Discussion about SAFE fund (Security Action for Europe) is currently one of the hottest topics in Poland, although it largely focuses on political rather than purely financial issues. This project, which is a gigantic EU defense financing instrument, arouses extreme emotions – from the government's enthusiasm to the opposition's sharp accusations of “selling out sovereignty”.

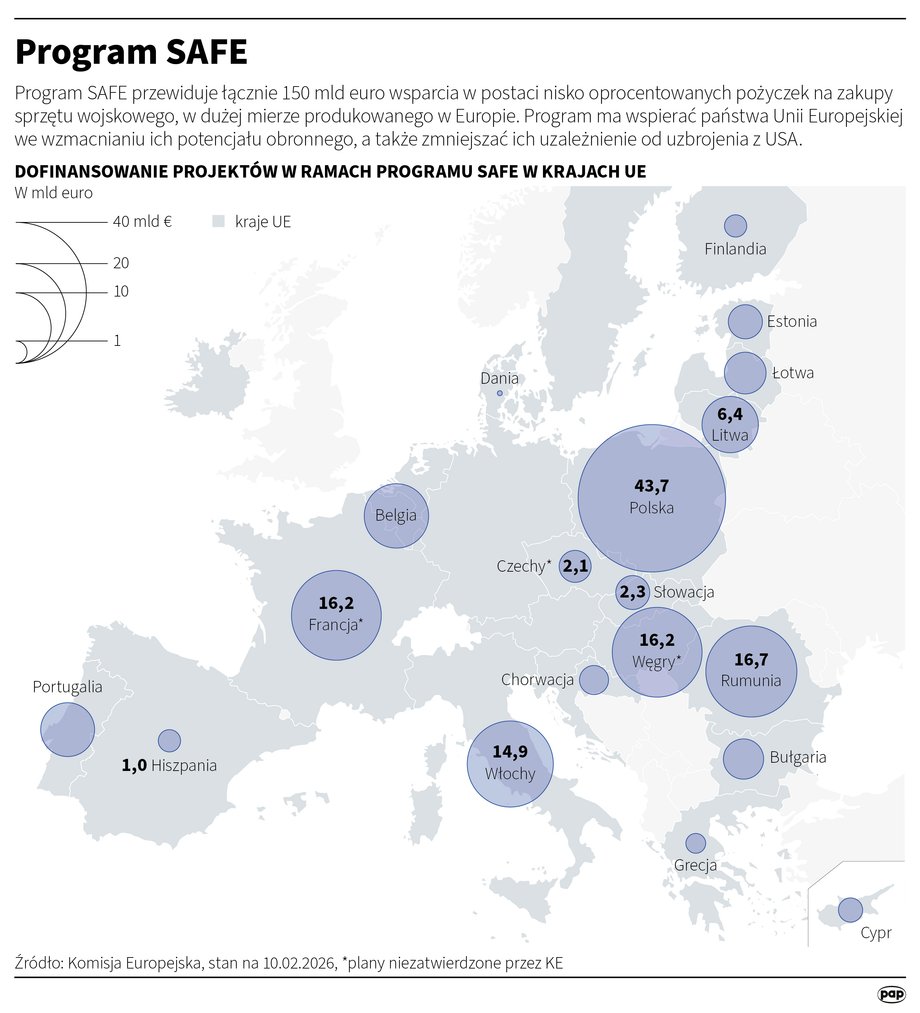

This is a European Union loan program under which Poland will receive close to EUR 44 billion (approx. PLN 185 billion) for the modernization of the army, the construction of the Eastern Shield and the development of the arms industry. SAFE funds are to be used to finance, among others: air and anti-missile defense systems, drones, ammunition and missiles, as well as the protection of space resources and the development of artificial intelligence. The requirement to spend this money within five years may be a challenge.

The rest of the text below the video:

At first glance, SAFE's financial conditions seem favorable: 45 years to repay and 10-year grace period (only interest is paid for the first 10 years). According to calculations by the Ministry of Finance, the interest rate in the first year will be 3.17%. Then it will be variable – depending on market conditions and the cost of bond issuance by the European Commission, which finances the entire mechanism with common debt.

Donald Tusk's government is a strong supporter of Poland's adoption of the SAFE program. The right side of the political scene, led by Law and Justice, believes that this project is unfavorable for us: allegedly, the financing is expensive and pushes us into even greater debt. What is it really like?

Access to money from SAFE is conditional, but…

According to the budget act for 2026, Poland is to spend about PLN 200 billion on defense this year – if the plan is implemented, which is not so obvious – about PLN 200 billion. This means that the impact of preferential loans from SAFE – counted in nominal values - would be significant: we would “get” an additional annual defense budget.

One of the elements of the discussion around SAFE is the conditionality of these funds. However, this is nothing new in the case of EU money. — Conditionality is also included in payments from cohesion and investment funds. The goal is transparent and appropriate spending of funds from the EU budget. Therefore, in order to maintain consistency, the refusal of the SAFE program due to conditionality also calls into question the acceptance of other EU funds, says Marcin Kujawski, economist at BNP Paribas Bank.

The example of Hungary, which had its cohesion funds funds frozen, shows that there is a risk of suspension of SAFE payments. — However, even if someone is afraid of such an event for political reasons, it will then be possible to switch to financing defense projects using bonds – adds the expert.

Read also: Economists are harsh on the idea of the president and the head of the National Bank of Poland. “There is no such thing”

SAFE is a long-term loan, not a bond

Marcin Kujawski estimates that if the investments planned under SAFE are necessary or even necessary from the point of view of Poland's security, then we should not hesitate and join this program, because financially it is attractive.

— The main advantage is that it is a long-term loan. Although we do not know the details yet, I assume that the repayment period may range from 30 years to the maximum 45 years provided for in the program. This means that the refinancing risk is significantly reduced. Additionally, for the first 10 years, only interest will be repaid, not the principal, he notes.

See also: How much of SAFE Poland will go to Germany? The Prime Minister provided the data

A loan or credit is significantly different from a bond. In the first two, the capital is repaid on an ongoing basis (equal or decreasing installments), which means that over time it decreases and the interest (if the interest rate were unchanged) becomes less and less of a burden. In the case of bonds, the capital repayment (a kind of balloon repayment) is due at the very end, so interest continues to accrue on the full capital (in a loan, the last capital installment is negligible).

The challenge with bonds is therefore to repay (annual interest and the nominal amount are returned) or roll over (refinance) the debt at maturity: it is unknown what market conditions and the budget situation will be then. A long-term loan from SAFE, counted in decades, protects us in the event of an increase in geopolitical risk in the coming years, which would hit the markets, increasing the costs of financing with bonds and limiting the possibility of obtaining money in this way.

In terms of the nominal value of loans, Poland would be the largest beneficiary of the SAFE program.

|

Michał Czernek / PAP / photos

It is also important how fast the Polish economy is growing — the more, the less the principal repayment would weigh at the end of the bond's “life.” If the growth rate of Polish GDP was lower than expected in the following years, the SAFE loan would have an advantage (no balloon repayment). It is also important that whether a SAFE loan could be repaid ahead of time (there is no information on this). If this were the case, it would be a beneficial solution for us: we could overpay if market conditions allowed us to finance ourselves with cheaper bonds.

— If Poland were to issue similar debt itself, it would be difficult to obtain such attractive conditions. In case of a loan under SAFE, I assume that after the first 10 years, approximately EUR 1-1.5 billion of capital will mature annually on a straight-line basis, which should not be a problem to refinancea. There will be no need to suddenly roll over tens of billions of euros, as would be the case with bonds. Issuing e.g. 10-year securities means the risk of refinancing, the conditions of such issues in the future are unknown, although of course they may potentially be more favorable than now. The use of a 45-year repayment period provides certainty in this respect, which is a value in itself. This increases certainty in public finance management, says Marcin Kujawski.

If not SAFE, then what?

It is worth combining SAFE with other sources of capital. Poland can finance itself by issuing treasury bonds. Economists, however, draw attention to the upcoming constitutional threshold of 60%. GDP, which – in terms of the State Public Debt (PDP, a narrower measure of debt) we can achieve around 2029. This means that defense debt financing will probably be obtained through bonds, e.g. of Bank Gospodarstwa Krajowego (the Armed Forces Support Fund already does this). However, this is slightly more expensive financing than with treasury bonds (although BGK securities are guaranteed, they are not formally the debt of the State Treasury, and in addition, the market for these securities is shallower than that of “ordinary” treasury bonds).

Euro emissions are also an alternative to SAFE. According to economists it would be difficult to place such large issues on the international market without an adverse impact on bond valuations. Issuances with a total value of PLN 180 billion would increase the foreign debt of the State Treasury by 50 percent, and they would probably not be issues for such a long term as the SAFE loan. Therefore, probably getting financing in euro for 45 years at 3.5 percent. with no capital repayment in the first decade would be possible period only under SAFE.

However, President Karol Nawrocki announced in his Thursday speech that he would not sign the SAFE Act. At the same time, he appealed to the government to consider an alternative presidential project.

SAFE versus Polish debt. What will be cheaper?

Marcin Mazurek, chief economist at mBank, analyzing alternatives to SAFE, assumed that BGK could place securities with a yield of 4.6%. (at least, it could actually be more, but it is difficult to estimate how the market would value a 45-year bond of the Polish development bank). His calculations show that in SAFE, in the first 10 years, the interest will amount to EUR 1.54 billion per year (PLN 6.5 billion each). Later, when the capital decreases regularly (assumes linear repayments), the interest will decrease, but you will also have to repay part of the capital each time. The total interest will amount to approximately EUR 42 billion.

See also: The SAFE program divides politicians and voters. The president faces a choice

In turn, the 45-year BKG bond with a yield of 4.6 percent. will be repaid until 2071, when the last interest and the nominal amount of EUR 44 billion will have to be repaid. The annual interest would amount to EUR 2.02 billion, and the total interest would amount to as much as EUR 91 billion.

“Calculating this way – and assuming that this is how it should be calculated – the difference in favor of the loan is EUR 49 billion (PLN 207 billion – ed.)i.e. just over one billion per year with the full allocation of EUR 44 billion” – wrote Marcin Mazurek on LinkedIn.

Taking into account NPV (net present value, reducing the value of future money to the current value) the difference between BGK bonds and the loan from SAFE, according to Marcin Mazur's careful calculations, would amount to EUR 6.4 billion (PLN 27 billion) in favor of the EU program. He assessed that the loan is much more profitable and this measure is the most adequate.

The government assures that over 80 percent funds from the SAFE program will go to Polish companies and the arms industry.

|

Mateusz Krymski / PAP / photos

— The yield on 10-year Polish treasury bonds in PLN is 5 percent, and in the case of similar BGK securities it is approximately 5.2 percent. Looking at today's market situation, the cost of the loan that the EU can take out to finance SAFE may amount to 3%. These are significant differences, providing the budget with tangible savings. In the case of Polish treasury bonds denominated in euro, the yield on 10-year securities is about 3.3%, and on BGK securities it is about 3.8%, so the differences here are smaller, although in the case of currency issues, the argument of getting rid of the currency risk disappears, says an economist from BNP Paribas Bank.

— In our analyses, we estimate about 1 percentage point. lower interest rate on the loan in this instrument than in the case of attempting to issue debt on the market. This gives approximately EUR 4.3 billion in savings, or approximately PLN 18 billion, only in the first 10 years, when only interest will be repaid – adds Marcin Kujawski.

How serious is the currency risk?

A loan from SAFE is money in euros. This raises questions as to whether this would not mean problems if the Polish zloty weakens against the EU currency. — Since it is debt in euro, there is obviously currency risk. However, debt issued in PLN would be much more expensive. So much so that it is worth taking the risk. Especially since the zloty – apart from crisis periods – is a relatively stable currency compared to the euro. In a worst-case scenario, which I do not expect, if the zloty weakens significantly, we could probably renegotiate the repayment terms. After all, the EU is not an external lender, but an institution of which we are part, says Marcin Kujawski.

It is also worth mentioning that the zloty market is relatively liquid, our currency is convertible, and the state obtains a lot of revenues in euro. We will continue to receive money from EU cohesion funds for years to come. The likelihood of having to buy large sums of euros at one time to repay the principal and interest from SAFE is small (reminder: it's a loan, not a bond).

The financial market positively assessed the SAFE idea

— It is difficult to find financial arguments not to take out a loan from SAFE. Especially since we already issue a lot of bonds both on the domestic and foreign markets. The behavior of the financial market can be interpreted as meaning that the information about plans to join SAFE was well received. In Poland, asset swap rates, i.e. a measure of the fiscal premium included in Treasury bond yields, have recently decreased significantly, notes Marcin Kujawski.

According to the BNP Paribas economist, this was probably due to the better implementation of the state budget last year, but the second argument is the SAFE program, which provides a stable source of attractive financing and may limit the scale of debt supply on the domestic market, which is beneficial from the investors' perspective and they look more favorably at our bonds.

Author: Maciej Rudke, journalist of Business Insider Polska