Poland imports gas, among others, from the USA, where government representatives regularly visit, including the Minister of Finance Andrzej Domański and Wojciech Wrochna, the government plenipotentiary for strategic energy infrastructure. Their talks with the Americans concern, among other things, the import of this raw material. It is in these circumstances that the concept of Poland as a gas hub is born.

Read also: Construction of a nuclear power plant and the Central Communication Port with the participation of BGK. What amounts are involved? [WYWIAD]

Poland – a gas hub for Central and Eastern Europe?

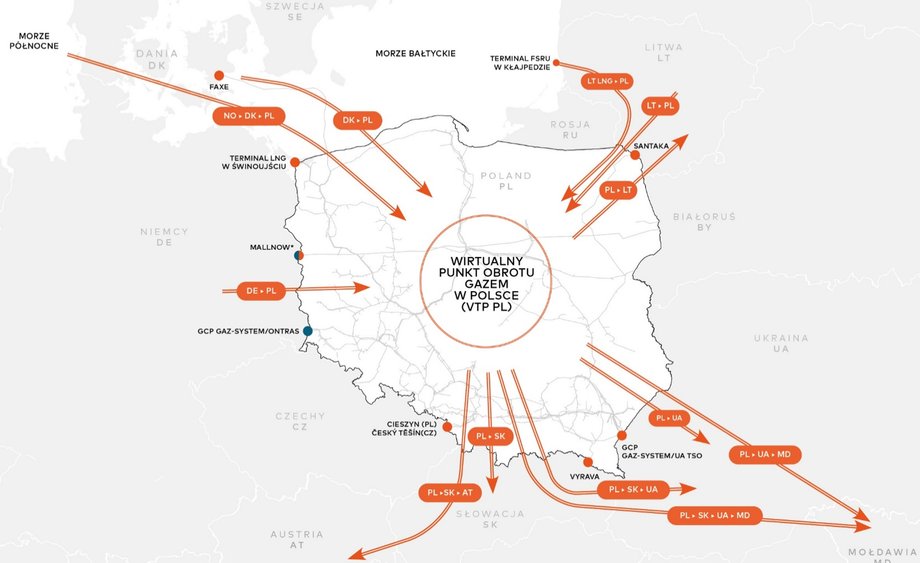

Minister of Energy Miłosz Motyka spoke about this in November in Athens during the P-TEC energy conference. He emphasized that Poland is able to perform such a function for the entire region, including Ukraine, in the so-called transition period of energy transformation. Our transmission capabilities can be seen on the map below.

Possibilities of gas transmission through Poland

|

Gas System

Motyka, in response to questions from Business Insider Polska, recently said that We are expanding the infrastructure and the northern corridor has a chance to become a key supply gate for this raw material for our region. — This is an element of geopolitics – emphasized the Minister of Energy.

Read also: Polish ports are breaking records. The government announces new major investments

Poland's potential amounts to billions of tons

In Poland, we use approximately 20 billion cubic meters. gas per year, and in the coming years, according to Orlen's estimates, this level is expected to reach 27-30 billion cubic meters. gas per year.

However, calculations by the Energy Policy Institute show that our country may have the ability to import as much as 50 billion cubic meters. gas per year.

As Aleksander Zawisza, an expert at the Energy Policy Institute, explains, for cost and logistic reasons realistically, we will be able to re-export the difference between domestic production (mining plus biomethane) annuallyown possibilities of import from the sea, partly import from Lithuania and own consumption.

In 2024, according to Orlen's data, natural gas supplies were based primarily on production in Poland (approx. 3.3 billion cubic meters), imports through gas connections with neighbors and the Baltic Pipe – approximately 7.3 billion cubic meters. and thanks to the supplies of liquefied natural gas (LNG) to the gas port in Świnoujście, which is celebrating its 10th anniversary this year – approx. 6.4 billion cubic meters.

However, a floating gas reception terminal (FSRU – Floating Storage Regasification Unit), i.e. a floating unit for storing and regasifying liquefied natural gas LNG in Gdańsk, is under construction, and Poland plans to build another such unit. Market research in this respect is currently underway.

The total import capacity is presented in the chart below.

The advantage of the Poland gas hub is its developed transport infrastructure

The Minister of Energy points out that Poland has long been becoming independent from imports of raw materials from the East, and at the same time it is expanding its storage and transmission infrastructure. At the same time, he adds, it is also a politically and economically stable country.

— This gives other countries in the region a basis to trust Poland, and our partners from the United States know this very well. These good relationships are maintained and conversations continue. Our ambition is to become the leader of this project, emphasizes Miłosz Motyka.

LNG delivery in Świnoujście

Minister Motyka's opinion is confirmed by Mateusz Kubuszek, gas trading expert at MET Polska. As he argues in an interview with Business Insider Polska, transforming the country into a regional gas hub is no longer an ambition. – Our country is becoming a new reference point on the supply map for Central and Eastern Europe – emphasizes the expert.

Kubuszek points out that the foundation of this change is “solid physical infrastructure, which has reached critical mass in recent years.”

Read also: Gas does not disappear from the energy mix. The government and Orlen are focusing on biomethane, but the transformation will take decades

— After the expansion of the LNG terminal in Świnoujście and the launch of the Baltic Pipe, Poland now has diversified sources and a regasification capacity unique in the region. The National Transmission System, with a capacity more than twice the national demand, is connected with all neighbors by interconnectors – says the MET Polska expert.

He adds that Polish transmission capacity will be additionally strengthened by the FSRU terminal in Gdańsk planned for 2028. It will increase the total capacity for global LNG supplies to approximately 14.4 billion cubic meters. annually. Mateusz Kubuszek emphasizes that this is a key advantage of Poland that landlocked countries lack.

Read also: What will Poles gain from the reconstruction of Ukraine? Here are the options on the table

The geopolitical situation is of key importance for gas import and export

Kubuszek sees the current geopolitical situation as the main catalyst for changing the country's role on the gas market. — Poland, thanks to direct access to LNG and Norwegian gas, becomes a natural intermediary in this scenario. Our country is ready to fill the gap created by the closure of the eastern direction – he explains.

Marek Niedużak, director for Poland of the European Initiative for Energy Security think tank, sheds additional light on the whole matter. — Polish ambitions to become a regional gas hub do not depend only on Warsaw. The decisive factor here is the very dynamic expansion of American LNG gas from various directions to the markets of Central and Eastern European countries, he says.

As an example, he cites the recent agreement between Kiev and Athens, supported by Washington, or the import of LNG by the Ukrainian company DTEK through the terminal in Klaipėda. — Polish plans to expand the FSRU terminal are part of this broader trend, he concludes.

Baltic Pipe – tunnel drilling, Pogorzelica

Can these countries import gas via Poland?

Miłosz Motyka mentions Ukraine and Slovakia among the recipients of gas from Poland. As he says, talks are underway with Bratislava.

– No decisions have been made, but we are on the right track – he says. He also admits that “financial issues related to the price for individual consumers will always be decisive and crucial for our neighbors.” – I think that we will arrange the format of cooperation in such a way that the interests of the end recipient in Slovakia and our country will be adequately protected – he says.

As Dominik Brodacki, head of the energy department of the Polityka Insight analytical center, tells Business Insider Polska, Due to our location, it is the most attractive sales market for us Ukraine. – This is a very absorbent market, and it will be even more absorbent due to the reconstruction of Ukraine, if the broadly understood West takes part in the reconstruction – he notes.

According to him, Slovakia and Hungary are definitely at stake, as they are currently dependent on gas from Russia. For now, as he admits, we will not conquer the Western world, because liquidity and prices there are much lower.

— The market research conducted by Gaz-System in the fall of this year showed that the demand for LNG in 2031-2032 exceeded the planned capacity of the installation of the second FSRU unit in the Bay of Gdańsk almost four times. At the same time, almost half of the reported demand came from Ukraine, Slovakia, the Czech Republic and Lithuania – notes Marek Niedużak in an interview with Business Insider Polska.

According to Mateusz Kubuszek, this will confirm Poland's role as a regional distributor. – The fact that market participants express a preference for long-term contracts is a signal of real and non-speculative capital commitment, which is preparing for the binding Open Season procedure in the first quarter of 2026 – he argues.

In the opinion of the MET Polska expert, the benefits for entrepreneurs in the region are twofold. Firstly, security of supply will reach a new level, providing access to gas from many diversified sources. Secondly, an increase in turnover on the Polish Power Exchange (TGE) and achieving a trading volume of over 16 billion cubic meters. per year with the FSRU fully loaded, will create scope for real price competition.

— Companies will gain the opportunity to purchase raw materials at transparent, stock exchange prices, instead of relying on the conditions dictated by dominant domestic players, the expert says.

For Poland to become a gas hub, the Świnoujście LNG terminal will not be enough

— Looking to the future, the optimistic scenario is firmly based on reality. If the Open Season procedure is successful, Poland has a chance to export 5-8 billion cubic meters. gas per year to neighborsand TGE will become a significant regional price hub. In our opinion, this scenario is not a fantasy, but a logical consequence of changing geopolitics and documented market interest – says the MET Polska expert.

However, as he adds, the condition for its implementation is the efficient implementation of the investment and maintaining growing liquidity on the stock exchange market. – Poland now has a privileged position, which it must use efficiently before competitive hubs in other countries catch up with our progress – emphasizes Mateusz Kubuszek.

A ship dredging the bottom for the construction of a floating gas terminal (FSRU) in Gdańsk

Aleksander Zawisza, an expert from the Energy Policy Institute, also believes that without a second FSRU unit and the development of the biomethane market, which will fill the gaps in the falling domestic production of natural gas, it will be difficult to talk about a real gas hub in Poland with its own independent sources and the potential to compete on price.

— In the event of a shortage of FSRU II, the existing infrastructure will meet national needs. We will be able to send gas to the south in the summer, but in the winter we will also import it from Germany, because our capacity to cover the winter demand will be too small. – explains Zawisza.

Poland must meet several conditions

Dominik Brodacki also believes that Polish ambitions have solid foundations. — Thanks to our infrastructure, we are able to receive gas in the form of LNG from virtually anywhere in the world and send it to neighboring countries: Lithuania, Ukraine, Slovakia, and further to southern Europe, also to the Czech Republic, although in this case there has been talk of building a new gas pipeline for years, but this has not happened, he argues.

Technically and volume wise, we are able to supply gas. However, as the expert emphasizes, the price of gas is also important – our gas must be price competitive to be attractive to customers in other countries. — However, there is a problem with this, because gas in Poland is one of the most expensive in Europe, and there is little competition on the market compared to the German or Dutch markets. – Dominik Brodacki points out.

Read also: Poland is breaking new records. The first such situation in history

Price and a competitive market are key

The price depends primarily on how much gas we import from different directions. Who trades this gas, what is the number of entities and how much gas passes through the exchange.

– For this to change, it is necessary to increase competition on the gas market. For this purpose, among other things, the Ministry of Energy plans to increase it to 85%. the so-called exchange obligation for gas precisely to force gas to be traded not in bilateral contracts – says Brodacki.

He adds: – At the same time, this stock market will cover a larger number of entities, which will result in prices being determined in a more market-oriented manner, and not as a result of bilateral arrangements between the supplier and the recipient. We have gas, we have infrastructure, we need even lower gas prices and a competitive market.

Aleksander Zawisza adds: – From the regulatory side, if we want to create a hub, the Act on Inventories must change, among other things – its current shape limits the development of the market and competition in our country.