The regulations oblige the government to review the effectiveness of the Employee Capital Plans (PPK). Business Insider has obtained opinions and proposals for possible changes discussed by those who manage several dozen billions of zlotys of Poles' savings.

According to the regulations, by the end of 2026, the government is obliged to review the Act on Employee Capital Plans (PPK)which could result in changes in the operation of the additional savings program for future retirement.

The rest of the article is below the video

PPK is a voluntary long-term savings system in which the employee's private funds are systematically increased by contributions from the employer and subsidies from the state budget. The collected funds constitute the private property of the participant and are invested by financial institutions to provide additional financial support after the end of professional activity.

See also: Pensions will be different in the future. What awaits Poles?

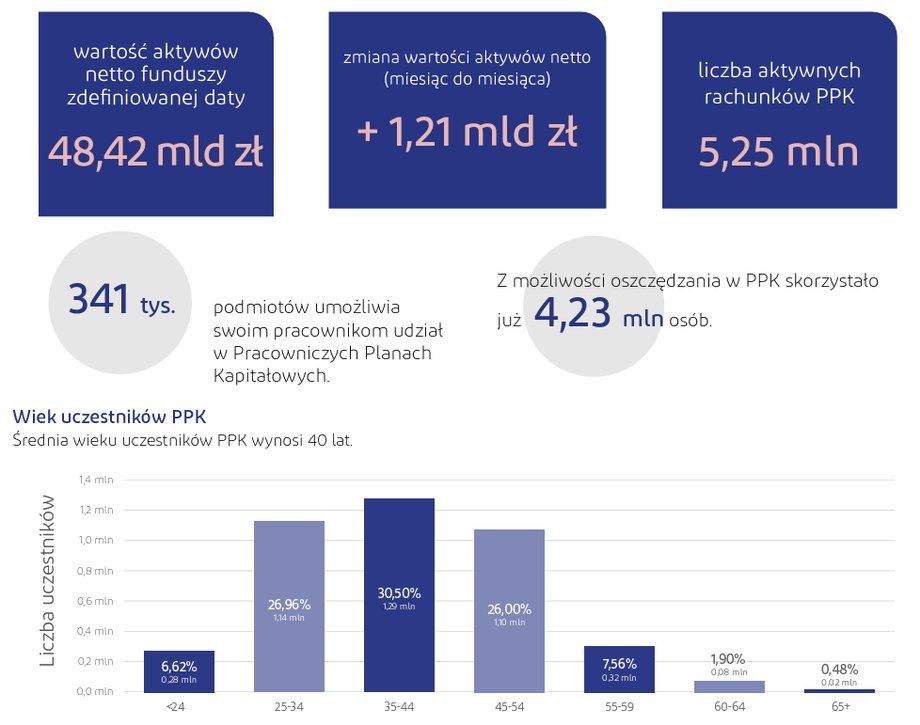

source: Monthly Bulletin of Employee Capital Plans. Data correct as of February 28, 2026.

|

PFR PPK portal

PPK review in 2026. Is it good, or can it be better?

So far, representatives of the Ministry of Finance, the main government stakeholder, have not decided whether any changes to the regulations regarding PPK are necessary, but the discussion is ongoing. Business Insider Polska obtained the content of the document sent to Jurand Drop, Undersecretary of State at the Ministry of Finance, by the Chamber of Commerce of Pension Companies (IGTE – an association of entities managing long-term retirement savings). In it, IGTE assessed the functioning of PPK and presented proposals for solutions that could – as it pointed out – “significantly increase the program's effectiveness for the future“.

In the opinion of IGTE “PPKs have become one of the key elements of the long-term policy of building the financial security of Polish citizens“And thanks to co-financing by the employee, employer and the state, they effectively strengthen the culture of systematic saving and enable the gradual accumulation of private capital.

See also: Finance people tell us how they invest their savings

The universally positive assessment of PPK, which IGTE also joins, does not mean that certain modifications would not allow the program to operate more effectively and become even more popular. For example, the participation rate (59%) still leaves much to be desired.

Below we present six out of nine proposals (the most important from the perspective of savers) for changes to PPKwhich is discussed by the community managing the savings of future retirees.

Changes in PPK? Suggestion: autosave more often

IGTE suggests considering better use of the autosave mechanism through shortening the interval between subsequent such windows from 4 years to 2-3 years.

“In the reality of the Polish labor market, where some employees make decisions under the influence of temporary liquidity pressure, a periodic return to participant status increases the likelihood of maintaining payments in the long term and, consequently, improving the financial situation at the time of retirement,” explains the chamber.

The last auto-enrolment to the program took place in 2023, and in accordance with applicable regulations, the next ones will take place in 2027 and 2031.

See also: The truth about saving extra for retirement is even sadder than it seems

Proposal 2: higher limits on voluntary additional contributions

The second change proposal that would be worth considering is: increasing the limits of voluntary additional contributions of the PPK participant and the employer.

“Increasing the allowable amount of additional contributions – both on the part of the participant and the employer – will translate into a faster increase in the capital accumulated in PPK and, as a result, into a higher level of long-term retirement savings,” says IGTE.

Currently, a PPK participant can declare an additional contribution of up to 2%. remuneration, and his employer may finance an additional payment of up to 2.5%. salary.

More incentives to save in PPK

From the perspective of savers, the structure of PPK is exceptionally advantageous compared to other forms of saving, and there is also an opportunity to withdraw the collected money before reaching retirement age. Unfortunately, this weakens the core function of the program — building private capital for the future.

“In practice, this turns PPK into a tool for current consumption, which reduces both the financial security of participants and the long-term effectiveness of the program on an economic scale. It is therefore justified to introduce additional incentives to stay in the program, which will be clear, simple and noticeable to the participant.” – says IGTE.

As an example recommendation is the introduction of progressive annual payments – treated as a “loyalty bonus”, increasing with the length of time the savings have been maintained in PPK (e.g. higher subsidy after 3, 5, 10 years of continuous participation or in the absence of previous withdrawals).

For example, for participation in PPK in the first three calendar years, the participant could receive an annual payment of PLN 250, hereinafter referred to as the “internship bonus”. After 3 years of regular payments, without a refund of funds from the account, the annual payment could increase, for example, to PLN 400, and after 5 years to PLN 500, etc. Alternatively, an indexation mechanism based on the inflation rate can be used.

What about withdrawals of savings from PPK after retirement?

IGTE proposes a discussion on introducing the possibility of changing the decision regarding the schedule of payment of savings after reaching retirement age.

The current solution locks the participant into the once-selected installment payment option and does not allow either to shorten the payout period or return to a one-time payment.. According to IGTE, this does not fit the realities of life, in which financial and health situations can change rapidly and unpredictably.

What could the change be? If, based on the declared number of installments, the payment of funds is to last at least 10 years, the PPK participant may change the declared number of installments in such a way that all funds remaining on the participant's account will be paid and a flat-rate income tax will be paid on the paid funds..

IGTE emphasizes that, on the one hand, this allows the participant – in justified cases – to complete the installment payment and withdraw the remaining funds once. On the other hand, the mechanism of paying a flat-rate income tax on the funds withdrawn acts as a “safety”, limiting the risk of abuse.

According to the originators, the introduction of the correction option (with clear tax consequences) may work in practice favor more frequent choice of payments spread over timebecause the participant will feel that he or she retains control over his or her savings.

Is a higher cost limit a chance for higher profits?

Among the topics that may be included in the discussion on possible changes to PPK is the issue of the costs of managing the savings of future retirees. They are currently low – the total cost of funds ratio is 0.3%. annually.

“We propose to raise this limit to 0.5%.. We think that This will enable the use of market strategies more focused on sources of potentially higher rates of return, while still ensuring appropriate diversification and an acceptable level of costs. – explains IGTE.

This would mean that PPK savers would incur higher costs, but it would make it possible to make investments that would bring higher profits in the longer term.

See also: Will Bitcoin go to the American equivalent of PPK? Cryptocurrency is gaining enormously

Reducing the costs of operating the portal

IGTE is considering not only increasing the cost limit (as before), but also reducing the operating costs in another area – the portal supporting PPK. The fee rate is 0.03%. from assetsso it will increase automatically over time, regardless of whether the costs of maintaining and developing the ICT system itself will increase at a similar pace.

“As a rule, they do not increase in proportion to assets” – estimates IGTE. It also notes that after several years of operation of the PPK, the scope of tasks actually performed has changed: a significant part of information activities and relations with employers and participants has been taken over by financial institutions.

There is a suggestion that a model combining fixed costs (lump sum) with an element depending on the volume of activities/operations in the portal, possibly with a maximum limit, instead of a simple percentage of assets would be more appropriate.

“Keeping the fee as a percentage of assets means that as the PPK AUM increases, the burden on participants and managing entities increases, which in the long term increases cost pressure on the entire system and may worsen the net results of participants — even though this is not due to the need to cover the higher costs of the portal,” IGTE concludes.

The above proposals, as the authors emphasize, are an invitation to discuss possible changes in PPK, and not criticism of existing solutions or pressure to introduce certain regulations.

Author: Damian Słomski, journalist of Business Insider Polska