Romania has the second highest rate of debt growth in the EU, a report shows. Bolojan admits that “we have borrowed rapidly in the last 5 years. We have loans of over 200 billion euros”

“On the basis of the loans registered by Romania, we ended up with credits of over 200 billion euros and we borrowed almost every year between 20 and 30 billion euros. Even if today Romania has a debt level of 60%, a debt level, our problem is that the interest rates paid by Romania are double those paid by other countries”, explained the head of the Executive.

Bolojan also stated that, by and large, “we paid interest rates that were between 7 and 8% in recent years and now we have lowered them very slightly below 7%, which means that, practically, the total interest rates we pay are as if we had a double degree of indebtedness”.

As debt rises, fiscal room for maneuver shrinks, as the knock-on effects ripple through a country's monetary policy, inflation and long-term competitiveness, a BestBrokers report says. Economists warn that when debt levels exceed 100% of GDP, the political space to respond to crises shrinks dramatically.

To understand the scale and pace of debt build-up in Europe, the BestBrokers team examined Eurostat's consolidated quarterly gross debt data, focusing on the first quarter of each year between 2015 and 2025. The report also tracks debt-to-GDP ratios to show whether economic output has kept pace with or outpaced borrowing.

The interest that Romania pays is almost 3% of Romania's GDP

“This means that next year, but also this year, the interest that Romania pays and will pay is almost 3% of Romania's GDP. So the interest we pay this year is approximately 55 billion lei, i.e. 11 billion euros, and next year it will reach 12 billion euros. Of the 6.5% deficit, practically half is occupied only with interest payments. If we do not reduce them, no matter who will be at government in the coming years, these interest expenses, we can't get out of this trap, we will end up in a dead end. That's why reaching the deficit targets is very important!” said the prime minister

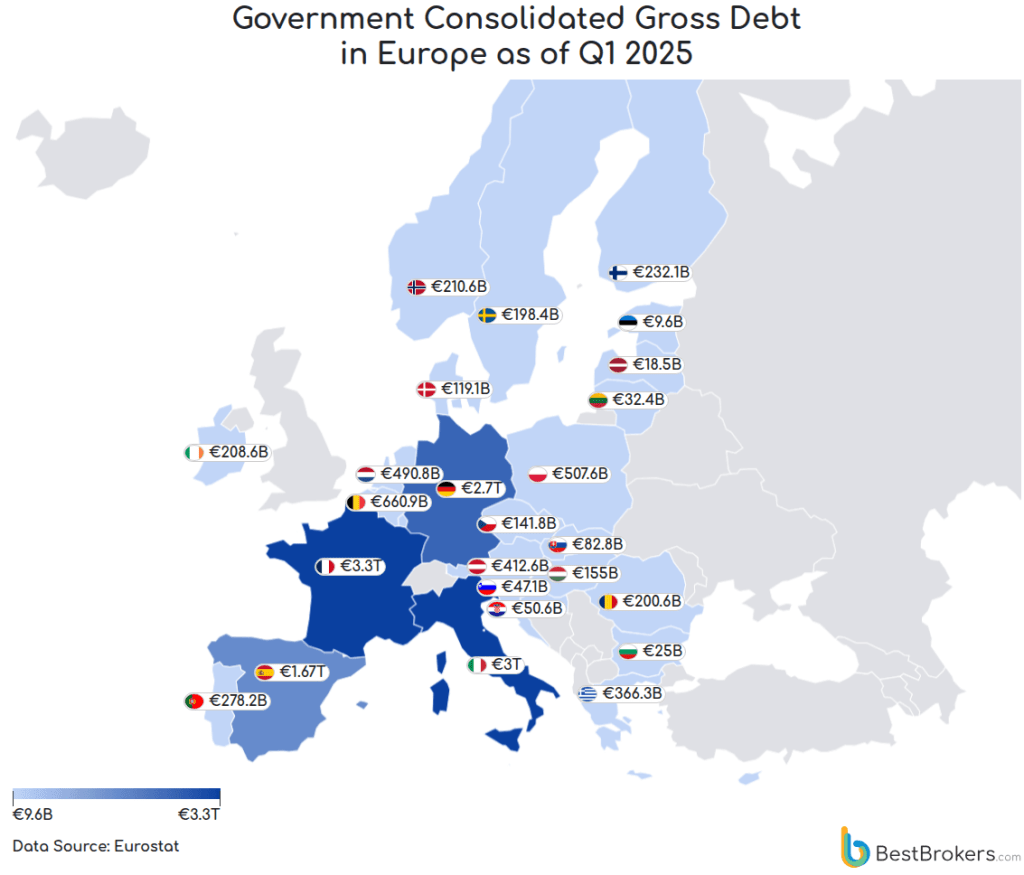

At the start of the first quarter of 2025, the collective national debt of the 28 European countries for which we found data stood at €15.2 trillion. However, three countries (France, Italy and Germany) account for almost €9 trillion of the continent's sovereign debt burden. The concentration of debt in the three largest economies of the euro zone presents a double risk: it amplifies the financial pressure on the EU bloc as a whole and complicates the European Central Bank's policy choices.

In short:

- France has the largest consolidated national debt in Europe, at around €3.3 trillion in the first quarter of 2025, equivalent to around 22% of the total debt of the 28 countries analysed.

- Greece, despite steady progress since its 2021 debt peak, still has the highest debt-to-GDP ratio in Europe at 152.5%.

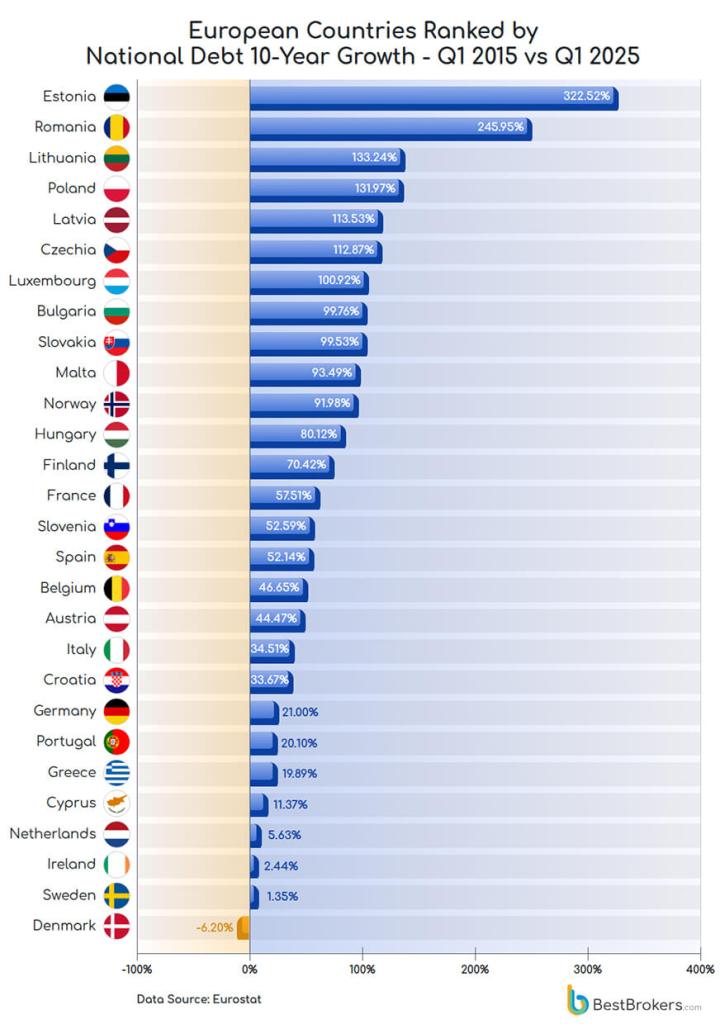

- Estonia has seen the largest percentage increase in national debt over the past decade, with a 322.52% increase between the first quarter of 2015 and the first quarter of 2025.

- Among the 28 European countries, Denmark is the only one whose public debt in 2025 is lower than it was in 2015. It fell by 6.2% in the first quarter of 2025 to 119.1 billion euros, compared to 127 billion euros a decade earlier

Public debt in Europe is far from evenly distributed. Instead, it is concentrated in a handful of large economies, each affected by its own fiscal history and policy choices. France tops the list with a consolidated gross debt of €3.3 trillion. In the second quarter of 2025 alone, public spending reached a record €167 billion, reflecting the country's deep-rooted commitment to expanded public services and social protection. This model protects households during economic downturns and also leaves some flexibility without politically painful budget cuts or tax increases.

The European Central Bank must act cautiously: rising interest rates could hurt debt payments, while easing policies risks fueling inflation.

Italy's €3 trillion debt stock is backed by one of the highest debt-to-GDP ratios in Europe at 137.9%. A substantial part of Italy's annual budget is absorbed by interest payments, making it difficult to invest in economic growth and reforms. Germany's 2.7 trillion euros have a different character. Much of this comes from deliberate borrowing to finance long-term investment: a €500bn infrastructure and investment programme, together with a temporary easing of the “debt brake” to finance defence, climate and digital projects, has pushed borrowing up.

Together, these three economies have debts of almost 9 trillion euros, about 59% of the total of the 28 countries analyzed. This means the European Central Bank needs to tread carefully: rising interest rates could hurt debt payments, while easing policies risks fueling inflation.

Belgium and Poland follow the “big three” with consolidated debts of EUR 661 billion and EUR 508 billion, respectively. Belgium's high debt per capita is remarkable given its smaller population compared to Poland. At the opposite pole, Estonia (€9.7 billion), Malta (€10.9 billion) and Latvia (€18.5 billion) illustrate how smaller economies can maintain low debt levels. However, low absolute debt does not necessarily mean low risk; these countries may be more vulnerable to external shocks, as even a modest increase in borrowing can suddenly change their credit profile.

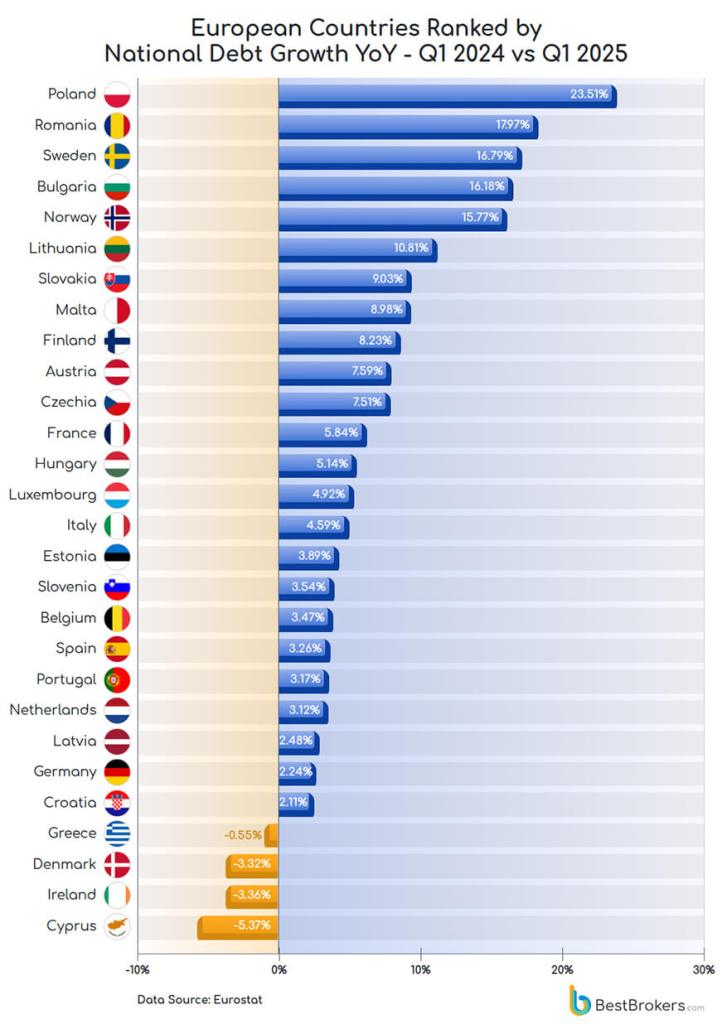

Poland leads Europe in national debt growth with record annual growth of 23.5%

Poland's national debt has seen its biggest increase in the past year, from €410.9 billion in the first quarter of 2024 to €507.5 billion in the first quarter of 2025, a staggering 23.5% increase in just one year. This growth can be attributed to a mix of ambitious infrastructure projects, extensive social programs and extensive economic stimulus measures. The country's proximity to ongoing geopolitical tensions has also led to a notable increase in military and defense spending, further contributing to the build-up of the national debt.

Romania follows a similar trajectory . National debt crossed the €200 billion mark in the first quarter of 2025, up 18% from €170 billion in the same quarter last year, reflecting comparable economic and security concerns across Eastern Europe.

Sweden (+16.79%) and Bulgaria (+16.18%) also saw a significant increase in debt. In Sweden, increasing spending on green energy initiatives and digital transformation programs drove growth, while Bulgaria's debt expansion reflects massive investments in transport networks, energy systems and digital infrastructure designed to align with EU standards and improve economic competitiveness as the country is in the final stages of joining the eurozone and adopting the euro as its official currency. Such spending can boost competitiveness in the long run, but leaves limited fiscal room for maneuver if economic growth slows or borrowing costs rise.

Only a few European countries managed to reduce their national debt between the first quarter of 2024 and the first quarter of 2025: Greece, Denmark, Ireland and Cyprus. These reductions are largely due to a combination of higher tax revenues, controlled government spending, and favorable borrowing conditions, which have allowed these countries to service their debt more efficiently than their neighbors.

Estonia outpaces the EU with a 323% increase in national debt over the past decade

Between the first quarter of 2015 and the first quarter of 2025, Estonia's national debt saw the steepest increase of all European countries, at 322.52%. The increase is largely driven by increased defense spending in response to regional geopolitical tensions. In 2024, Estonia allocated 3.4% of GDP to defense and security, a figure that is set to reach 5% by 2026, making it the largest defense budget in Europe as a percentage of GDP. Despite the rapid build-up, Estonia's debt burden remains relatively modest, at around 24.1% of gross domestic product in 2025.

The situation of Romania follows, with a national debt increasing by 245.9% over the decade, driven by increased borrowing to finance public spending. In 2024, its fiscal deficit reached 9.3% of GDP, the largest in Europe, raising concerns about long-term fiscal sustainability.

Other nations with sharp increases include Lithuania (+133.24%), Poland (+131.97%) and Latvia (+113.53%), where debt growth is fueled by infrastructure investment, expansion of social services and economic stimulus measures.

Denmark is the only European country to reduce its national debt in the last decade, recording a decrease of 6.2%. This achievement reflects disciplined fiscal management, restrained public spending and highly efficient tax collection, making the Nordic nation a strong role model for countries looking to stabilize or reduce their debt without undermining economic growth.