After several years of one-sided legal battles, the share of judgments favorable to borrowers reaches 97%. (courts declare the contract invalid) – the franc saga is slowly coming to an end. Although there are still many cases of this type pending in courts and there will still be many of them (appeals and so-called counter-claims) and there remain legal ambiguities regarding the method of settlement between the lender and the client after the contract is invalidated, in financial terms Polish banks have already borne the greatest cost of the Swiss franc problem.

Before we move on to the amounts, it is worth showing the scale of the problem. Different sources indicate different data, but according to our estimates, based on the statistics of the Credit Information Bureau, Polish banks granted a total of PLN 775,000. Swiss franc mortgages. The peak occurred in 2006–2008, when 127,000, 149,000 and 149,000 were sold, respectively. and 109 thousand with a value of PLN 28 billion, PLN 29 billion and PLN 43 billion respectively (calculated at the exchange rate on the date of granting). It was a time when the zloty was exceptionally strong, and the franc exchange rate fluctuated in the range of PLN 2-2.75 for a long time (the average rate for taking out Swiss franc loans was about PLN 2.55). Currently, the price for the Swiss currency is approximately PLN 4.55, and there were months when it was even close to PLN 5.

The text continues below the video:

The portfolio of Swiss franc mortgages has shrunk significantly

In 2012, when Recommendation S came into force, forcing the loan currency to match the currency in which the client earns money, only 600 such loans were granted. A decade ago, when on January 15, 2015, the Swiss National Bank stopped defending the exchange rate of its currency against the euro, there were approximately 562,000 Swiss franc mortgage agreements. (repaid by 980,000 people, mainly married couples), worth PLN 136 billion. The number of contracts could drop to around 142,000. currently, which is caused by natural repayments, invalidation of contracts by courts and settlements.

See also: The annulment of mortgages brings great benefits to Swiss franc borrowers. PLN borrowers may envy you

The increase in the Swiss franc exchange rate, which translates directly into the value of the principal to be repaid in PLN and the amount of the installment, outraged the borrowers, who went to court. Initially, they filed group lawsuits, which dragged on and lasted for years, and additionally, the case law for Swiss franc borrowers was not favorable. Various concepts for statutory regulation of this problem have been created, but politicians have never decided on a law. The doubts were dispelled in February 2017, when Jarosław Kaczyński, president of PiS (his party was in power at that time), announced that Swiss franc borrowers should take matters into their own hands and fight in the courts.

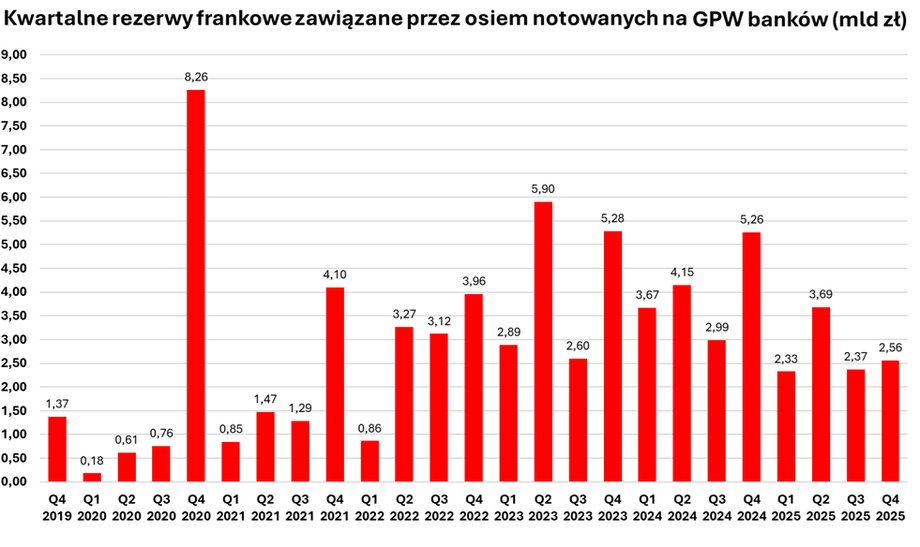

The group of banks analyzed includes: PKO BP, Pekao, Santander, mBank, ING Bank Śląski, BNP Paribas, Millennium and BOŚ.

|

banks, own study

Resolutions of the Supreme Court favorable to borrowers and the famous judgment of the Court of Justice of the European Union in the case of Mr. and Mrs. Dziubak (issued in autumn 2019) changed the line of jurisprudence. Franc borrowers began to win en masse, which resulted in an avalanche of lawsuits.

See also: Swiss franc borrowers get summonses. They may have to pay high interest rates to banks

At the end of September, there were 182,000 cases in court. active Swiss franc cases (compared to 204.1 thousand at the end of 2024), of which approximately 50 thousand this is the so-called counter-suit (proceeding in which the bank demands the return of capital as part of the settlement of a canceled contract). It is also worth remembering that a large number of contracts have already been legally settled, so they are not included in the statistics of pending lawsuits or active loans (according to the National Bank of Poland, by the end of the first half of 2025, 59,000 cases were legally concluded).

Over PLN 100 billion went into the pockets of Swiss franc borrowers

Lost cases mean a huge financial cost for banks, which must set aside reserves for this purpose. The first significant ones appeared in the fourth quarter of 2019, when the wave of lawsuits began to increase and the judgments began to be clearly favorable to borrowers.

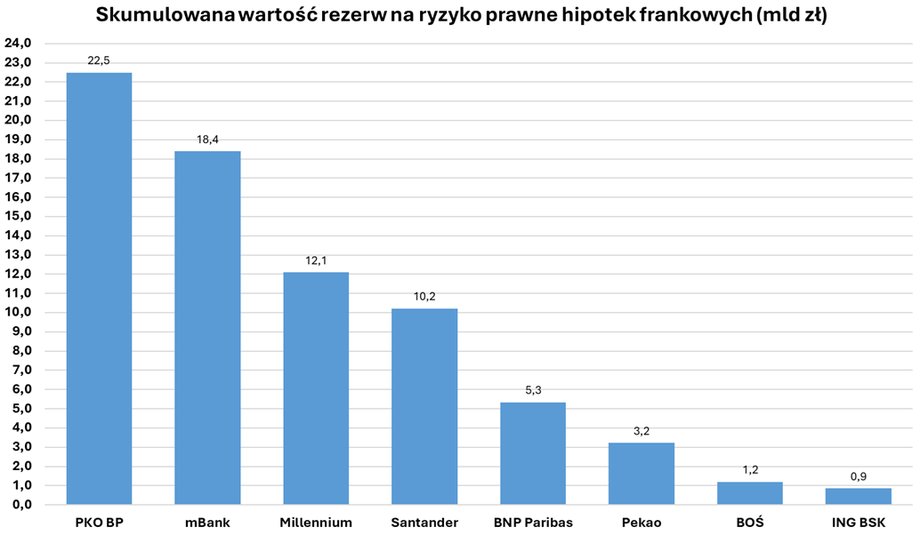

According to our estimates, at the end of 2025, the banking sector had a total of over PLN 102 billion in reserves for Swiss franc mortgages.. This account is based on the reports of eight listed banks and estimates of reserves in other institutions, such as Getin Noble Bank (compulsorily restructured in 2022), Raiffeisen Bank International, former BPH and Deutsche Bank Polska. This money went to a relatively small group of people, numbering in the hundreds of thousands, at the expense of bank shareholders (including indirectly participants of funds such as OFE, TFI, PPK), among others. State Treasury (controls over half of the assets of the Polish banking sector).

This is a huge amount, because the gross value of Swiss franc mortgages at the end of 2019 was PLN 98 billion: this was the value without any reserves. The sum of write-offs made over six years can also be compared to the banks' equity – at the end of 2019, they amounted to approximately PLN 210 billion (the sector's current capital – inflated with great profits thanks to high interest rates – amounts to nearly PLN 320 billion).

There are banks – such as mBank or Millennium – whose total reserves are close to their current capital and much higher than those from six years ago. For example, mBank created as much as PLN 18.4 billion of this type of reserves, and its equity at the end of September 2025 (the latest available data) amounted to PLN 20.4 billion. In the case of Millennium, these proportions are even clearer: the established reserves amount to a total of PLN 12.1 billion, and the current value of capital is PLN 8.8 billion.

Banks have established Swiss franc reserves from the fourth quarter of 2019 as a result of an unfavorable change in case law caused by, among others, the judgment of the CJEU in the case of Mr. and Mrs. Dziubak.

|

banks, own study

“The legal risk related to foreign currency loans remains significant, although its impact on the stability of the financial system has been significantly limited. The scale of the reserves created means that the sector is now well prepared for the further materialization of this risk. Nevertheless, the costs related to foreign currency housing loans will continue to constitute a burden for banks in the coming quarters,” we read in the December “Financial Stability Report” prepared by the NBP.

Billions more are possible in reserves for foreign currency mortgages

NBP data shows that by mid-2025, banks and borrowers signed approximately 156,000 settlements regarding foreign currency housing loans, including approx. 35 thousand with clients who had previously sued the bank. “Concluding a settlement is beneficial to both parties to the process, as it significantly shortens the time needed to resolve the dispute and avoids additional costs associated with lengthy court proceedings,” it was noted.

Banks have so far created significant provisions, but due to the possibility of further disputes arising, they still incur the costs of creating additional provisions. Representatives of leading Swiss franc banks have recently indicated that in 2026, write-offs for this purpose will no longer be significant in the scale of their institutions' results. However, the NBP is skeptical and more cautious.

According to the National Bank of Poland, approximately 40 percent the established reserves have already been used to cover the costs of materialization of legal risk (costs of settlements and costs of final judgments), 60 percent is intended to cover further costs of this risk. Banks adapt their write-off models to current conditions and forecasts regarding, among others, the number of court disputes and average loan losses (which is influenced by, among others, the Swiss franc exchange rate or the terms of individually negotiated settlements).

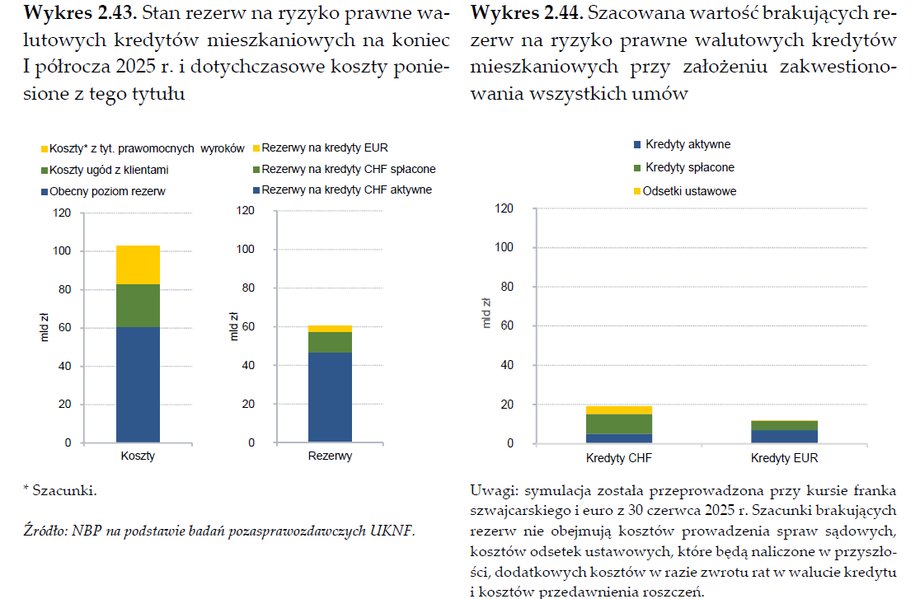

According to estimates by the National Bank of Poland, banks may be forced to create reserves amounting to as much as several billion zlotys.

|

National Bank of Poland, Polish Financial Supervision Authority

“The costs resulting from legal risk have already been covered to a large extent by banks, but the need to establish additional provisions cannot be ruled out. Assuming the extreme scenario of customers questioning all foreign currency housing loan agreements (CHF + EUR), including repaid loans, it can be estimated that the missing provisions for this risk could exceed a total of PLN 30 billion,” NBP reported in the “Financial Stability Report.”

In this amount, the estimated value of provisions relating only to active currency loans would amount to approximately PLN 12 billion. The potential provisions necessary to cover the risk of lawsuits filed by borrowers who have already repaid their liabilities would be higher (approx. PLN 15 billion) due to the current low coverage of these loans with provisions. Moreover – as noted by the NBP – due to the long duration of court proceedings, additional provisions for statutory interest may be needed (the estimated cost of interest accrued by the end of the first half of 2025 is approximately PLN 4 billion). It was added that the entry into force of the “franc law” proposed by the Ministry of Justice would reduce this amount due to the expected shortening of court proceedings.

Author: Maciej Rudke, journalist of Business Insider Polska