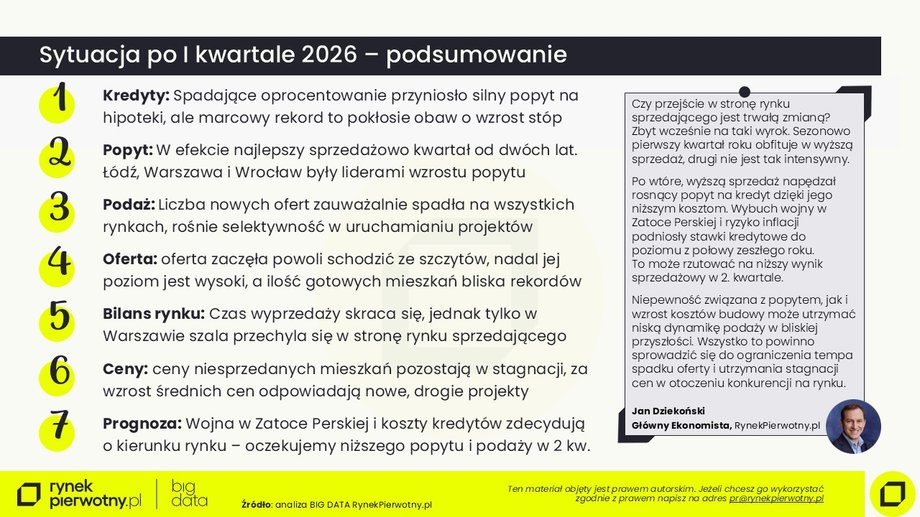

The first quarter of 2026 brought results on the development apartment market that seemed unrealistic just a few months ago. Sales were record high, credit demand exploded, and the supply began to shrink. At the same time, however, they appear in the background warning signs: rising financing costs, geopolitical uncertainty and developer caution. Experts indicate that this may be a breakthrough moment – after a period of rebound, the market may enter a slowdown phase.

Read also: The most expensive hotels in Poland. Luxury, unique apartments and experiences

Mortgage loans: the impulse fueled the purchasing boom

The mortgage market was one of the main drivers of growth in Q1 2026. The previously falling interest rates on loans quickly translated into an increase in interest in financing the purchase of apartments. Already in January and February, a clear recovery was visible March brought a record number of people submitting loan applications compared to the last 18 years.

The situation on the housing market

The situation on the housing market

See also: Are apartment prices rising because of flippers? “We are rather an element that organizes the market”

As RynekPierwotny.pl experts emphasize, it was the effect of both earlier stimulation of the market and acceleration of purchasing decisions. Customers, fearing an increase in loan costs, decided not to finalize transactions faster. They also played an important role refinancing companies, who could be responsible for up to 40-50 percent. demand for mortgages. As a result, the number of applications increased by 27%. compared to Q4 2025

The borrowers' fears turned out to be justified. In March, the interest rate on periodically fixed rate loans increased, accounting for approximately 65-75 percent. market. A jump of approximately 70 bp. means a return to the levels from a year ago. The “accumulation of credit demand” may therefore be short-lived — as creditworthiness decreases, interest in financing may weaken in the following months.

Housing market

Read: A higher tax bracket? There's so much to gain [KWOTY]

Apartment sales are breaking records, but supply cannot keep up

The effect of cheaper loans was immediate – apartment sales in the seven largest markets reached 14.8 thousand. premises, which means an increase of 19%. year to year and by 17 percent quarter to quarter. This is the best result in two years.

The highest growth dynamics was recorded in Łódź, Warsaw and Wrocławwhere sales were over 20 percent. higher than the average from 2025. Importantly, customers were eager to buy completed apartments – often covered by attractive discounts. At the same time, there was a growing interest in high-end premises, especially those above PLN 1 million.

On the supply side, however, the situation is completely different. Developers have clearly reduced the pace of introducing new investments. In most large cities, the number of new offers was lower than the 2025 average. Kraków remains an exception.

There are several reasons: a high level of the available offer, a large share of ready, unsold apartments (26% of the market) and growing economic uncertainty. Additionally developers face cost pressure and risk related to the geopolitical situation.

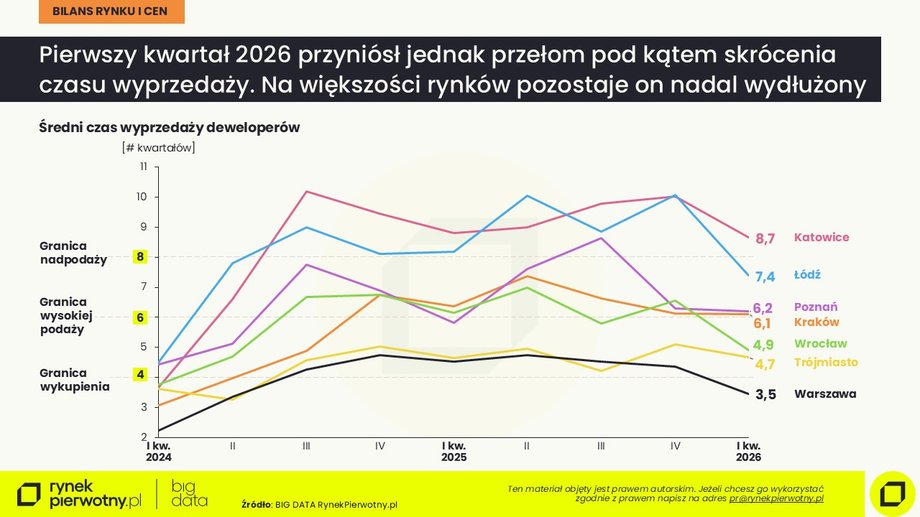

As Jan Dziekoński, chief economist at RynekPierwotny.pl, notes, “Warsaw is a forerunner and responds fastest to good economic conditions — we already have a seller's market there. In the capital, the sale time has dropped below four quarters, which means that sellers have an advantage. In other cities, however, the offer remains relatively high.

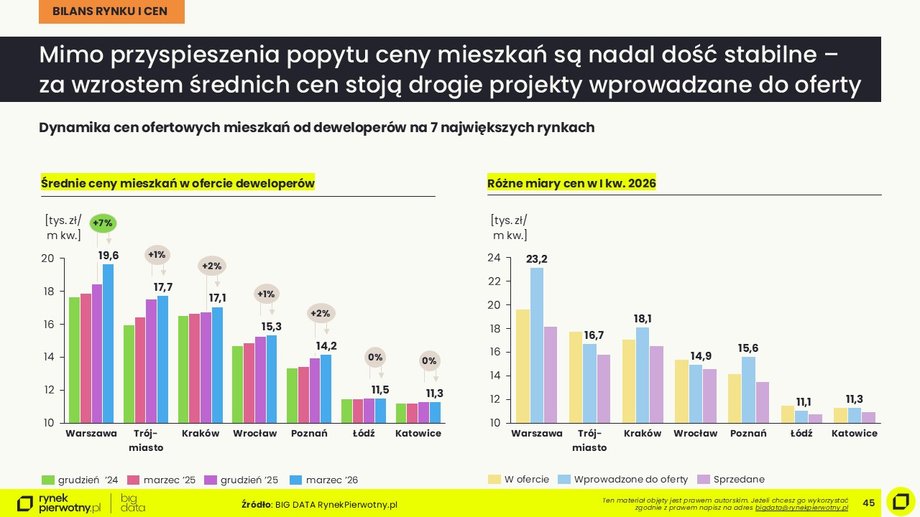

Apartment prices are stagnant… but this is an illusion

Despite strong demand and shrinking supply, housing prices in most cities remain stable. In the first quarter of 2026, only cosmetic increases of 1-2% were recorded. or stagnation.

There is a clear exception Warsaw, where the average price per square meter increased by 7%. within three months. As experts emphasize, this is not due to increases in existing investments, but to… introducing new, more expensive projects.

– Unsold apartments keep prices unchanged, and if they remain on offer, it leads to greater price aggression and discounts – points out Gabriela Prygiel from RynekPierwotny.pl.

Marek Wielgo also draws attention to the problem. In his opinion the average price says less and less about the real availability of apartments. — First of all, the cheapest premises disappear from the marketand in their place more and more expensive investments appear. It is this mechanism that drives up average prices, he explains.

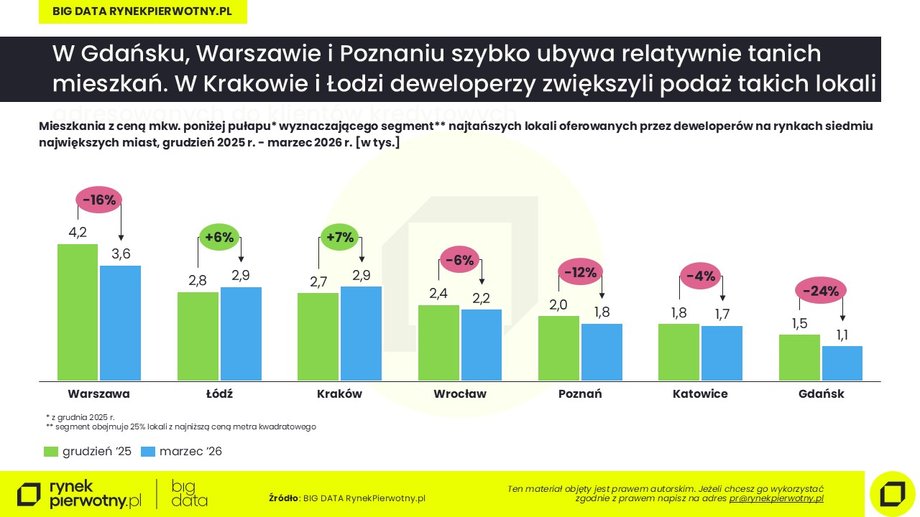

The examples are clear. In Gdańsk, the number of the cheapest apartments dropped by almost a quarter in three months, and the price threshold of this segment increased by almost 7%. We observe similar phenomena in Warsaw and Poznań. This means that people with limited creditworthiness have less and less opportunities to purchase.

Offer on the market

Offer on the market

Worth reading: CJEU on the limitation period for banks' claims. What does this mean for Swiss franc borrowers?

The second quarter of the housing market is marked by uncertainty

Experts agree: Q2 2026 will probably bring a cooling of the market. Demand will still be relatively high, but lower than at the beginning of the year. Some of the transactions will still be the result of “unloading” the record number of loan applications from the first quarter, but there may be fewer new customers.

Housing market

Read also: It was a month of surprises on the stock exchange. Here's what's next for bonds and stocks [ANALIZA]

The reason is increase in loan costs and deteriorating creditworthiness. Additionally the market is influenced by the geopolitical situation, including the conflict in the Persian Gulf, which drives up oil prices and increases the inflation risk.

On the supply side, it is expected further decline in new investments. Developers remain cautious, and the high share of completed apartments limits the pressure to launch new projects.

As a result the offer may gradually shrink, although the number of unsold, ready units will continue to grow. This, in turn, will maintain competitive pressure and limit the potential for price increases.

Price forecasts remain moderate — stagnation or growth close to inflation is expected in most markets. The exception may be locations with limited supply, such as Warsaw or Gdańsk, where point increases are possible.

As Jan Dziekoński summarizes, the current situation is different from that of 2022 – the market is entering a period of uncertainty after a phase of growth, not decline. This means that any economic downturn may be milder, although it is still difficult to predict clearly.