PPK, OFE, IKE, IKZE after the turmoil. We checked what happened to the savings

The stock market declines in the first weeks of March caused by the war in the Middle East caused Poles' retirement savings to shrink by several percent. At first glance, the amounts were impressive, as they were talking about billions of zlotys, but experts were reassuring. Verification came quickly.

— The current turmoil does not call into question the wisdom of long-term retirement savings – emphasized Małgorzata Rusewicz, president of the Chamber of Commerce of Pension Companies (IGTE) and the Chamber of Fund and Asset Managers (IZFiA) in an interview with Business Insider.

Read also in BUSINESS INSIDER

— It must be remembered that funds in PPK, OFE, IKE or IKZE are invested in different asset classes and on different markets, so short-term fluctuations in their value are natural – she explained.

History shows that after large market shocks (e.g. during the COVID-19 pandemic), markets reacted sharply but stabilized over time. The pace of making up for losses varied – from a few days to several months. In the last crisis, in most cases two weeks were enough to erase all losses.

Pension savings in OFE

At the end of March 2026, according to ZUS data, the number of members of Open Pension Funds (OFE) was exactly 13 million 887 thousand. 875. This group includes both people who make monthly contributions from their salary and those who have stopped doing so, but OFEs continue to use their money, which will be paid out after reaching retirement age. We are talking about a considerable sum of over PLN 303 billion.

Currently, eight entities manage the money of future retirees accumulated in OFE. Nationale-Nederlanden OFE has the highest share unit value and the largest assets (approx. PLN 84 billion). The value of its share unit (baseline unit of performance measurement) between February 27 (the day before the US and Israel attacked Iran) and March 23 (the trough of performance) decreased by 6%. To put it simply, we can say that this is how much pension savings have shrunk in connection with the conflict in the Middle East.

See also: Polish retirees are rich, but only on paper. How long will the savings last?

Is that a lot or a little? In three weeks, the entire surplus previously generated for almost two months evaporated. It was though a small percentage of previous increases (from the end of February 2025 to the end of February 2026, the valuation in Nationale-Nederlanden OFE increased by approximately 35%).

|

Created using AI/ChatGPT

It took only two weeks to make up for the “war” losses. Already on April 8, 2026, NN OFE quotations were higher than on February 27. Then they went up even more (peaking in mid-April), then retreated slightly again, but the balance is positive.

The scale of losses from the beginning of the conflict in the Middle East and subsequent profits are well illustrated by the charts below of the value of a participation unit in NN OFE.

NN OFE quotations over the last 12 months

|

Analysis.pl

NN OFE quotations after the attack on Iran

|

Analysis.pl

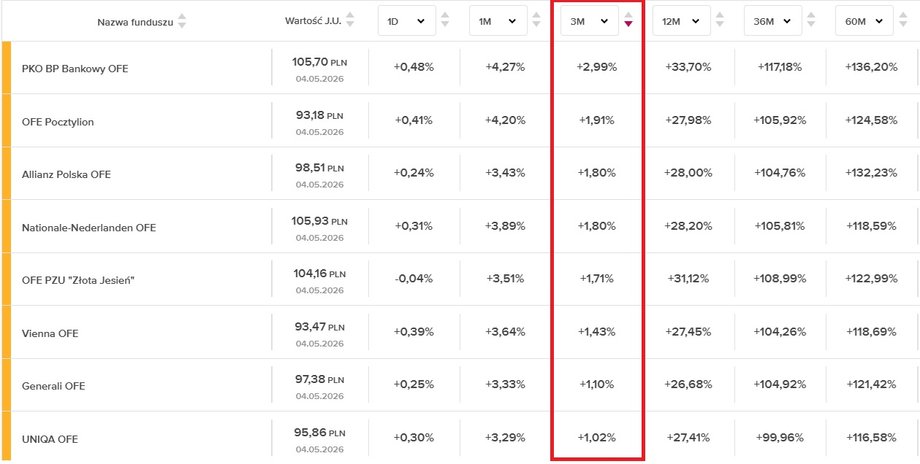

The charts and rates of return look very similar in the case of the seven remaining OFEs.

OFE rates of return in various periods (valuation increases in the last three months marked in red)

|

Analysis.pl

Pension savings in PPK

The analysis of PPK results is slightly more complicated. There, retirement savings are managed by several institutions that in total operate approximately 160 different funds with different strategies depending on the age of the savers.

Recall that there were 5.31 million active accounts in Employee Capital Plans (PPK) at the end of March 2026on which it gathered almost PLN 47 billionand PFR, responsible for managing the program, indicates that 4.28 million people have already taken advantage of the opportunities offered by PPK.

See also: Here is the average pension in the uniformed service. There is something to envy

We took a closer look at extreme solutions, i.e. funds supporting PPK, which had the lowest and highest rates of return in recent months.. It turns out that, similarly to OFE, the leaders had already made up for their losses by April 8, and after that time the savers were in the black. In turn, the most aggressive strategies (less than half) were still in decline at the same time, but only to a small extent (maximum 2.5%).

Esaliens 2060 quotes after the attack on Iran

|

Analysis.pl

Goldman Sachs quotations Pension 2025 after the attack on Iran

|

Analysis.pl

The results of IKE and IKZE depend on the chosen form of investment

At the end of 2025, it was almost there 770 thousand Individual Pension Security Accounts (IKZE)which included over PLN 18 billion and close 1.2 million Individual Retirement Accounts (IKE)which in mid-2025 was PLN 27 billion.

Unlike OFE and PPK, which are managed by specially designated investment funds, it is more difficult to show the impact of market turmoil on IKE and IKZE. Both entities are merely tax “wrappers” that may hide very different investments.

Is a large variety of forms of investing savings in IKE/IKZE. It may be a bank deposit, a brokerage account, a life insurance policy or a portfolio of investment funds. In the case of IKE/IKZE in the form of a brokerage account, the results depend on the specific shares or bonds that a specific person purchases. There is no single “IKE/IKZE quotation” that can be checked.

See also: ZUS loses in the courts. Mr. Andrzej received 18,000. PLN and PLN 800 towards retirement

There is no doubt that the money invested in treasury bonds alone could only grow in recent weeks. Similarly with bank deposits. Overall, stock markets have been doing well lately, so only unlucky choices of specific companies from the WSE or other exchanges may continue to weigh more heavily on retirement savings.

— In the face of limited predictability in the world, the most reasonable and effective investment principle remains consistent, regular saving over a long period of time and appropriate diversification, e.g. by using various savings instruments with different risk profiles. This is why Savers should not panic in times of crisis, but remember that the greatest damage to pension products is usually not caused by the declines themselves, but by the emotional decisions made during them. – emphasizes Małgorzata Rusewicz, head of IGTE and IZFiA.

Note: the information contained in the text is for informational purposes only and does not constitute an investment recommendation, information recommending or suggesting an investment strategy within the meaning of applicable regulations, or any other form of advice regarding the purchase or sale of financial products.

Author: Damian Słomski, journalist of Business Insider Polska