Bank Pekao was the first in Poland to introduce a product based on a new reference rate, i.e. POLSTR (Polish Short Term Rate), which will soon replace WIBOR as a result of the reform of reference indices carried out over the last few years.

The new product of Bank Pekao is addressed to companies from the SME and corporate segments. The overdraft facility has a variable interest rate, which is based on the POLSTR 1M Folded Rate (an index built on the basis of the POLSTR rates from the last month) and increased by the bank's margin. Pekao argues that daily updated interest rates accurately reflect market conditions and increase the predictability of financing costs. The loan, which enables financing the current operations of companies, is available in PLN for a period of up to 12 months.

— Our main goal is to offer innovative products supporting company liquidity management, but an equally important issue is to build trust in the new architecture of the financial market, says Dominika Byrska, director of the Credit Products and Processes Department at Bank Pekao.

The first issue of treasury bonds with the POLSTR index is coming soon

The introduction of POLSTR is aimed at adapting the Polish market to EU regulations regarding benchmarks and developing modern financial standards. However, the course of the reform of benchmarks in Poland was turbulent and accelerated for political reasons.

Initially, the Steering Committee of the National Working Group for the Reform of Reference Indicators (KS NGR) chose the WIRON index as the successor to WIBOR. However, it turned out that there were problems with this indicator, including: too much variability and deviation from the NBP rates. POLSTR (initially called WIRF-) was selected as the successor to WIBOR in December 2024.

The symbolic lack of confidence in the initially proposed WIRON index was that, despite the announcements, the Ministry of Finance never decided to issue treasury bonds based on this index (even though some banks, such as Pekao or ING Bank Śląski, had already introduced loans with this index to their offer). Now the situation is better – any day now we will have a debut debt auction, during which the Ministry of Finance will sell a new series of treasury bonds (NZ0928) based on the POLSTR index. This plan was confirmed a few days ago by Deputy Minister of Finance Jurand Drop. In November, the Ministry of Finance is planning two auctions: on November 21 (PLN 5-10 billion) and on November 26 (PLN 6-12 billion).

Banks are moving along the roadmap towards the POLSTR index

We asked leading Polish banks when they would introduce products based on the POLSTR index to their offer. It's mainly about loans, especially mortgages. All banks refer us to the so-called roadmap, i.e. the schedule developed by the National Working Group on the reform of benchmarks.

|

GPW Benchmark, own study

— We operate in accordance with the road map adopted by NGR. It is worth noting that according to her, the offer of loans by banks to customers is preceded by the development of the State Treasury bond market and the wholesale market of derivatives based on POLSTR – says Paweł Bednarz, spokesman for Alior Bank.

This means that after the debut issue of treasury securities with the POLSTR index, an important condition will be met. The road map, updated in April this year, stipulates that short-term credit products and cash management for companies should be introduced from the first quarter of 2026, and other credit products will be offered from the second quarter of 2026.

— Taking into account when the development of the WIBOR index is to end, which will happen at the end of 2027, large-scale loans with the POLSTR index will probably start in the first half of 2026. There is no point in offering loans based on the WIBOR index, since it will soon cease to be published and the successor is ready, says one of the bankers, speaking on condition of anonymity.

PKO Bank Polski announced that it plans to first start offering selected products based on reference indicators from the POLSTR indicator family to institutional clients. Santander Bank Polska replied that it was at an advanced stage of analytical work. “According to the Road Map, we will make products available on POLSTR by the end of next year,” it added.

Bank Pekao informed us that analyzes the introduction of subsequent banking products based on the new POLSTR interest rate reference index. “We will keep you updated on planned implementations, in accordance with the deadlines specified in the Road Map,” added the bank's representatives.

— We have not yet decided when we will implement products based on the POLSTR index – both for individual and corporate clients. We will definitely do it to comply with the requirements, says Piotr Skoczek, director of the Credit Product Management Department at Credit Agricole Bank Polska.

The rest of the article is below the video

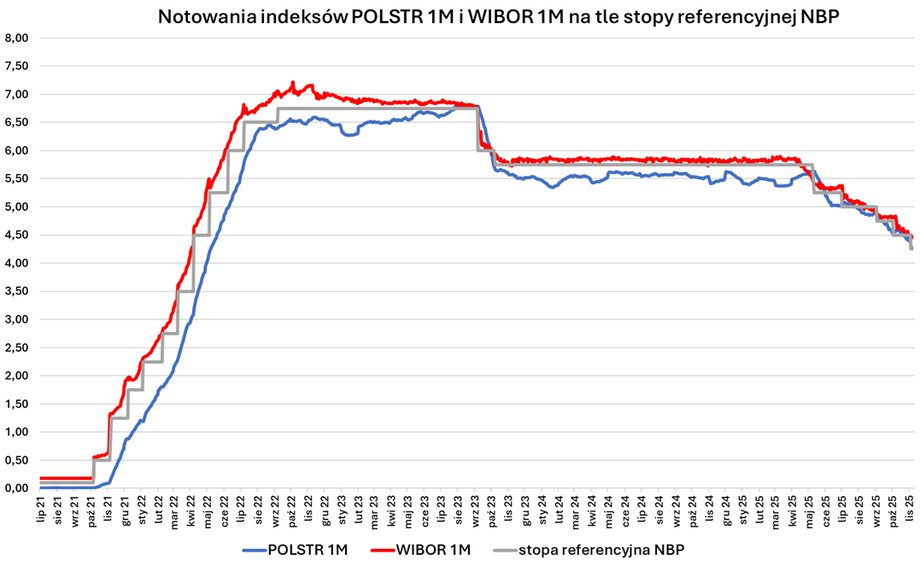

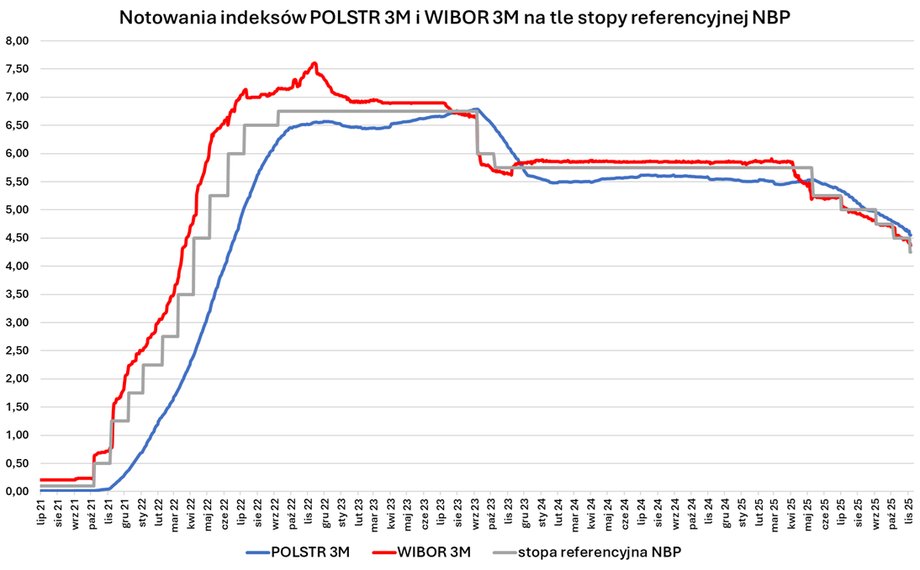

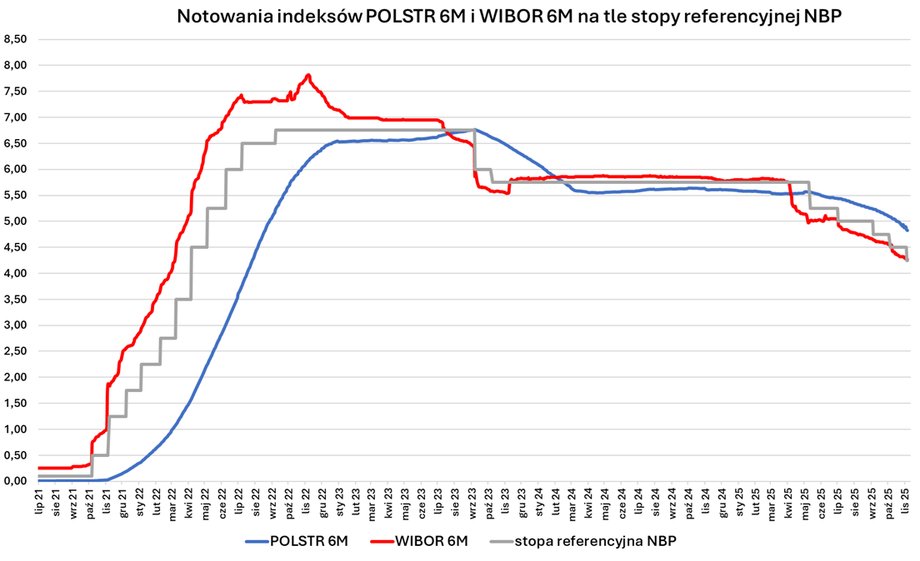

For now, the “folded” POLSTR indices are higher than the WIBOR equivalents

From the perspective of bank customers, it is interesting whether the interest rates on new loans with the POLSTR index will differ from the existing ones based on the WIBOR rate. And although in times of stable NBP interest rates and with expectations of continued stability, the new rate is usually slightly lower than the current one, it seems that there is no reason to expect that new loans will be cheaper for consumers.

For example, POLSTR 1M was about 0.3 percentage points during stable rates between autumn 2023 and spring 2025. than WIBOR 1M and averaged approximately 5.5%. We emphasize that when comparing both indices, it is worth choosing a period of stable rates: WIBOR “looks into the future” (takes into account the expected cost of money on the interbank market), while POLSTR “looks into the past” (it includes rates from recent months). During the period of rising rates, WIBOR grows slightly faster than POLSTR. During a decline, the new rate takes into account NBP rate cuts later than WIBOR, which “anticipates” them. In this text, we describe in detail the calculation method and key features of the POLSTR index.

|

GPW Benchmark, own study

Currently, WIBOR in the monthly version is approximately 4.47%, and its equivalent POLSTR is lower by approximately 0.2 percentage points. But in the case of the three-month POLSTR rate, it is 4.55 percent. and is higher than WIBOR by 0.18 percentage points. The new six-month rate is now 4.83 percent, which means it is 0.57 percentage point higher than WIBOR.

The lower readings of the WIBOR indices than the POLSTR in the 3M and 6M varieties demonstrate the above-mentioned feature of the new index: it “looks into the past”, so it reacts “with a delay” to reductions in official interest rates.

Can you count on lower interest rates on loans from POLSTR?

What does all this mean in practice? Let us repeat – assuming stable NBP rates and no further cuts, i.e. in conditions when POLSTR should be slightly lower than WIBOR, can bank customers count on lower interest rates on new loans?

Bartosz Turek, a financial and housing market analyst, does not expect such an effect. — The reason is simple: banks make money on the difference between the interest rates on loans and deposits. In order to offer cheaper loans, first of all, the cost of obtaining capital used to grant these loans must decrease.. Simply put, for loans to become cheaper, deposit rates must fall. Just replacing WIBOR with POLSTR does not change anything in this respect. To reduce interest rates, we need interest rate cuts, a decrease in the risk of granting loans and greater competition between banks, the expert emphasizes.

|

GPW Benchmark, own study

There is no sign of a decrease in risk, as there are attempts to question not only smaller consumer loans (cases regarding the so-called free loan sanction, SKD), but also housing loans due to the WIBOR rate and information requirements in this area. In addition, banks have to issue a lot of financial instruments due to regulations such as the Long-Term Funding Index (WFD) or MREL, which costs them a lot. On the other hand, the potential to reduce the margin could be increased by a further increase in record excess liquidity (predominance of deposits over loans), but a gradual credit recovery and slowing down of the growth rate of deposits will reduce the excess liquidity.

— Theoretically, a cosmetic difference in interest rates may occur if banks offered mortgages based on POLSTR 1M. Then, on the borrower's side, there would be greater monthly variability of the interest rate than in the case of a loan in which the installment changes every three or six months, as with WIBOR 3M and WIBOR 6M. This means a slightly higher risk on the client's side. As a result, in a period of stable rates, this may mean a slightly lower interest rate, but the difference would be cosmetic at best, and the price for it would be more frequent installment variability. At least in theory, says Bartosz Turek.

Existing wallet and conversion to POLSTR. There will be a corrective spread

What about previously granted loans with variable interest rates based on WIBOR indicators? Here, the WIBOR index will be replaced by the POLSTR index in the contracts. In the case of loans with the so-called emergency plan (also known as the so-called fallback clause), the matter is simple. However, many older contracts do not have such provisions. In such loans – apart from legislative doubts that appear in the public space – the rate will also change to a new one based on the appropriate legal act.

One more move will be necessary, i.e. the introduction of the so-called corrective spread. This is an element that will equalize the loan interest rate after changing the indicator to POLSTR so as to maintain the economic neutrality of the reform. Therefore, the installments of already repaid loans will not change or the changes will be minimal. We write more about this here.

Polish banks are already sending letters to their clients on this matter. The correspondence concerns housing loans in PLN. First of all, those whose interest rates are variable and based on the WIBOR rate, where there are no emergency plans. Banks suggest signing an annex to the contract.

What is the POLSTR index?

Let us recall that POLSTR is an interest rate index that is close to the risk-free rate, i.e. the so-called Risk Free Rate. The development of RFR indices means that the purpose of the index is to reflect the interest rate measured with the assumption of limiting market risk, including the risk of market expectations as to the development of rates in the future, as well as liquidity risk or credit risk. Providing RFR-type indices and switching from IBOR-type indices to indices that do not take into account these risk factors is part of a global trend (a similar reform to ours was recently carried out, e.g. in Switzerland).

POLSTR presents the average interest rate weighted by the volume of deposit transactions in PLN concluded at O/N maturity on the wholesale money market. According to the results of NGR's work to date, the choice of POLSTR means that the target of measurement is the wholesale money market, defined as the market for unsecured deposits made by credit institutions and financial institutions. Unlike WIRON, which was originally intended to be the successor to WIBOR, it does not take into account the corporate deposit market.

Author: Maciej Rudke, journalist of Business Insider Polska