The July data on CPI inflation was adopted as a good coin (intended irony) and raised the S&P and Nasdaq to new records of all time. Traditionally, the increase was based on Quasi-Monopoli technological actions.

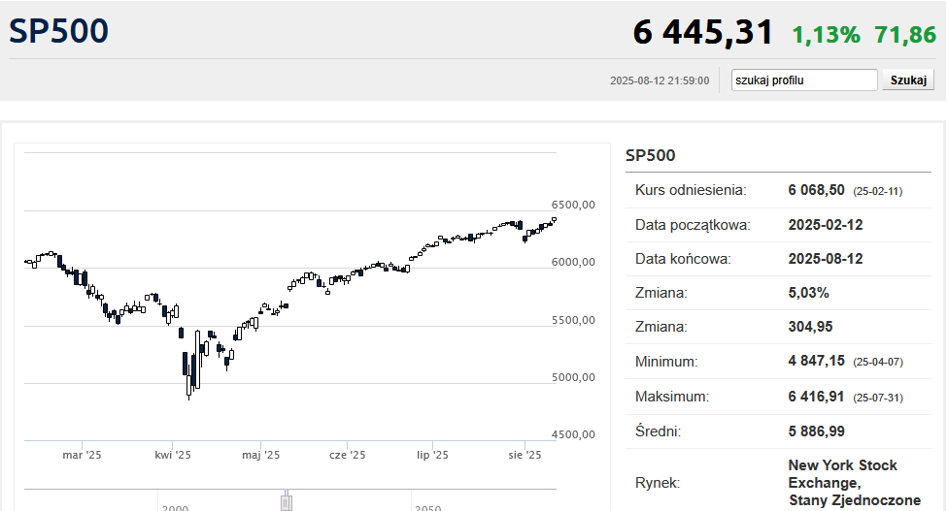

S&PC ended Tuesday trade at 6445.76 points, which means an increase by 1.13% and at the same time The highest closing course in history (as well as the intra -seis record located at 6446.55 points.

The new Hossa peak and at the same time a new historical record also broke by Nasdaq, which, having gained 1.39%, registered at the level of 21,681.90 points. The industrial average of Jones has grown by 1.10%, but the result at 44,458.61 points. It was over 600 points lower than the July summit.

Advertisement

Mainly all the technological giants' actions were expensive and they pulled the stock indexes up. Such a metal went down by 3.2%, Broadcom gained 2.9%, and Microsoft and Alphabet grew over 1%. It is also worth paying attention to the strong attitude of the banks. Citigroup quotations increased by 4.1%, the values of Bank of America went up by 2.8%, Wells Fargo by 2.4%, and Goldman Sachs by 3.4%.

The nail of the Tuesday program of the day on Wall Street was the July report on CPI inflation. The data turned out to be a bit strange and as if inconsistent (about that in a moment). Thanks to the cheaper gasoline, the “wide” consumer inflation rate was “only” by 2.7% higher than a year ago. It is still far above the 2%target of the federal reserve (and the same as in June), but economists selected a reading of 2.8%.

The fact that CPI inflation did not increase in July pleased investors because it was feared that it was in the previous month that we would see the first effects of the import duties of President Trump. And because the evidence of the support of this hypothesis lacked, the term market increased the chance of a chance for a September reduction in federal funds from 84% to 94%. Completely ignoring the fact that CPI base inflation (i.e. everything without food and energy prices) rose from 2.9%to 3.1%, while 3.0%were expected. President Glapiński after such data in his life would not be on interest rates.

It is worth mentioning that monthly dynamics – both in the case of full CPI and the base – proved to be perfect with the expectations of economists. Thus, the differences between data and consensus on annual dynamics had to result from either revision or the issue of rounding.

– CPI data is generally support for the stock market. This is good news that the Fed is on the path to the September foot cut and potentially more temporary inflation – said Katherine Bordlemay from Goldman Sachs Asset Management, trying to explain the Tuesday market reaction to Tuesday's reaction.

It is worth noting that the profitability of 2-year US government bonds (i.e. short-term, most sensitive to foot changes in Feda), however, decreased only by 4 PB, descending to 3.74%. The current range of federal funds rate is 4.25-4.50%. The market speculates that by the end of 2026, feet in Feda will fall around 3%. The reaction of the currency market was also quite moderate, where the EUR/USD exchange rate went up (i.e. the dollar weakened against the euro), but it was not an increase in excessively impressive and we suddenly returned to the States at the end of last week.

To sum up, the Wall Street reaction was much stronger than the other market segments, which generally quite calmly adopted data on the July CPI inflation. Malicious also add that President Trump did not release the previous boss of BLS, so that now the same work statistics office would publish data about the growing CPI inflation.