The mortgage market has returned from a long journey. For the first time since the “safe loan of 2 percent” you can see two -digit quarterly increases. The latest Amron-Sarfin report also brings puzzling data on customer elections.

The Association of Polish Banks and the Amron Center have just been presented to a report summarizing the second quarter of 2025 on the mortgage market. The authors of the document point out that a new chapter is opening. After a period of balance, shaken by a afterburner in the form of a “safe loan 2 percent”, stabilization and now, revival. This time they have roots in fundamental factors, such as falling interest rates and sliding real estate prices.

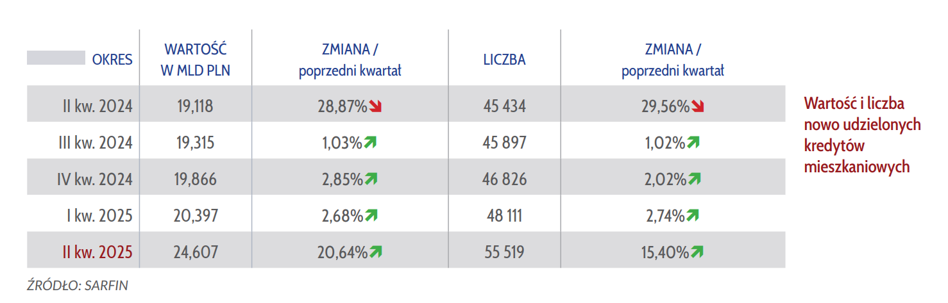

In the second quarter of 2025 Banks granted 20.6 percent more financing than in the first three months of the year. In comparisons year on year The dynamics is also double -digit and loud +28.7 percent “This may be a preview of a new credit action record in the dimension of the volume of loans granted,” indicates in the introduction to the report by Jacek Furga from ZBP.

Also in terms of the number of contracts signed, the second quarter looks great. Banks have obtained together 55.5 thousand contracts. This means an increase of 15.4 percent. Quarter to the IO quarter 22.2 percent year on year.

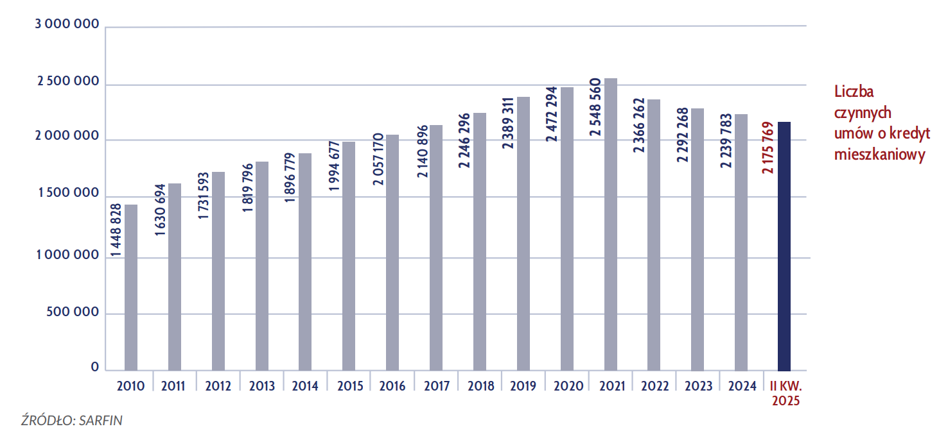

However, great sales results did not cross the long -term trend – Poles still get rid of housing obligations faster than new ones. In the middle of the active year, 2.17 million mortgage loans remained. This by 4.55 percent less than a year earlier IO 0.76 percent less than at the end of March 2025.

The image of the wallet looks different if you look at the value of debt from housing loans. For the first time since the record 2021, the sum of the mortgage debt exceeded PLN 500 billionreaching PLN 500.4 billion. This means an increase of 1.27 percent. Compared to the first quarter of the year, and 2.5 percent In combination with data from a year ago.

Mysterious love for a permanent percentage

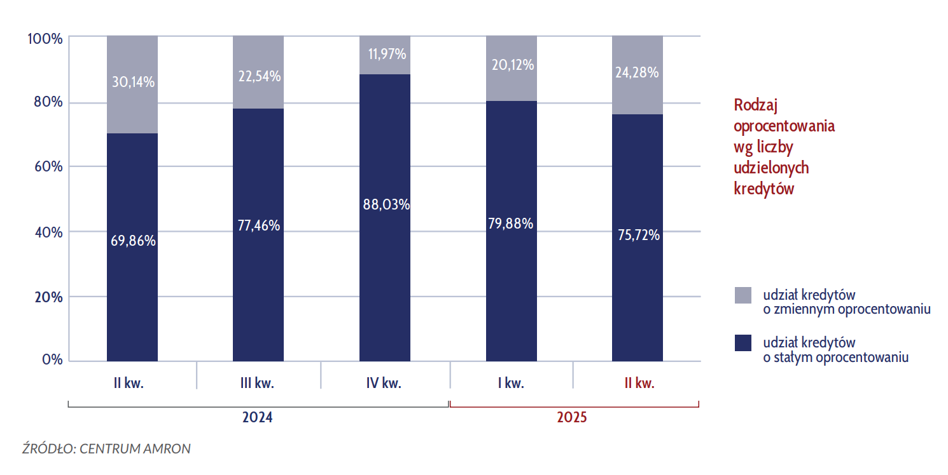

By far the most interesting point in the Amron report are the latest data on borrowers' preferences. We would like to remind you that in the first quarter of the year, when interest rates were already looming on the horizon, mortgages based on periodically constant interest rate were responsible for almost 80 percent. sales (quantitatively). It could be expected that along with the materialization of the announcement about cutting the feet, interest in a fixed foot will definitely fall. However, nothing like that happened.

Over 75 percent new contracts in Q2 were loans with a period of periodically a fixed rate. This product had a slightly lower share in a valuable basis, responsible for 74.3 percent. financing.

Compared to the first three months of the year, interest in a fixed interest rate has dropped slightly (reduction of share by 4.49 percent in the number of contracts), but And so it was higher than a year agoand solid 6.54 percent In the report, these results did not get comment, although at first glance they seem puzzling. The price policy of banks may be partly responsible for the tendency to “percent” elections (the fixed interest rate is initially lower), but this is probably not the only factor.

Low own contribution on the wave

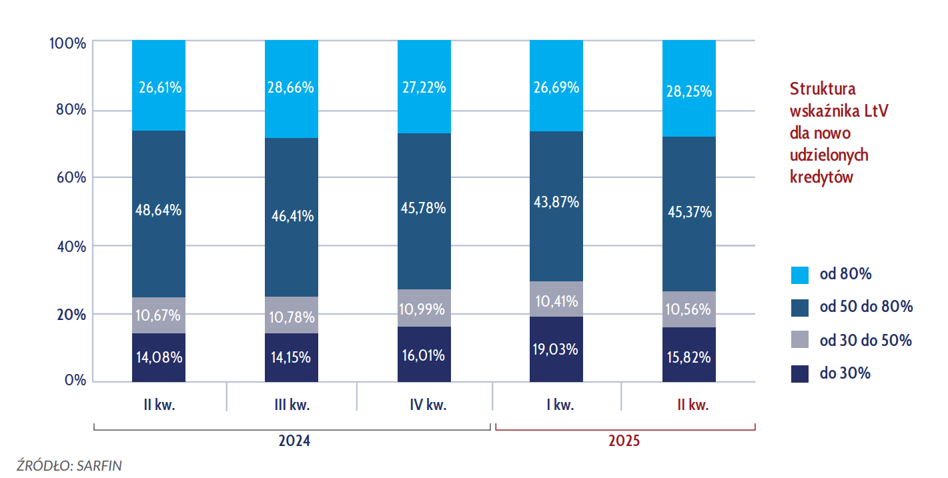

“The share of loans with an LTV indicator above 80%slightly increased. Their percentage increased by 1.56%, to the level of 28.25%. It is also a disturbing signal to extend the incidence period of newly granted loans. Compared to the results listed in the second quarter of 2024, by 4.5 pp, the share of loans between 25 and 35 years old increased by the inclusion The most important changes in the mortgage sales structure have been summarized.

After two quarters of a decline, again the share of loans with a own contribution below 20 percent exceeded the limit of 28 percent. At the same time, the category of liabilities with the highest own contribution (70 percent), which corresponded to the end of the second quarter for 15.8 percent. new loans.

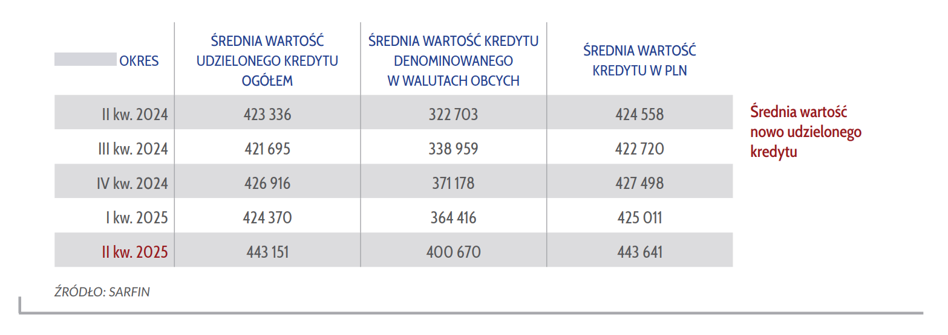

Average value of a new loan At the end of June it was 443.1 thousand zloty. After a one -time decline in the first quarter, this indicator climbs up again. The increases were determined – by 4.43 percent Quarter to the IO quarter 4.68 percent year on year.