The end of the fat years of banks. The change in conditions set their profits back by three years

The net profit of the banking sector after two months of 2026 amounted to less than PLN 6.1 billion, i.e. it decreased significantly by 25%. year to year – according to the latest data from the National Bank of Poland. This is also 17 percent. less than in the same period of 2024 and 1 percent less than in 2023

In February alone, net profit fell by 27%. year to year and 3 percent on a monthly basis. These results may suggest that a major earnings decline is coming after the record profits of 2024-2025, but this may not necessarily be an accurate diagnosis.

To check this, you need to look at the structure of the results. Firstly, the new operating conditions of banks must be taken into account. Although the economic situation is still good – GDP is growing, the labor market is still strong, and interest rates remain elevated despite the declines – but these tax regulations have changed significantly.

Higher tax already reduces bank profits

This is about the increase in the CIT rate, which came into effect at the beginning of this year: from January, the tax rate for banks increased to 30%. In the following years, it is expected to gradually decrease to 26%. in 2027 and 23 percent in 2028, but it will still be significantly higher than 19%. applicable before the increase. The effects can be seen in the effective tax rate (tax in relation to gross profit), which after two months of 2026 is approximately 39%. compared to 25 percent a year ago. The government estimated that in the first year the CIT increase for lenders would provide the state budget with an additional PLN 6.5 billion.

Before we move on to the second key factor after tax, i.e. interest income, let's take a look at other elements of the banks' income statement. Total operating revenues decreased slightly by 0.3%. year to year and amounted to over PLN 22.9 billion, and at the same time administrative costs increased by 8.5%, to PLN 11.1 billion. This is bad news for banks because it means a deterioration in operational efficiency.

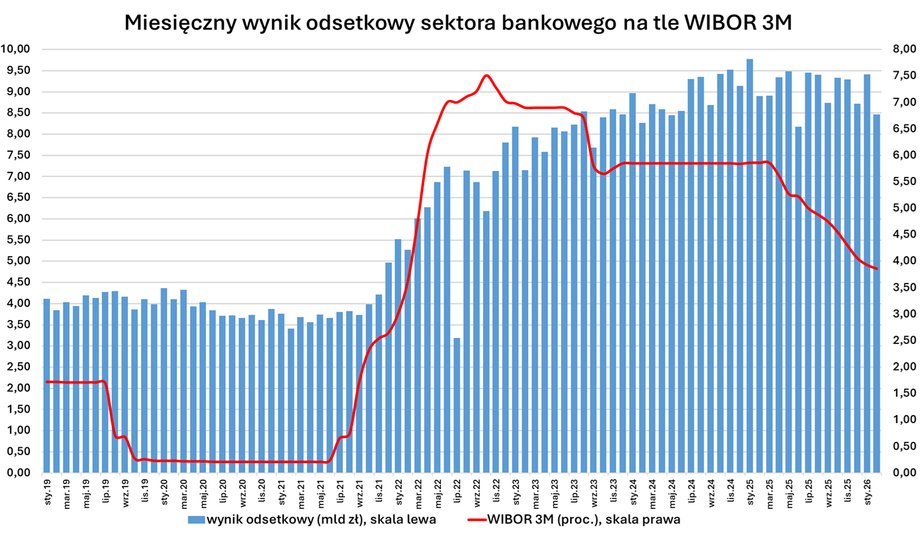

The beginning of 2026 for banks was already weaker in terms of net profit. Not only compared to 2025, but also compared to previous years.

|

NBP, own study

The increase in operating costs is mainly the result of salary increases for employees and an increase in general administrative expenses. The contribution to the Bank Guarantee Fund is almost identical to last year and will amount to PLN 2.73 billion, but the structure is different. The entire amount is a contribution to resolution fundand this is important because it is fully booked in the first quarter, unlike the contribution for deposit guarantee fundwhich is divided equally into four quarters. In 2025, PLN 1.81 billion was paid to the restructuring fund, and PLN 0.89 billion was paid to the deposit guarantee, so this year the burden on the first quarter results is greater. Analysts estimate that if the sector's net result after February were adjusted for the effect of the BFG contribution this year, the net result would decline by 17%. instead of the reported 25 percent.

See also: The attack on Iran affects Polish treasury bonds. Banks have a dilemma

At the same time, loan repayment is good (parameters such as the cost of credit risk and the share of receivables with delayed payment are at the best levels in history). The balance of loan provisions after two months amounted to over PLN 670 million. This is true by 16 percent. more than a year ago, but the impact on the nominal result is small (about PLN 100 million).

Interest income under the microscope

Interest income is crucial for banks, it now accounts for 78%. their income. This is the difference between interest income and interest expense. This result is mainly influenced by the interest rates on loans, but also on bonds (they have a large share in the sector's assets), and on the other hand, the rates that banks pay to depositors and bondholders (interest costs) are of great importance.

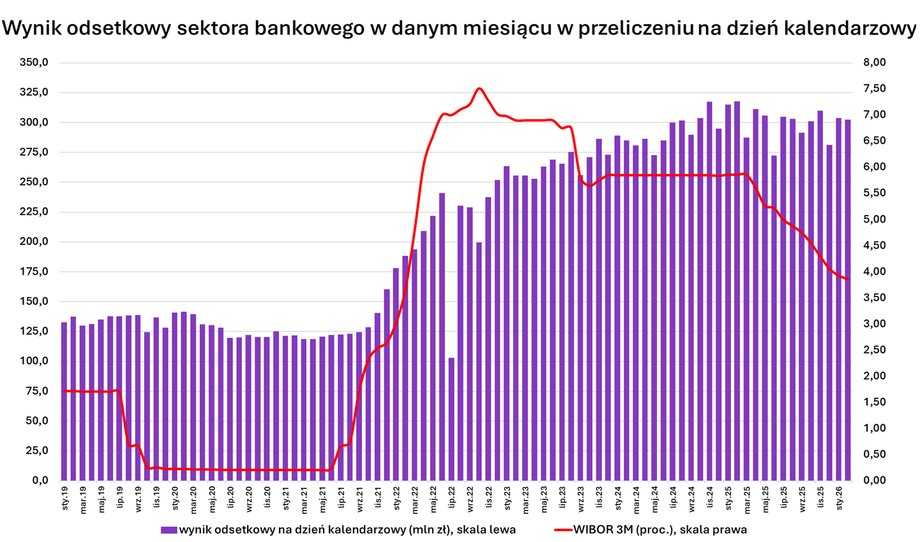

The numbers don't lie and the interest income has deteriorated: after two months of 2026, interest income amounted to PLN 17.9 billion, which means a decrease of 4.2%. year to year. Most likely, the industry has already passed its peak in terms of this result (in 2025, thanks to high interest rates, it managed to generate PLN 109.5 billion).

The decrease in interest income in July 2022 visible in the chart is the result of the settlement of credit holidays. This result is highly dependent on interest rates and changes in the value of bank assets.

|

NBP, own study

One of the most important factors for interest income is the level of interest rates: mainly WIBOR (the interest rate on variable rate loans is based on them) and the NBP reference rate (the interest rate on NBP money bills that banks buy, investing surplus liquidity in them). WIBOR 3M rates in February 2026 dropped to approximately 3.85 percent, i.e. by 2 percentage points. lower than a year earlier, and the reference rate at that time decreased by 1.75 percentage points, to 4%. (in March there was another cut of 0.25 percentage points). Interest income is also influenced by whether the assets (loans and treasury bonds) of banks are growing. It is worth recalling that in recent years the so-called volumes have increased significantly and this trend continues.

See also: “Banks will have no scruples.” This is how rate cuts will affect their results

Also in February itself, a deterioration of the interest income is visible: compared to January, by 10%, to PLN 8.47 billion (the lowest level since December 2024), and year-on-year by 5%.. Taking into account the significant drop in rates, the deterioration of the result in February should not be surprising. However, this is not the full picture because a different number of calendar days must be taken into account. In February it is lower than in January, and the difference between 31 days and 28 days is important. After such a correction, the February result was only slightly (0.4%) worse than in January. On an annual basis, it fell by almost 5%, so it is still highly resistant to a significant drop in interest rates.

Banks are trying to defend their interest income

— A factor supporting the interest income is the increase in volumes: loans and deposits grow by approximately 7%. year to year. Moreover, the sensitivity of Polish banks to changes in rates is lower than in the past, among others. thanks to a greater share of fixed-rate loans and hedging transactions – says Łukasz Jańczak, analyst at Erste Securities.

Marcin Materna, director of the analysis department at BM Bank Millennium, has a similar diagnosis. — The large share of bonds in the portfolio limits the short-term impact of a drop in interest rates on results. Additionally, banks do not compete when it comes to deposit rates, and part of the loan portfolio is based on fixed rates or hedged, the expert notes. More government bonds with higher interest rates also help.

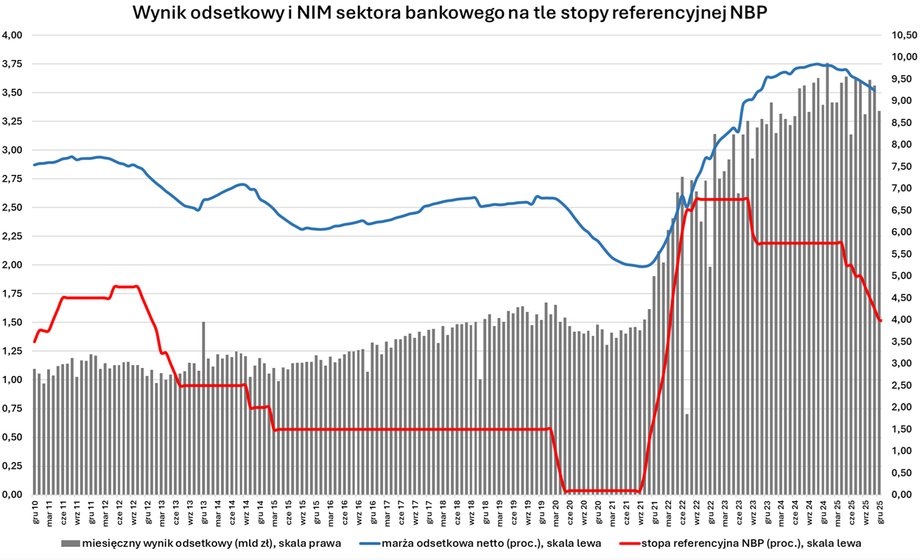

Calculated per calendar day, the interest income of the banking sector – despite the decline in interest rates – remains relatively high.

|

NBP, own study

To isolate the impact of changes in volumes, it is worth tracking net interest margin (NIM). It is the ratio of the interest income for the last 12 months to the average interest-bearing assets during this period. Our estimates show that the peak of NIM occurred at the end of 2024, when this indicator in the Polish banking sector reached 3.75%. At the end of January 2026, it was approximately 3.46 percent, i.e. 0.27 percentage point. less than a year ago.

See also: All-time banking record. Will billions in profits survive rate cuts and higher taxes?

— NIM is decreasing and I expect that, assuming stable interest rates, it will drop further by the end of the year, because it takes time for lower WIBOR rates to translate into lower loan interest rates. Banks reduced financing costs to defend margins and interest income, and although there is still room for optimization in this respect, it is rather small and the biggest move in terms of cutting deposit interest rates has already been made. The receding prospect of interest rate cuts means that NIM will probably not fall this year as expected when continuation of cuts was assumed, says Łukasz Jańczak.

He explains that in order to protect the margin and interest income, hedging works in such a way that its negative impact has been decreasing in recent quarters and will continue to decrease (we wrote about the impact of hedging on banks' results, among others, in this text). — At some point, the hedging result may even turn out to be positive, because over time the oldest transactions of this type, concluded at lower interest rates, expire. Banks have taken advantage of high interest rates in recent years to enter into new hedging at higher rates, so they should be well protected against falling costs of money in the next few years.

Banks' net interest margin (NIM) has been falling for several months due to interest rate cuts.

|

NBP, own study

So what's next for interest income? — However, I would expect this result to decline – lower rates will sooner or later be more reflected in the result from this item. I do not expect a large increase in lending, and if there is, it will concern segments with low margins, such as loans for large infrastructure investments for which every bank is “fighting” – says Marcin Materna.

Author: Maciej Rudke, journalist of Business Insider Polska