EKF Research and Deloitte report on the prospects for the insurance market in Poland by 2025

The mood among domestic insurers is not the best. As the latest report by EKF Research and Deloitte “Analysis of key factors influencing the development of the insurance market in Poland in a three-year perspective” shows, the sector is struggling with the accumulation of systemic risks: climatic, demographic and geopolitical, which outweigh the opportunities offered by the development of technology and digitalization.

The market sentiment is clearly worse

Sentiment analysis of the insurance industry in 2025determined as the difference between the 5 greatest opportunities and threats, indicates a deterioration in the mood compared to the previous year. The coefficient is currently -117.4 (-92.5 a year earlier) and illustrates the prospects for the insurance market in which negative rather than positive factors will be more important.

Although the mood of experts is not the best, according to the authors of the report, EKF Research and Deloitte, the macroeconomic environment over the next three years will be rather favorable for the insurance sector. Economic growth forecasts are stable, supported by falling inflation and unemployment, but there are also threats, such as the poor condition of public finances and the need to increase defense spending.

Advertisement

Opportunities for the insurance market, i.e. digitalization and economic improvement

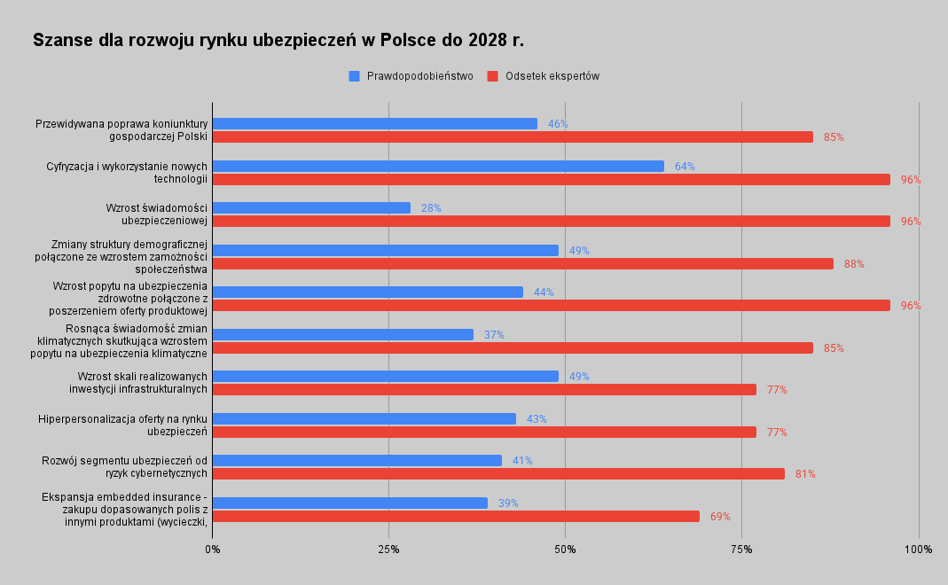

The study of the prospects for the industry was carried out in two stages: in the first stage, opportunities and threats for the insurance market were identified, and in the second stage, experts indicated both their importance and the likelihood of their occurrence. The most important opportunity for the development of the insurance market in Poland is digitization and the use of new technologies (AI) that can improve business processes. As many as 96% of respondents indicated this factor as important with a 64% probability of occurrence. The second important element for the industry turned out to be forecast improvement of the economic situationin turn the third increase in demand for health insurance combined with expanding the product offer.

The authors of the report also point to two important opportunities: changes in the demographic structure combined with the increase in society's wealth, as well as improved insurance awareness. Respondents mentioned, for example, issues related to climate change and the increase in demand for climate/catastrophe risk insurance and the development of cyber insurance.

Legislative burden and geopolitics among main concerns

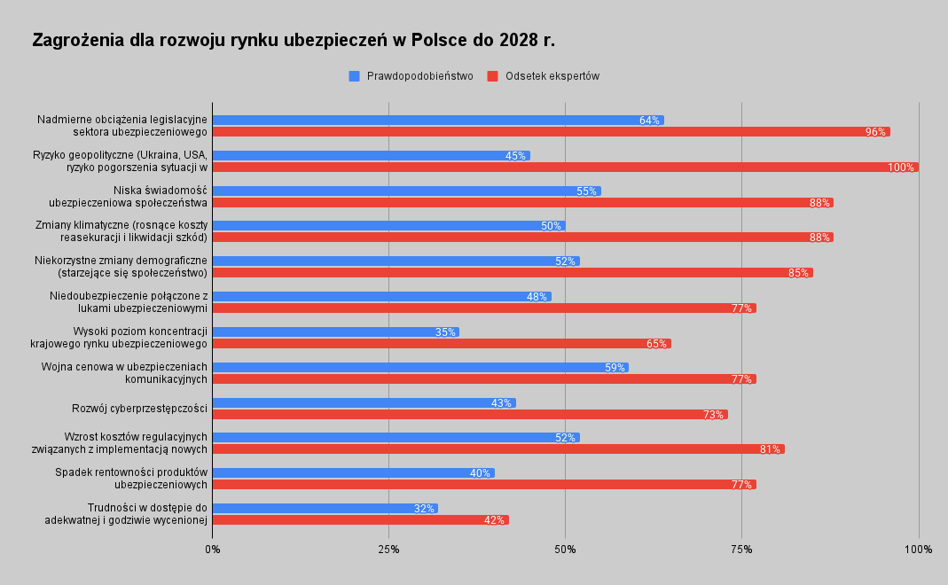

In addition to 10 chances, the surveyed experts indicated as many as 12 threats to the insurance sector, the biggest of which are excessive legislative burdens combined with regulatory uncertainty. For all respondents, the situation is an important factor geopolitical riskrelated to the conflict in Ukraine, the unstable situation in the USA and the risk of deterioration of the macroeconomic situation in Poland.

The threats of high importance and probability for the industry also include:

- climate change affecting the rising costs of reinsurance and loss adjustment,

- low insurance awareness resulting in little interest in voluntary policies and a predominance of compulsory insurance,

- price war in motor insurance and low profitability of this segment,

- unfavorable demographic changesmainly the aging of society.

Demography, climate and security are challenges for the market

In the opinion of Deloitte's expert, climate change means real consequences for the economy and the insurance market:

In Poland, the effects of climate change are becoming quantifiable: more and more frequent flash floods, storms and local flooding, as well as periodic droughts translate into an increase in the frequency and costs of damage to property, agriculture and infrastructure. For the sector, this means the need to adjust tariffs and sums insured, increase the use of reinsurance and catastrophe models, and develop new products – including: parametric and business interruption protection. Investments in prevention, better risk maps and data exchange with the administration become critical; without these elements, the protection gap will remain high and premiums will remain more variable. – comments Marcin Warszewski, FSI Insurance Leader, Partner, Deloitte.

Dominika Kozakiewicz, CEO of Aon Polska, quoted in the report, points to demographic changes as a challenge for the market, affecting e.g. medical insurance or young people's interest in property insurance. Catastrophic risks are also an important area, as they are based mainly on the insurer's risk and are poorly reinsured, while the third challenge is war, terrorism and cybersecurity.

These are complex threats that cover large areas and interconnected interests of states, communities and businesses. There is an ongoing debate about the insurability of war, as insurance, by definition, applies to events that are sudden and uncontrollable by humans. There are clauses on the market that, for example, protect transported goods or export credits – but they concern territories exposed to the outbreak of war, and not already covered by a full-scale conflict. – says Dominika Kozakiewicz, CEO of Aon Polska.

The market and its environment must change

Pessimistic sentiment prevails among insurance market experts, however, the report by EKF Research and Deloitte also includes important recommendations for the sector in a three-year perspective. They were formulated in 6 points:

- Actions for increasing insurance awareness – educational and information campaigns, cooperation with public institutions.

- Actions for increasing trust in the insurance sector – simplifying the General Terms and Conditions of Insurance, introducing contract standards, adapting the product to the customer, minimizing liability exclusions.

- Digitization and technological development combined with increased resistance to cyber risks – investments in new technologies, strengthening resistance to cyber risks.

- Reducing regulatory burdens and increasing legislative stability – dialogue between the market and its regulators and deregulation.

- Development of the offer in the field of health and pension insurance combined with tax reliefs supporting the development of health and pension insurance – adapting the offer to the needs and wealth of customers.

- Increased importance ESG in the business model – integrating ESG with product policy.

A separate part of the report was the topic of ESG in insurance. The sector recognizes climate risks, including them in calculations and the offer itself, but preparation to implement solutions is moderate.