Silver does not forgive: the Hunt brothers, “Silver Thursday” and the replica of 2026 – when regulators put the brakes on the bubble

In the 70s, the Hunt brothers, very wealthy investors, concluded that inflation would erode the value of the US dollar, writes economist Laurian Lungu, co-founder of the think tank Consilium Policy Advisors Group (CPAG) in an analysis sent to HotNews.

At that time US citizens were prohibited from owning gold so the Hunt brothers chose silver, which was then trading at around $1.50/ounce, as a speculative hedge. They decided to protect their wealth by trying to corner the silver market. The price of silver rose from around $6/ounce in early 1979 to a peak of $50/ounce in January 1980 — an increase of about eight times in a single year, writes the Romanian economist.

At their peak, the Hunt brothers controlled the equivalent of nearly 70% of the world's silver.

In January 1980, Commodity Exchange Inc. (COMEX) introduced “Silver Rule 7” to stop speculation, imposing severe restrictions on margin trading and subsequently the “liquidation only” regime. This triggered the price crash on the so-called “Silver Thursday” (March 27, 1980), when silver fell 50% to $10/ounce, 80% below the high reached just two months earlier.

Following this episode, Laurian Lungu's analysis shows, numerous banks and trading firms that had financed the Hunt brothers' positions also fell into financial difficulty, generating a second wave of bankruptcies and mergers. The Federal Reserve (FED) had to step in to allow an orderly liquidation of silver positions.

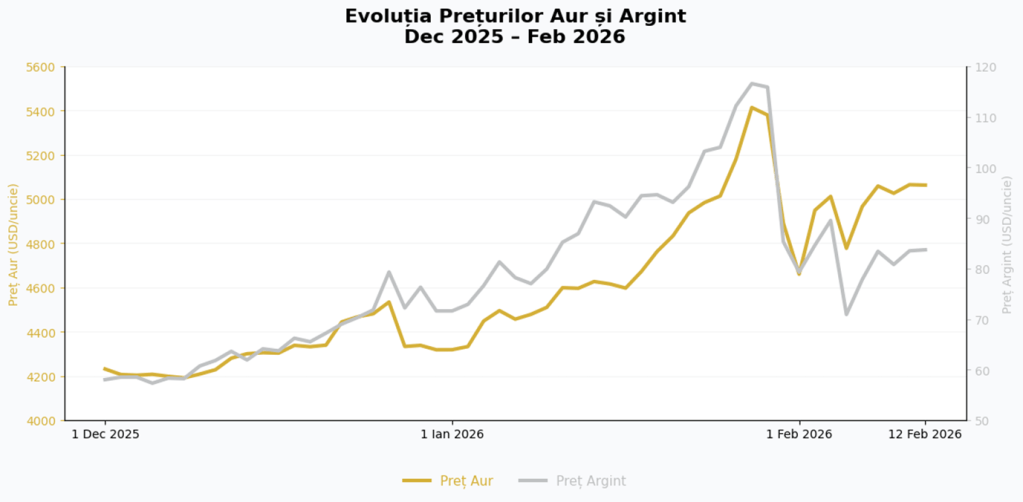

The lessons of history are always useful. Silver's recent 26% one-day drop at the end of January 2026 has striking parallels to the 1980 episode

There was a speculation-fueled parabolic rally in the price of silver — eight times then and three times in a year in 2026 — fueled by heavily leveraged investors who couldn't afford margin calls. This triggered a “liquidation only” dynamic, with forced sales and a lack of new buyers. The result was a dramatic one-day collapse as leverage dissipated.

The silver price adjustment was triggered by regulators, by changing margin requirements (margins being the security deposits needed to cover potential losses).

The Chicago Mercantile Exchange (CME) switched, in January 2026, to a percentage-based margin system, increasing maintenance margins up to 15% for standard positions — thus continuing the process of increasing margin requirements started in September of the previous year, says the Romanian economist. The mechanism was similar to the “Silver Rule 7” of the 1980s. The Shanghai Futures Exchange also widened margins, albeit at a more moderate pace.

The classic lesson is that regulators have the power to end speculative bubbles by changing the rules during the game

When they increase margins in a highly leveraged (ie high leverage) market, they can force a self-feeding cascade of liquidations. This is exactly what happened in 1980 and it happened again in January 2026.

Another lesson is that globalization involves risks when regulatory standards differ. There was a veritable speculative frenzy in China, with investors flocking to precious metals through platforms — some unregulated — that offered leverage of up to 40 times, according to the CPAG co-founder. This meant that the required margin was sometimes only one fortieth of the spot price.

Leverage has an inverse relationship with the margin requirement. It was no surprise that there, silver rose 60% in just four weeks, while a number of other assets — including gold, palladium and bitcoin — were used as investment assets.

China controls about two-thirds of the global physical silver supply, being the largest consumer

China controls about two-thirds of the global physical silver supply, being the largest consumer for solar PV modules, electronics and electric vehicles. Before the crash, physical silver in Shanghai was trading at a substantial premium to “paper” contracts. In theory, arbitrage should have been simple: you bought silver on the COMEX, delivered it to Shanghai, and made the profit, after deducting shipping costs. In practice, however, the mechanism stalled because there was not enough physical silver available to be delivered.

COMEX, like other exchanges, operates on a fractional reserve system. The number of “paper” silver contracts in circulation is about 300 times more silver than is physically held in COMEX warehouses. Given the high demand and in reaction to global trade tensions, China imposed export licensing requirements in early 2026.

The arbitrage opportunity generated by the difference between the price “on paper” and the physical one has been extraordinary and without historical precedent in recent weeks. Between early and mid-January, in a single week, over a quarter of the COMEX's recorded inventory evaporated as it was physically withdrawn for delivery. And silver stocks on the Shanghai Futures Exchange (SHFE) fell to their lowest levels in a decade, reflecting the sharp tightening of the global physical silver market.

Currently, the silver market is still in a self-correcting process

The crash of January 2026 eliminated over-indebted speculators, and the likelihood is that markets where physical demand is stronger — such as China — will gradually develop an alternative price formation system. If a large enough portion of the physical market moves to London, Shanghai, Dubai and other delivery centers, COMEX contracts may become less relevant to actual physical transactions. On the other hand, demand for silver from companies that use it as an input could decrease as alternative materials are used.

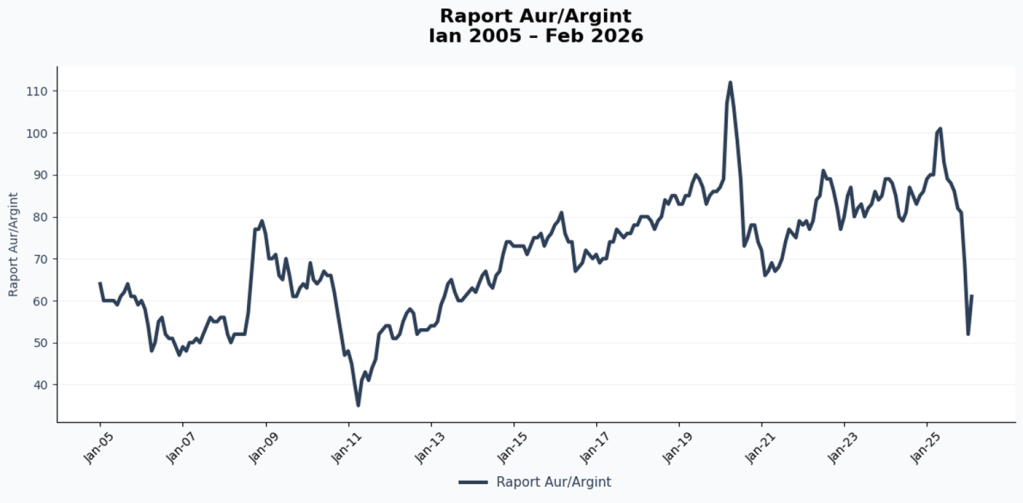

Gold has also rallied strongly in recent months, largely due to geopolitical uncertainties and fears of bubbles forming in certain stock markets. However, gold has much deeper physical markets, which allows it to absorb shocks more easily, is used to a much lesser extent in industry — where price is a major obstacle — and benefits from more stable demand from large institutions such as central banks. The average gold/silver ratio was around 70 between 2005 and the present; today it is around 60. A key question is whether the current rate of growth in commodity prices, especially silver and gold, can be sustained and for how long.

The collapse of 2026 is a warning signal, says Laurian Lungu. It remains to be seen whether regulators will act before an exchange faces an actual delivery failure, whether they will wait for the system to reach a critical point to impose emergency rules, as happened in the 1980s, or whether the markets will correct themselves without further major convulsions. Time will decide, the Romanian economist says at the end of his analysis.