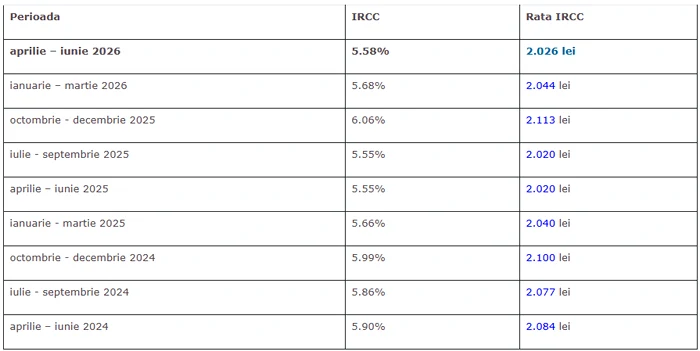

The reference index for consumer loans (IRCC) decreased to 5.58% (from 5.68%), which brings good news for Romanians with loans in lei with variable interest. The new value will lead to lower monthly rates for those who have loans calculated according to this index.

Rates come down a bit thanks to IRCC. Photo by Shutterstock

The decrease in IRCC reflects recent developments in the interbank market and a slight easing of funding costs. For borrowers, this translates directly into monthly savings, although the differences may vary depending on the loan amount and the bank's margin.

For example, for an average mortgage loan, reducing the index can mean a decrease in the rate by several tens of lei per month. Although the impact is not spectacular, it is a step in the right direction, especially after periods of successive interest rate hikes.

Computational simulation

Compared to March, the rate decreased by 18 lei. Compared to the same period last year, the monthly rate is 6 lei higher, but remains 58 lei lower than the 2024 level.

Finzoom specialists recommend that people with variable loans carefully follow the evolution of IRCC and consider options such as refinancing or switching to fixed interest, depending on the economic context and personal plans.

Calculation simulation: 250,000 lei / 30 years. Interest: IRCC + 3.5%

Rates are falling, but too slowly

Specialists point out that, although the direction is positive, the rate of decline is too slow to significantly reduce the financial pressure accumulated in recent years. However, there are signs that IRCC will continue to decline slightly in the third quarter as well, which could bring a gradual stabilization of credit costs.

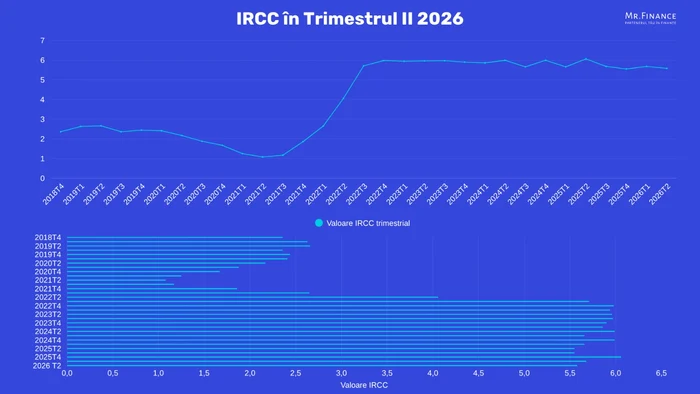

Since Q1 2023, IRCC has seen little fluctuation, staying in a relatively stable range with a low of around 5.55% and a high of just over 6%. This evolution is closely related to the high level of inflation in Romania in recent years, says Ion Soltinschi, Mr.Finance consultant. According to him, in order to control the increase in prices, the NBR had to increase the monetary policy interest rate, which directly influenced the cost of interbank loans and, implicitly, the IRCC.

The credit market in 2026, from turbulence to calculated decisions. How was 2025

The economic and geopolitical context also played an important role. Events such as the war in Ukraine, internal political tensions or conflicts in the Middle East have contributed to increased uncertainty and the increase in the price of resources, especially fuel. These developments fueled a new wave of inflation, felt especially in food and energy prices.

Even though estimates point to a slight decrease in IRCC to around 5.55% in the third quarter of 2026, experts caution that we should not expect significant rate cuts in the immediate period ahead. The process of falling inflation is slow and influenced by many external factors, which makes a quick return to lower borrowing costs difficult.

IRCC the main reference index for loans in lei with variable interest

IRCC remains the main reference index for loans in lei with variable interest granted after May 2019. It represents the average interest rates at which banks lend to each other and has an important feature: it is applied with a lag of one quarter. Thus, the values calculated in one period are reflected in the actual costs of credits only in the following quarter, which delays the effects felt by consumers.

In terms of the concrete impact on rates, the differences are minor. For example, for a mortgage loan of approximately 70,000 euros (the equivalent of approximately 350,000 lei), contracted for 30 years, the current monthly rate is around 2,612 lei. With the decrease of IRCC to 5.58%, the rate would drop to approximately 2,587 lei. If the index reaches 5.55% in the third quarter, the rate would decrease slightly, to around 2,580 lei. The differences are, therefore, of the order of tens of lei, which confirms that the impact is reduced.

In this context, those who have variable interest loans should carefully analyze the available options. One of the most frequent recommendations of specialists is to refinance to a fixed interest rate, especially since some banks still offer favorable conditions, with interest rates starting at around 4.59%. Also, early repayments can significantly reduce the total cost of the loan, and for those who can, early closing the loan remains the most effective long-term solution.

It is interesting that, recently, several banks have come up with fixed interest offers below the current level of IRCC, which is considered atypical for the banking market. This allowed many Romanians to reduce their risk associated with interest rate fluctuations by refinancing.

Banks with the best interest rates on mortgage loans

In an attempt to attract new customers, many banks have mortgage offers with a fixed interest rate of 4.59%. These can be good options for refinancing if we have variable interest rates that have increased a lot in recent years.

The best mortgage loan offers at the moment are:

- UniCredit has among the most competitive interest rates on the market. For the purchase of a home with energy class A or the refinancing of a loan accessed for the purchase of a “green” home, UniCredit offers a 4.59% interest rate loan, fixed for the first 2 years.

- And Raiffeisen has an attractive offer for new loans or refinancing loans to access a home. In this case, the interest is 4.7%, fixed for the first 3 years, then variable. Likewise, the home must be “green”, i.e. have energy class A.

- At BCR, things are almost similar, for a new loan or mortgage refinancing, the interest rate is 4.79%, fixed for 3 years. To benefit from this offer, customers must collect the income in a bank account, take out life insurance and the property must have energy class A.