The low price of love… Tinder, Bumble, Grindr and other dating applications are today a shadow of their former power

Once upon a time, algorithms were supposed to solve the problem of human loneliness, and investors saw it as a goldmine. After all, love is a first-order need. Today, Tinder (Match Group) and Bumble are scraping by, losing several dozen percent from their historic highs in 2021, when the pandemic lockdown and the need for closeness sent valuations skyrocketing. Grindr, its equivalent aimed at the LGBTQ+ community, fares slightly better, but only slightly, but it is still a shadow of its version from a year ago.

The end of the romantic boom, or the stock exchange cemetery of broken hearts

The clash of promises from years ago with today's reality is best seen in stock market charts, which for industry giants today resemble the ECG recording of a patient in a state of collapse.

Match Group, such a symptomatic name for a company in this industry, i.e. the owner of applications such as Tinder, Hinge and OkCupid, definitely failed its “relationship” with the stock exchange. The company's shares, which cost over USD 170 in 2021, are today trying to stay in the area of USD 30-31.

The fourth quarter results published at the beginning of February exposed the fundamental problem of the model: the number of paying users decreased by 5% year on year to 13.8 million, and revenues from Tinder alone are shrinking by 3%.

How does the company save profits? Raises prices. Of course, those who still believe in the algorithm. Revenue per user (RPP) increased by 7% to over $20, and shareholders are reassured by gigantic share buybacks (almost $800 million in 2025 alone) and the growing popularity of the Hinge application – it's like Tinder with a different name, but revenue forecasts for 2026 assume zero growth and stagnation.

Revenge against a former employer running out of gas

The situation is similar with Bumble, an application created by… the former co-founder of Tinder right after she left the startup in the shadow of a loud scandal. The application that became famous for “women take the first step”, debuted in February 2021 at a price of $43 per share (jumping to $76 at the opening). Today the rate fluctuates around just $3 and that means down from the highs by a staggering 96%. So if someone, on a wave of post-pandemic optimism, invested $1,000 in Bumble during its debut, today they only have about $75 left of that amount.

The company is facing a dramatic outflow of paying users. The latest data for the third quarter of 2025 shows that the base of paying customers shrank by as much as 16% year on year, falling to 3.6 million people. For the flagship Bumble app alone, the decline was a painful 18%.

The lifeboat here is the same as in the case of Tinder, i.e. it is based on squeezing the maximum out of those who are still in the application. Bumble raised prices, which increased average revenue per user (ARPPU) by nearly 7% to over $22, but the company's total revenues decreased by 10% anywayand the forecasts for the turn of 2025 and 2026 leave no doubts, assuming a further double-digit decline (even by 14-17% y/y).

Gays and lesbians pay more, a loyalty-driven anomaly

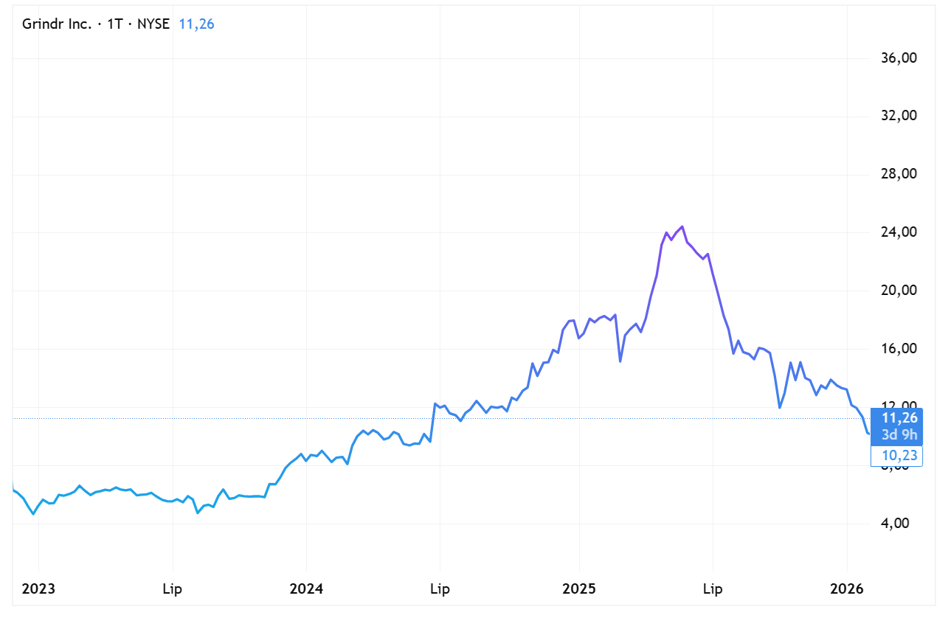

However, in this stock exchange graveyard of broken hearts, we can find one very interesting case. This is Grindr – the exception that proves the rule. Although the company's price has also experienced considerable turbulence and fell to around USD 11 in February 2026 (from last year's peaks of over USD 25), from a fundamental point of view this business is escaping the industry downturn.

Unlike Tinder or Bumble, which are losing customers, Grindr delivers results that continue to impress. Data for the third quarter of 2025 show that the company's revenues increased by an impressive 30% year over year (piercing USD 115 million in one quarter) and the margin adjusted EBITDA increased to 47%. Moreover, forecasts for 2026 still assume aggressive, double-digit growth.

What causes this anomaly? The reason is a loyal, strictly defined target group with completely different engagement dynamics. While users of traditional dating applications quickly feel tired (the so-called Dating App Fatigue), Grindr statistics show a completely different world: users spend there on average as much as 70 minutes a day, and the application for the LGBTQ+ community has long ceased to be just a dating tool, becoming an integral element of everyday communication, or – as the management itself calls it – a “global, digital gay district” (Global Gayborhood). Grindr users are much less likely to delete the app after finding a partner, which allows the company to effectively bypass the “dating business paradox” and ruthlessly monetize its base of over a million paying users.

Fatigue of the material, i.e. Dating App Fatigue

Why has the stock market turned away from Tinder and Bumble? The answer does not lie in complicated financial indicators, but in the social mood and the phenomenon that has already been mentioned in this text. We are currently observing the phenomenon of “Dating App Fatigue”. For Generation Z (today's 20-somethings), Tinder is no longer synonymous with modern dating. The youngest adults are going back to their roots – they are looking for partners organically.

Another blow to the industry is the ongoing “enshittification” (a term coined by Cory Doctorow, meaning the gradual degradation of quality on digital platforms in favor of profits). Apps have become a pay-to-play format. Free users feel invisible, relegated to the bottom of the digital profile stack. To do anything, you need to buy a Premium package, Super Likes or VIP status, which in the era of inflation and high costs of living is one of the first expenses that go under the knife.

A business model that kills business

All this leads to a fundamental, even fatal error in the DNA of these companies. The industry has hit the wall of its own business model, which is based on an insoluble paradox: a perfectly working product means the irreversible loss of a paying customer. If the algorithm actually finds you the love of your life, you simply delete your account and unsubscribe.

When the management boards of the giants realized that happy couples could not generate infinite growth and dividends for shareholders, they changed the rules of the game. Algorithms stopped effectively connecting people and started optimizing their frustration. They have been programmed to dispense successes rarely enough to keep the user in the application for longer, and often enough to make them pull out their credit card in an act of desperation.

Users have finally seen through this system. The stock market's valuation of love is sinking to the bottom, and investors are now learning from their own portfolios what millions of singles have known for a long time: nothing meaningful will come from this “relationship”.