publication

2025-05-26 06:00

Consumer bankruptcy has entered a new stage. The number of bankruptcies has ceased to grow, but also does not decrease. The April results confirm that the rush initiated by the liberalization of the law was exhausted and the time has come for stabilization.

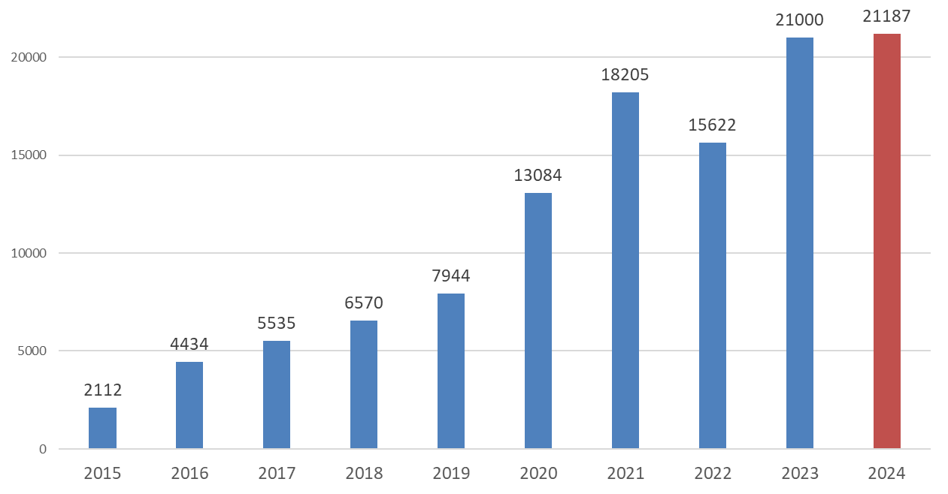

In recent years, we have observed an almost continuous increase in the number of consumer bankruptcy. Each of the subsequent periods brought a historic record, except for 2022, when procedural changes in bankruptcy occurred and some of the debtors “got lost” in the digital trial. However, it seems that the rush has run out and this year the records will not be repeated.

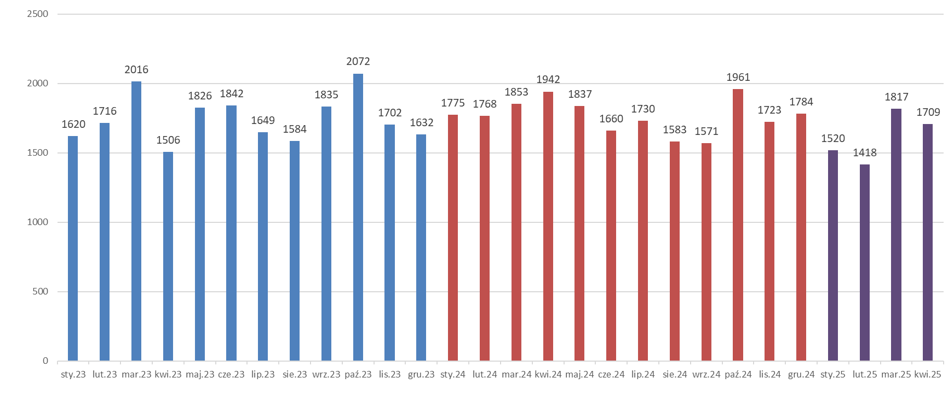

The latest data published by the Central Economic Information Center shows that in 1709 people announced bankruptcy on April 2025. Compared to the same period of the past year, this means decrease by almost 12 percent.

Assuming that in the following months the number of advertisements for consumer bankruptcy will be similar to the calculated period calculated for the period January-April, it can be expected that the year 2025 will close the result below the trend recorded in 2023 and 2024 below.

Bankruptcy in three phases

After 2015, the bankruptcy option became more widely available to the average debtor and it can be considered that this date begins for the good history of this institution in Poland. The first stage of bankruptcy development was the gradual increase in the number of advertisements with a slight interest in the procedure by 2020. At that time, legal regulations at that time discouraged some debtors, who in other circumstances would probably decide to bankrupt.

In 2020, new regulations entered into force that gave people a chance and contributed to insolvency. The debtor's fault is no longer a key barrier and does not affect the possibility of bankruptcy. However, it has a role in determining the conditions for the implementation of the repayment plan and possible debt relief.

The revolution in law coincided at the beginning of the pandemic and closing the economy. The effects of liberalization came with a delay, but they had a spectacular nature – the number of bankruptcy announcements doubled in the second half of 2020.

From 2023, increases had a less dynamic course. Still, consumer bankruptcies were coming, and in 2024 their number slightly broke the record set a year earlier. After the stabilization stage, we will probably observe a slight landslide, the signal of which is the results of the first months of 2025.

Where can stabilization come from?

For consumer bankruptcy, several groups of debtors of various motivation reach. These are both “consumers” in the full sense of the word, never conducting business activity, as well as people who, after defeating business, must take advantage of the emergency exit as a natural person. In the first group there is probably a certain percentage of people falling due to purely random reasons (e.g. loss of work capacity and incurred with earlier debt), as well as those who have converted, incurring commitments, but have paid abilities.

If there are no dramatic changes in the environment, such as a rapid deterioration of the economic situation and an increase in unemployment, then you can hypothesize that there is a certain “organic” level of interest in bankruptcy. In other words, the number of people falling into trouble will oscillate around a certain average value. Stabilization or improvement of the economic situation will be reflected in the stabilization of the number of bankruptcies.

In this context, as a pre -emptive indicator, you can treat the data on the quality of repayment of loans published by BIK. In recent months, an office notes the improvement of all measures. In March, the indexes were better than a month earlier in each segment – from cash loans from housing loans.