0.17% |

|

TUW-CUPRUM |

92,935 |

85,642 |

0.20% |

|

THIS IS EULER HERMES SA |

321 848 |

315 026 |

0.68% |

|

GENERAL TUS |

2,092,610 |

1,976,050 |

4.39% |

|

HERE INTER POLSKA SA |

189,594 |

168,882 |

0.40% |

|

INTERRISK TU SA Vienna Insurance Group |

1,403,031 |

1,301,814 |

2.95% |

|

KUKE SA |

135 081 |

141,920 |

0.28% |

|

LINK4 HERE SA |

775 004 |

915 727 |

1.63% |

|

NATIONALE-NEDERLANDEN TU SA |

159 506 |

141,628 |

0.33% |

|

PARTNER TUiR SA |

6,665 |

5,718 |

0.01% |

|

PKO TU SA |

445 733 |

575 940 |

0.94% |

|

PTR SA |

722 186 |

655 607 |

1.52% |

|

PZU SA |

12,763,699 |

12,745,651 |

26.80% |

|

TUW PZUW |

804 587 |

1,068,620 |

1.69% |

|

SALTUS TUW |

109 405 |

173,595 |

0.23% |

|

SANTANDER ALLIANZ TU SA |

114,848 |

100 806 |

0.24% |

|

SIGNAL IDUNA POLSKA TU SA |

121 405 |

87,229 |

0.25% |

|

STU ERGO HESTIA SA |

7,355,399 |

7,289,890 |

15.44% |

|

HERE EUROPA SA |

174,761 |

283 031 |

0.37% |

|

TUiR WARTA SA |

9,730,121 |

7,979,034 |

20.43% |

|

TUW TUW |

490 488 |

515 963 |

1.03% |

|

TUZ INSURANCE HERE |

339,943 |

340 444 |

0.71% |

|

UNIQA TU SA |

3,785,541 |

3,338,952 |

7.95% |

|

HEALTH IS HERE |

149,067 |

136 815 |

0.31% |

|

Together |

47 632 339 |

45 547 856 |

100% |

|

Source: Bankier.pl based on KNF data |

|||

Fewer contributions after the third quarter of 2025 on a year-to-year basis were recorded, among others, by: Allianz, Link4 and TU Europa. In the case of the latter, the write-off was lower by as much as 38.2%.

Warta is at the forefront in motor third party liability insurance

What could be expected in the scale of the entire property insurance sector looks slightly different if we look at the category of motor third party liability and comprehensive insurance. In the field of compulsory third-party liability insurance for motor vehicles, Warta is in the lead, having once again overtaken PZU and Ergo Hestia, but in the field of voluntary insurance it is losing ground to the largest player on the market: KNF data indicate that PZU has 24.5% in third-party liability insurance and 31.1% in general liability insurance, respectively, while Warta's share is 26.5% and 24.5%.