Investing without tax Belka. What benefits can a Personal Investment Account bring?

The government has finally presented a draft law introducing the Personal Investment Account. It is intended to allow investors to benefit from fiscal benefits, which it will mean the possibility of achieving higher real rates of return.

OKI is intended to be a personal and voluntary solution, intended for individuals, with the possibility of depositing and withdrawing money at any time without losing tax benefits. People who are over 18 years of age will be able to set up OIC.

It will be possible to have several OICs, e.g. in a brokerage house or investment fund, but only from the beginning of 2028 (until then, it will be possible to set up only one OIC). The limit will not change and will still amount to a total of PLN 100,000. PLN (regardless of the number of accounts). For now, there are no plans to introduce an upper limit on assets accumulated in OKI.

Read also in BUSINESS INSIDER

You can “package” in OKI, among others: deposits, securities admitted to trading on the stock exchange (e.g. WSE or NewConnect), financial instruments that are not securities (e.g. ETFs), treasury bonds and participation units in funds. Note: the list does not include, among others: cryptocurrencies or CFDs (contracts for differences, an instrument “pretending” to be e.g. shares). When will the new instrument be available? Previously, the government announced that the OIC would enter into force in mid-2026.

|

Ministry of Finance

Although it will be possible to buy foreign instruments at OKI, the tax exemption will de facto only cover assets denominated in Polish zloty. This applies, for example, to shares and ETFs listed on the Warsaw Stock Exchange. One small exception was left for investment funds whose investment policy assumes that at least 70 percent their assets will be invested on the WSE, and only 30 percent abroad (but not around the world: an additional limitation here is the need to invest in European and OECD countries).

OKI can be operated by banks, brokerage houses, investment funds, OFEs and insurers. The taxpayer will have to settle the tax on assets in OKI on his own. The returns must be submitted by May 31 following the tax year and the tax must be paid by the same date.

This is how you can avoid Belka's investment tax

The general rule is quite simple. Assets accumulated in OKI up to PLN 100,000. PLN are to be exempt from capital gains tax (Belka tax), which is 19%. Here is the first important caveat: in the case of bank deposits and retail Treasury bonds, the total amount of non-taxable assets is PLN 25,000. zloty. By the way: in 2026, there will be a transition period and the limits will be lower (PLN 12,500 in the savings part and PLN 50,000 in the investment part).

The simplest example (assuming target parameters): if an investor has shares in OKI worth PLN 75,000. PLN, and the remaining 25 thousand. PLN, he will not have to pay Belka tax on dividends and interest. The same applies to the sale of shares: unless the total funds in the account exceed PLN 100,000. PLN, the tax office will not collect a penny. Limit applies asset valueand not just profit or paid-in capital. For example, if an investor deposited PLN 80,000. PLN, and the valuation went up by PLN 15,000. PLN and in total he has PLN 95,000 for OKI. PLN, then in the event of selling the shares and realizing the profit, he will not pay Belka tax.

OKI introduces a “new” tax on assets

Assets over PLN 100,000 PLN will be taxed with a new levy (instead of the Belka tax). Its rate will vary depending on market conditions. This is the result of multiplying 19%. By NBP reference rate effective on October 31 of the year preceding the tax year. Now it will be 0.85 percent. However, it cannot be lower than 0.1%. It will be applied to the taxpayer's assets, which are recalculated daily. As interest rates increase, the tax rate will increase (and vice versa).

“The tax on the value of assets is a special tax, i.e. it is not strictly an income tax or a property tax,” it is written in the justification of the proposed act.

What if the investor has treasury bonds and deposits worth more than PLN 25,000 in OKI? zloty? In this case, asset tax will be applied (it will be charged on deposits and treasury bonds worth more than the limit of PLN 25,000, up to this amount Belka will enjoy no tax).

How does the tax on assets in OKI compare to the regular Belka tax?

Although this results from the structure and principles of OIC, it must be written clearly: in this system it will be possible – in fact, this is one of its key features – to benefit from fiscal optimization for assets worth over PLN 100,000. zloty.

This solution supports active investors looking for higher potential rates of return, i.e. investing, for example, in shares (directly or through funds) as well as in corporate bonds. However, this solution also has its drawbacks: it carries the risk of paying tax on assets even when the investment brings a loss. However, people for whom such tax risk is too high will have a choice – they can stay with the current method of taxation, i.e. the Belka tax. Thanks to OKI, savers will have a much better choice in how to manage their investments.

Tax on assets over PLN 100,000 PLN is to be paid every year regardless of whether you managed to make a profit (the value of the portfolio increased) or whether there was a loss (the valuation decreased). At the same time, in the case of shares in this part of the portfolio, you will have to pay “ordinary” tax on dividends obtained (as before, i.e. 19%).

|

XTB Research

In other words, if a portfolio valuation of, for example, PLN 300,000 PLN will increase to PLN 390,000. PLN, i.e. by 30%. due to the increase in market quotations (we do not assume additional payments), the amount of tax on assets will increase – even if the investor has not sold a single share – from PLN 2.6 thousand PLN up to PLN 3.3 thousand zloty. However, if the investor decided to realize a profit, he would have to pay Belka tax of 19%. from earnings. The tax amount would, of course, depend on how many shares he would sell.

And on the other hand: if the valuation dropped, e.g. from PLN 300,000 PLN up to PLN 210 thousand PLN (30% reduction), the investor would still have to pay PLN 1.8 thousand. PLN tax (even if he did not sell a single instrument). This is a completely new tax formula, because you will have to take money out of your own pocket to pay the tax, even if they have not sold a single instrument. So far, investors were used to paying the tax office if they made a profitable transaction, so they had money to pay tribute.

Application of taxation on assets over PLN 100,000 PLN, instead of Belka's tax, will reward active investors achieving high rates of return, and may not necessarily favor the “buy and hold” strategy (although this is not certain, a lot depends on the specific situation). It may also make it difficult for investors who react poorly to a temporary drop in valuation to survive difficult times on the market (not only will their valuation drop, but they will have to pay tax).

|

XTB Research

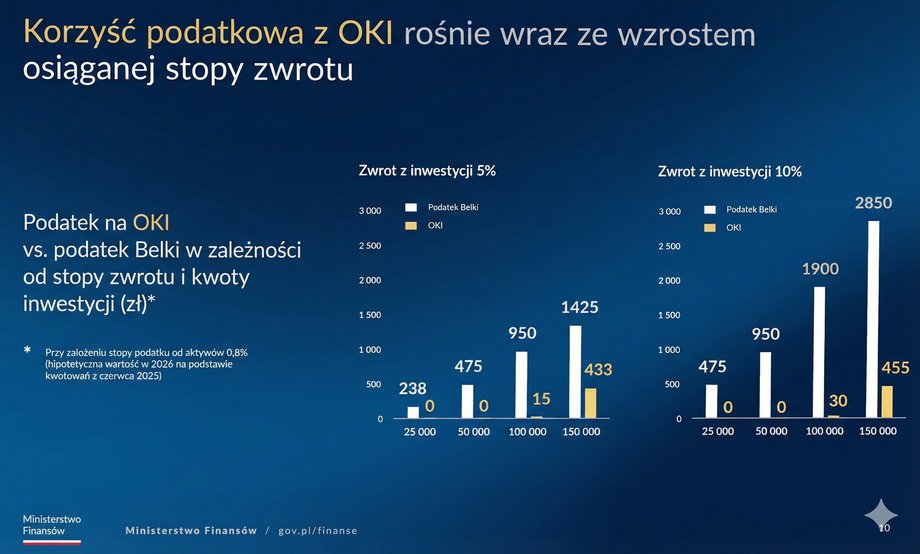

The essence of tax on assets over PLN 100,000 PLN can be reduced to the following statement: the higher the investor manages to achieve the rate of return on capital in OKI, the more you will gain from the fiscal relief compared to the Belka tax.

With a portfolio worth PLN 1 million and 10%. rate of return (and this is not a particularly high result during a boom), the tax in OKI would amount to approximately PLN 8.5 thousand. PLN compared to 19 thousand in Belka's tax. However, if the investor earned only 3%. profit with the same capital, he would pay the same tax on OKI, but according to Belka's tax only PLN 5.7 thousand. zloty. To put it simply: the larger the portfolio and the lower the rate of return and the higher the tax rate on assets, the worse OKI performs compared to Belka's tax (and vice versa).

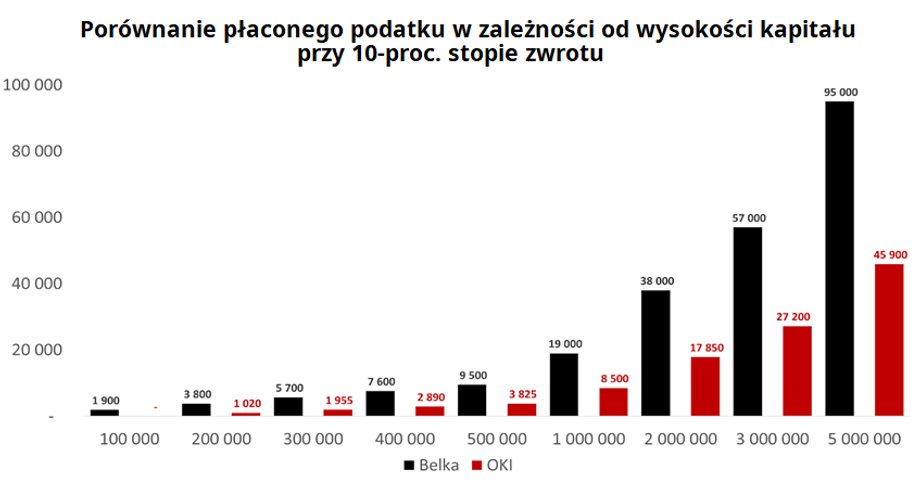

OKI performs slightly worse (though still better), assuming a lower rate of return. In the case of 5 percent profitability, tax benefits are still visible in the value of tax paid over the value of portfolios up to PLN 5 million.

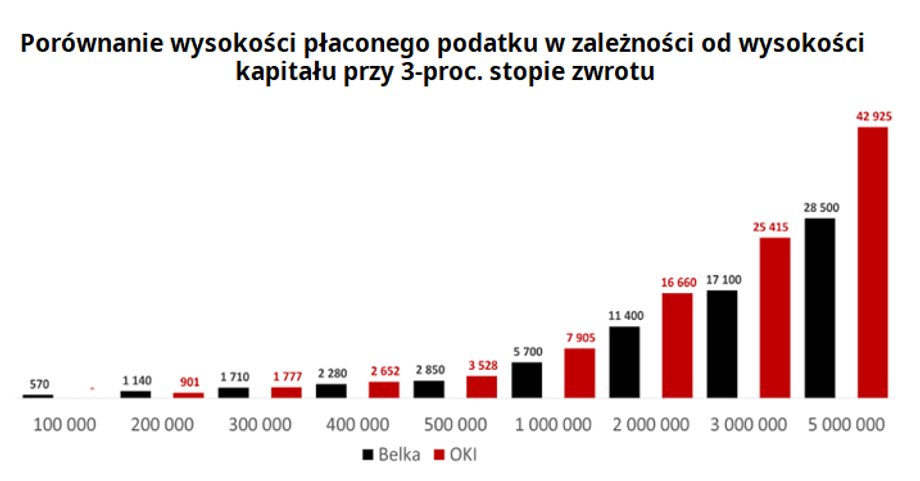

However, if we lowered the assumed rate of return to 3%. (as shown in the second chart), then OKI does not perform so favorably. For wallets over PLN 300,000. PLN, the tax paid in the case of OKI will be higher than in the case of Belka, and the difference will grow faster and faster with greater capital.

OKI good for the corporate bond portfolio (including mortgage bonds)

One of the popular solutions that can be used by people willing to invest in bonds will be the purchase of debt securities worth up to PLN 100,000. zloty. The interest on such a portfolio will not be taxable. Partly up to PLN 25,000. PLN may be treasury securities, and some of them may be up to PLN 75,000. PLN corporate.

Covered bonds, i.e. very safe securities with an interest rate and risk comparable to treasury bonds rather than typical debt issued by companies, may be a particularly good fit for OKI. Their variable interest rate means that – unlike fixed-rate bonds – their valuation is not susceptible to changes in interest rates (as official rates fall, the prices of fixed-coupon bonds increase and vice versa).

For a very cautious investor, a solution worth considering would be to invest PLN 25,000 within OKI. PLN treasury bonds, and the remaining part (PLN 75,000) could be allocated to mortgage bonds. Thanks to this, he would not pay Belka's tax on the full PLN 100,000. PLN while maintaining low risk.

Author: Maciej Rudke, journalist of Business Insider Polska