In March 2025, in seven major Polish cities (Warsaw, Kraków, Poznań, Wrocław, Tri -City, Łódź, Katowice), developers offered over 2,000 houses, which means an increase of 4 percent. Compared to the previous quarter and by as much as 18 percent year on year. The average price per sq.

The situation is a bit different when we also include agglomerations. The total offer of development houses at the time was 6100, which means a small quarterly increase (0.5 percent), but at the same time a clear decrease in annual terms (-14 %). The average price in this segment amounted to PLN 9,000 per sq m (+2 percent sq m, +8 percent year -on -year).

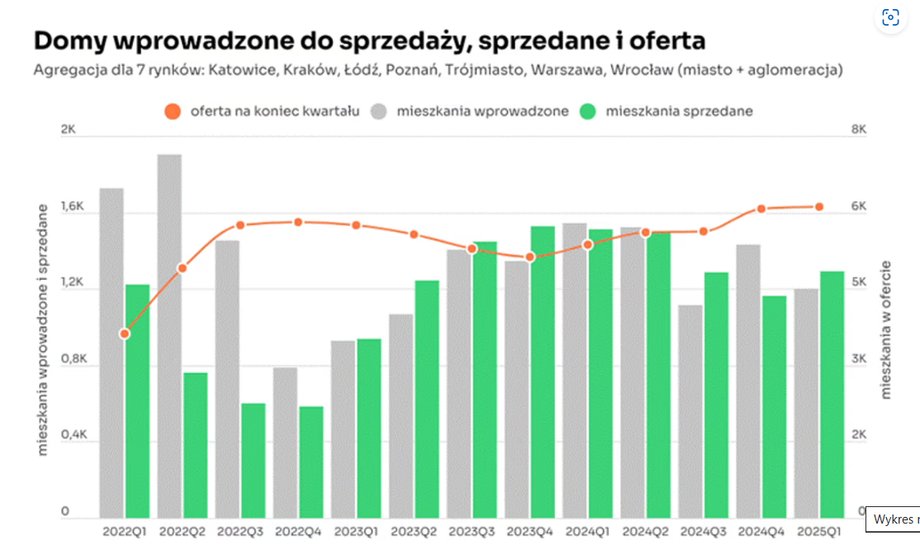

In the first quarter of 2025, developers introduced 440 houses on seven main markets, which is an increase of 20 percent. Compared to the previous quarter, but at the same time a decrease of 8 percent. compared to the same period a year earlier. Sales during this period amounted to 370 houses, which means a decrease in both quarterly (-17 percent) and annual (-19 %).

Sales strategies of developers

In response to a reduced demand within the city limits, developers introduce various strategies to stimulate sales. They are increasingly common:

- discounts and price promotions,

- additional incentives in the form of free parking spaces,

- innovative ecological solutions in standard,

- Smart Home systems.

At the same time, developers show caution in launching new investments. In the first quarter of 2025, they introduced 1,200 new houses to the market (taking into account cities and agglomerations), which means a 16 % decrease. Compared to the previous quarter and by as much as 22 percent. year on year.

Houses put on sale, sold and offer

|

Otodom.pl / otodom.pl

Increased interest in the suburbs

It is worth noting a positive signal flowing from sales data in agglomerations. In the first quarter of 2025, 1300 houses were sold there, which is an increase of 11 percent. Compared to the previous quarter, despite the fact that a 15 % decrease is still recorded in an annual basis.

– It is worth emphasizing that both market segments go to various groups of recipients – people choosing houses within city borders value a convenient location, comfort of living in a house instead of living in a block of flats and are ready to bear higher costs to get a house in attractive, convenient locations – says Agata Stachowiak, an expert in the Otodom real estate market.

– Meanwhile buyers looking for houses in agglomerations are more sensitive to costsfocus on economic solutions and are willing to give up the location in favor of lower prices – he adds.

Regional diversity

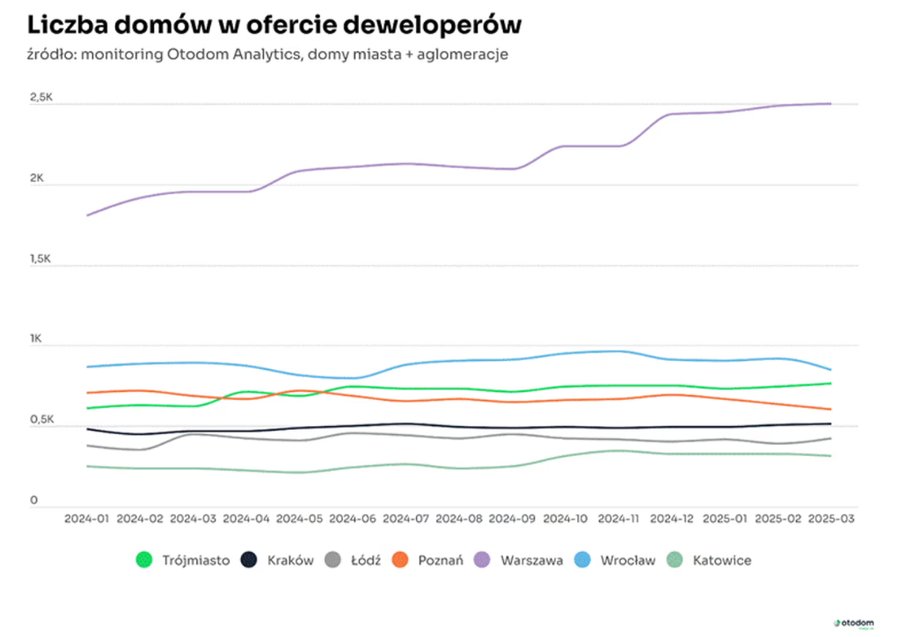

In an annual basis, most of the analyzed cities together with agglomerations recorded an increase in the offer of development houses. The highest increases were recorded in Katowice (+33 percent year -on -year), Warsaw (+28 percent year on year) and the Tri -City (+22 percent year on year). On the other hand, in Poznań (-12 percent year on year) and Wrocław (-5 percent year on year) the offer decreased.

A decrease in the number of new houses put on sale is particularly disturbing. Compared to the first quarter of 2024, the new supply fell in Poznań and neighboring poviats by 61 percent, in Wrocław and the agglomeration by 38 %, and in Warsaw and the surrounding area by 25 percent.

Number of houses in the offer

|

Otodom.pl / otodom.pl

– Developers have adopted a more cautious investment strategy. They also noted weaker results in the category of houses sold. The decrease in sales suggests the possible impact of macroeconomic factors, such as higher interest rates, more difficult availability of mortgage loans and an increase in living costs – he explains Agata Stachowiak from Otodom.

Sales by regions

Despite the overall decline year -on -year, the quarterly comparison shows the increase in sales in four of the seven analyzed regions:

- Warsaw and agglomeration: +27 percent sq.

- Katowice and surroundings: +19 percent sq.

- Wrocław and agglomeration: +11 percent sq.

- Poznań and its surroundings: +10 percent sq. to KW.

In Łódź and the agglomeration, sales remained at a level similar to the previous quarter, while in the Tri -City and the surrounding area it fell by 6 %, and in Krakow with an agglomeration by 15 percent.

Price dynamics

The highest annual price increases were observed in Poznań and Warsaw. Poznań and the agglomeration recorded an 11 % increase, which indicates the growing attractiveness of this region. In Warsaw and the surrounding area, prices increased by 10 %, thanks to which the capital again became the most expensive market with a price of PLN 10,400 per sq m.

Katowice and Łódź also recorded significant price increases, respectively by 8.5 and 5 percent The Silesian region attracts the attention of both residents and investors, thanks to the still relatively low price (PLN 7,100 per sq m) and developing infrastructure. In the Tri -City prices increased by 4 percent, while in Wrocław and Krakow increases were minimal and did not exceed 1 percent.

Market perspectives

Data from the first quarter of 2025 indicate a careful approach of developers to new investments, which may be a reaction to earlier slowing down sales and challenges related to the absorption of available offers. At the same time, the increase in quarterly sales in most regions gives grounds for moderate optimism.

Macroeconomic factors, such as high interest rates or more difficult availability of mortgage loans, still affect purchasing decisions of potential buyers. In this situation, developers must demonstrate flexibility in adapting the offer to changing customer preferences, increasingly choosing suburban locations offering a better value for money.