The National Bank of Poland sees inflation as a target. But only in 2027. And higher than in July

The November inflation projection of the National Bank of Poland assumes that we will see CPI inflation at the 2.5% target only in 2027. Moreover, the central path of the latest CPI projection is higher than in the July projection.

During the November press conference, NBP President Adam Glapiński trumpeted success across the board. – From maintaining interest rates at a very restrictive level for a sufficiently long time, to lowering interest rates this year – we managed to perform all these sequences correctly – said the helmsman of Polish monetary policy.

– Over the entire projection horizon, i.e. 2 years, inflation should remain within the NBP target, i.e. 2.5% +/- 1%. This allowed us to decide to reduce interest rates, added President Glapiński.

And he was partly right. In fact, CPI inflation in October 2025 was 2.8% for the fourth month in a row was within the permissible (+/- 1 percentage point) deviation from the target. But at the same time alone The NBP's 2.5% target has remained virtually unachieved for 6 years. For just In 4 of the previous 72 months, CPI inflation was within the NBP target. As a result, this target was permanently exceeded, both in the medium and long term. The average (geometric) CPI inflation for the last 5 years was 7.47%, for 10 years it was 4.51%, and for 20 years it was 3.35%.

What did the November NBP projection tell us?

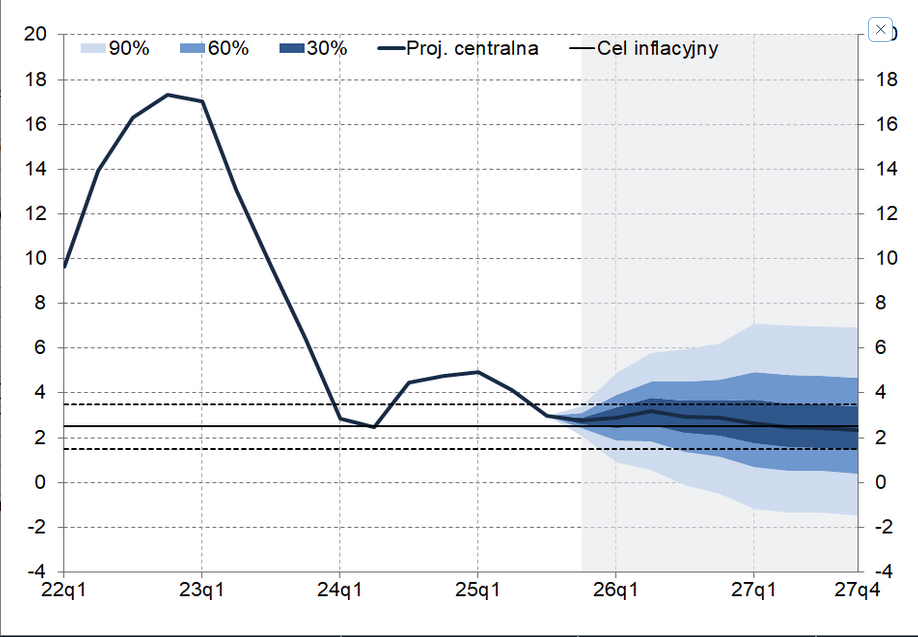

On Friday, the National Bank of Poland published the latest inflation projection. This projection is the result of feeding the NECMOD econometric model with fresh macroeconomic data. This model calculates that with a given probability CPI inflation will be at a specific level assuming that interest rates remain unchanged. And we already know that this condition will not be met, because on Wednesday (i.e. after preparing the projection), the Council reduced the NBP rates by 25 basis points, thanks to which the WIBOR 3M rate decreased to 4.30%. And the NECMOD model assumed it at the level of 4.62% starting from the fourth quarter of 2025 until the end of the projection horizon.

It is also basically certain that the Monetary Policy Council will continue to cut interest rates next year. Although much slower and more cautious than in the previous six months, when it reduced the interest rate on the zloty by as much as 150 basis points. Market economists assume that in 2026 the cycle of reductions will end with a reference rate of 3.50-4.00%. That is, by 50-75 bps. lower than currently.

But even if the Council did not decide on these cuts, the latest inflation projection assumes that CPI inflation will reach the 2.5% target only in the second quarter of 2027. And it will remain at this similar level until the end of 2027. Let us add that over the entire horizon of the November projection (i.e. until the end of 2027), core CPI inflation does not reach the inflation target, falling to 2.6% in the fourth quarter of 2027 (currently it is approximately 3%).

Of course, this is just a project “spit out” by a certain mathematical model, the assumptions of which include the principle that inflation in the medium term always heads towards the target. As we already know from 2019-22, this assumption does not always prove true. Secondly, the source data entered into the model change over time and, for example, the March projection may show both a lower and higher path of future inflation than currently. Here everything depends on the shape of the input data.

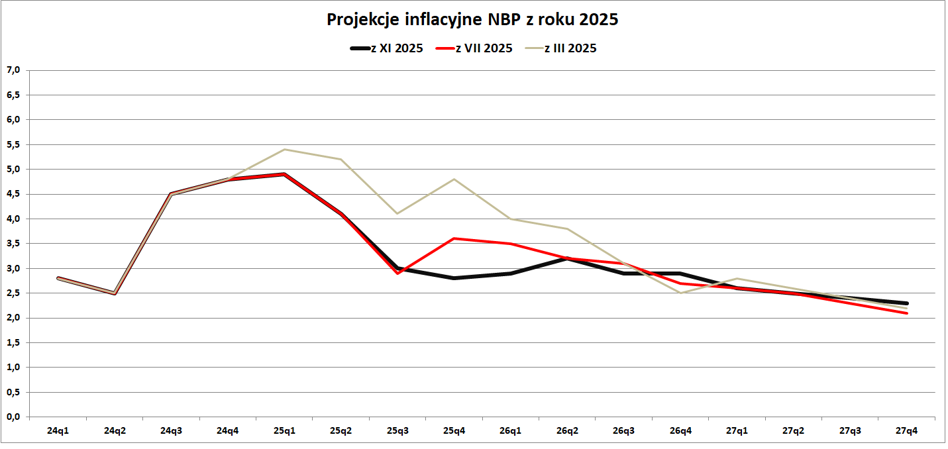

It is also worth comparing the November screening with its predecessors – especially its July edition. Since then, NBP rates have dropped by 100 basis points, current CPI inflation has dropped significantly (mainly due to the base effect in the context of energy and gas prices), crude oil has become cheaper and the annual growth rate of wages has decreased. Taking all this into account, I would point out that the November central path of CPI inflation is slightly higher than the July path. The differences are not excessively large (of the order of 0.1-0.2 percentage points), but they suggest the so-called function of the reaction of the majority of members of the Monetary Policy Council.

Theoretically, they should take into account primarily core inflation. This is because it is considered to be a derivative primarily of the action of domestic factors, which is influenced by monetary policy. It is assumed here that the NBP cannot influence global prices of crude oil or food, which are of decisive importance for the prices of fuel and food products in Poland. In this context, we see that subsequent NBP projections this year indicated that core inflation falls to the 2.5% target only at the very end of the time horizon.

And this was enough for the Council to cut the NBP interest rates quite sharply, thus extending the path to achieving its statutory goal. If a majority in the Council actually wanted to reach the 2.5% target as quickly as possible, it would not have voted for lower interest rates. Or at least it would lower them much slower than actually happened. After all, according to “the latest economic knowledge”, each reduction in rates by the central bank means – ceteris paribus – higher inflation in the future than in the scenario in which the rates were not reduced. In fact, this is the principle on which Enbep's NECMOD model works.

It therefore seems that the current majority in the Council, led by President Glapiński, is satisfied with CPI inflation remaining within the permissible deviation from the 2.5% target. To paraphrase the pirate captain from “Pirates of the Caribbean”: the goal here is only a guide rather than a binding rule. This leads us to the conclusion that the actual NBP inflation target is now 3.0-3.5%, not the officially declared 2.5%.

This is important information for all investors and savers, who should recalibrate all their spreadsheets and change the assumptions regarding expected inflation (i.e. if they still have inflation of 2.5% per year entered there). Moreover, the assumption of future CPI inflation at an average annual level of 3.5% would be consistent with the historical achievements of the National Bank of Poland in this field. Let us recall that the average (geometric) CPI inflation in Poland in the previous 20 years was 3.35%.