China and India have 35% of the world's population and will soon be two of the world's three largest economies. Despite so many similarities, both countries have different approaches to the national currency: the Indian one is junk, while the Chinese one aspires to the role of a global reserve currency.

By 2024, India's gross domestic product has approached $4 trillion. Indians have recently overtaken Great Britain and today in terms of total GDP (calculated at official exchange rates) they are second only to Japan (USD 4.03 trillion). As well as Germany ($4.66 trillion), China ($18.7 trillion) and the United States ($29.2 trillion).

For several years, Indian GDP has been growing at a real rate (after taking into account inflation) of 5-10% per year. At this rate, the Indians will probably overtake Japan this year, and in 2-3 years they will overtake Germany. Of course, it will still be a much poorer country than both industrial powers mentioned above. After all, India's GDP produces almost 1.4 billion people, while the population of Germany is 83.6 million and Japan's is 120.7 million.

Everything indicates that in the next 20-30 years (further forecasting no longer makes any sense) only three countries will be important in the world economically: the United States, China and India (though not necessarily in that order). If we take currency blocks into account, the euro zone will probably also join us, but its growth rate has been practically zero in the last few years.

Two currency paths

However, this article is not about who (and when) will be the greatest, but rather about how they got there. There are many differences between the economies of China and India and we will focus on only one here. That is, on the issue of currency. In the case of China, the matter is quite obvious. Beijing has been concerned about the value of its currency since the mid-1990s. In the years 1993-2004, a virtually rigid official exchange rate was maintained for the dollar, which at that time cost USD 8.10-8.70. After 2006, Beijing allowed the yuan to appreciate under the supervision of the authorities.

As a result, in 2014 the official USD/CNY exchange rate stopped at almost six yen per dollar. And although the renminbi has since tended to weaken against the US dollar, it remains relatively strong. It is enough to recall here that the years 2014-22 are a period of strength of the “green” in relation to other major convertible currencies (maybe with the exception of the Swiss franc). During this period of dollar hegemony, the USD/CNY rate never exceeded 7.50 yuan.

The Chinese authorities also care about the stability of their equally important currency pair. The euro-yuan pair has been moving mainly sideways for almost two decades, remaining in the range of 6.50-8.50 yuan per euro. And although the yuan has weakened slightly in the last three years both in relation to the euro and the dollar, it still retains its relative value quite well for an emerging market currency.

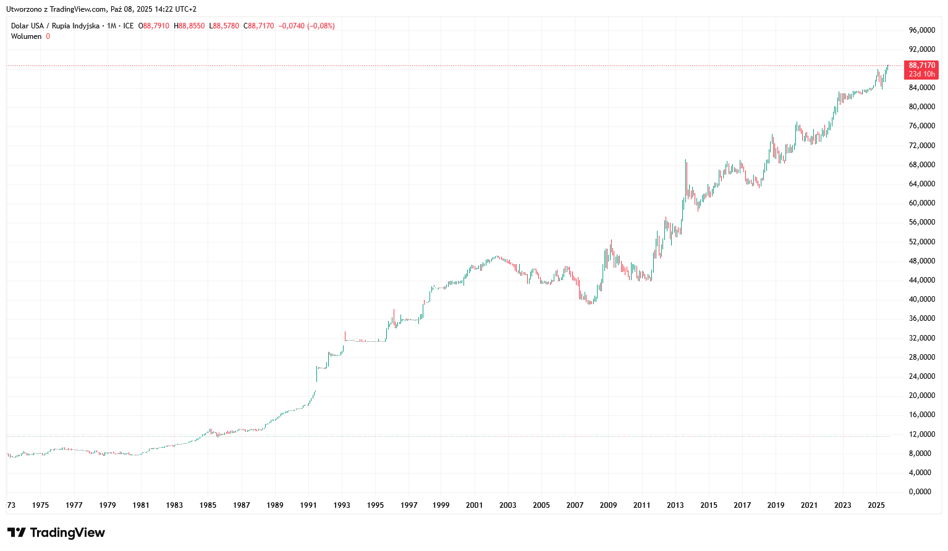

The same cannot be said about the Indian rupee, for which no shameful monetary epithet will probably be exaggerated. When choosing almost any period on the USD/INR chart (i.e. the price of 1 US dollar expressed in Indian rupees), it is difficult to find a clearly declining period – i.e. a time of appreciation of the Indian currency. It has been losing value almost continuously since the early 1980s. During this period, the dollar rate in India rose from approximately 10 rupees to nearly 90 rupees today.

However, let's leave the distant past behind and take a closer look at India's monetary history. Tentative attempts to stabilize the rupee at the beginning of this century ended with the escalation of the global financial crisis in 2008. Since then, few things are more certain in India than the fact that the rupee will lose in relation to the USD. In the previous 15 years, there was only one year in which the Indian rupee appreciated against the dollar. It was 2017, when global capital “remembered” about emerging markets for a short time and its inflow lifted all the boats in the port. Even the Indian rupee, which gained 6.3% that year. However, in all other years in the period 2011-25, the rupee ended in negative territory, and the dollar almost doubled in price during this time.

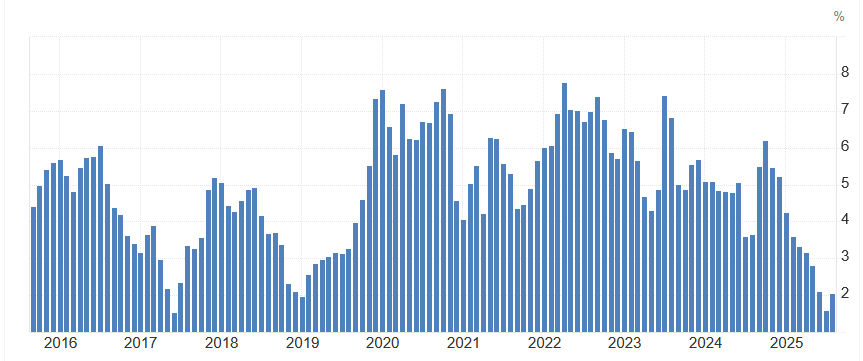

The barely 15-year half-life of the national currency does not reflect well on the Indian authorities in general and the management of the central bank in particular. The rupee's weakness against the dollar is not surprising if we look at historical consumer inflation statistics. In the previous 50 years, it only occasionally fell below 5% and often exceeded 10%. In the previous 10 years, Indian inflation could exceed 7%, but also fall below 2%.

Since 2016, the Reserve Bank of India's inflation target has been 4% with a permissible deviation of two percentage points up and down. Considering historical “standards”, the RBI has been monitoring inflation quite well for several years, which is generally kept below 6%. Of course, this is nothing to be proud of, because 6% inflation is a merciless destroyer of the purchasing power of money. At this constant rate of inflation, money loses half of its purchasing power in just 11 years. And after 20 years it is only worth 29% of its initial value.

Despite this, the rupee continues to weaken. This year it has already lost almost 3.6% against the already weakening dollar globally. On October 2, the American currency in India was at a record price and cost almost 89 rupees. Analysts have no shortage of explanations for this situation. This is about the pressure resulting from the growing demand for dollars needed to import gold. India is, next to China, the largest consumer of gold in the world, and gold jewelry is almost a basic necessity for Indians. But unlike the Middle Kingdom – which ranks first in the world in terms of gold mining – India has to import almost all its gold. And since the royal metal is record-breakingly expensive and has gone up in price very much (by as much as 48% only in 2025), Indians need significantly more USD to import the same amount of yellow metal.

An additional risk factor for the rupee is the proposed significant increase in the cost of obtaining an H-1B visa, allowing foreigners to work legally in the United States. President Trump would like to collect as much as USD 100,000 for such paper – 50 times more than currently. Such a move would probably force some Indian employees from the IT sector to return to the country. And this, in turn, would mean a reduction in the flow of dollars that immigrant workers send to their families back home. Economists from Capital Economics estimate such transfers at $120 billion annually, which constitutes as much as 3.4% of India's GDP.

Rupee in the trash, yuan in the throne?

Regardless of how things turn out in the short term, in the long term the Indian rupee is a whipping boy for the Chinese yuan. This year alone, the rupee has lost 6.1% against the PRC currency. Over the last 5 years, it has weakened by 12%, in a decade it has regained 17%, and over the previous 20 years it has lost more than half (i.e. 55%).

If this trend does not change, in a dozen or so years the rupee will again lose half its value compared to the Chinese yuan. And this is assuming that it does not advance to a higher currency league. In the previous decade, Beijing tried hard to internationalize the yuan, which resulted in partial success in the form of its entry into the Special Drawing Rights on October 1, 2016. This opened the gate to the vaults of some central banks, which began to keep part of their foreign exchange reserves in Chinese currency.

However, as of 2020, the internalization of the yuan has stopped. The share of the renminbi in global foreign exchange reserves has stopped at just over 2%. That is even less than half of the British pound and similar to the Australian dollar. The yuan is doing slightly better on the global currency market share front. According to this year's study by the Bank for International Settlements (BIS), the share of the Chinese currency in global Forex turnover reached 8.5%, which puts it in fourth place among the most frequently traded currencies in the world. This is 1.5 percentage points more than in the previous study of this type from 2022 (BIS conducts it every three years).

However, the yuan still lags far behind the euro and the US dollar. However, this may be enough to further drive away the Indian rupee, in which even Indians are not keen to keep their savings, sensibly preferring gold in this respect. And although the current Indian authorities aspire to the role of a world power, it will be a bit embarrassing to show such a currency in showrooms.