The Monetary Policy Council is cutting interest rates, but the yields on 10-year bonds have barely budged

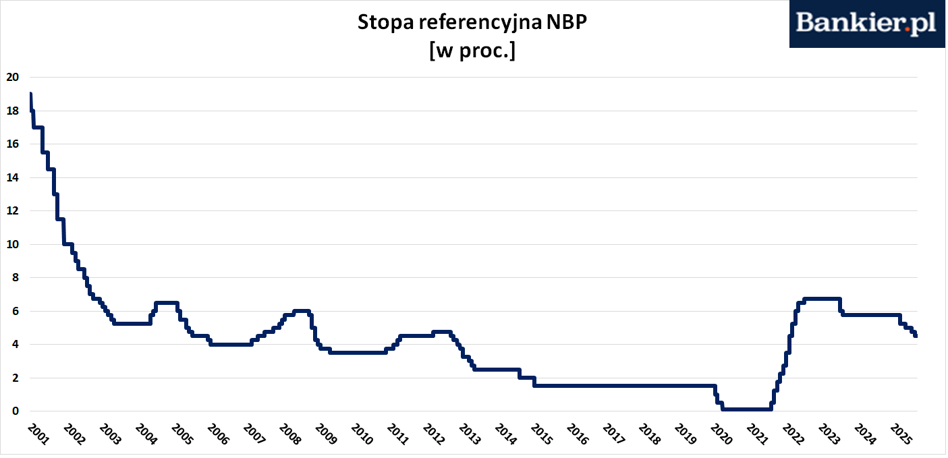

We have already had four interest rate cuts at the National Bank of Poland. Meanwhile, the yields of Polish long-term treasury bonds have barely budged and remain at levels similar to what we observed a year or two ago.

Three weeks ago, the Monetary Policy Council reduced interest rates by 25 basis points, in the case of the NBP reference rate, reducing it to 4.50%. This was the fourth reduction in a row, bringing the cost of borrowing from the central bank to the lowest level since May 2022. But first, in May, the Council cut interest rates immediately by 50 bps, in July it added -25 bps, and in September another -25 bps. Therefore, in total, over the previous six months, NBP rates were reduced by 125 basis points.

And it probably won't end there. Economists assume a 25-point cut at the November MPC meeting. In December, the Council traditionally does not change interest rates, but it will probably reduce them in 2026, although probably much slower than this year. The market consensus assumes reducing the NBP reference rate to 3.50%. As a result, short-term interest rates in Poland would be at their lowest level since spring 2022.

The short end down and the long end to the side

Each such rate reduction by the Monetary Policy Council brings joy to debtors with debts based on a variable interest rate. This group mainly includes “old” housing loans and business loans. At the same time, this is bad news for savers, who will receive lower interest on deposits or floating-coupon bonds. But the Minister of Finance should be most happy, for whom lower rates at the NBP mean – ceteris paribus – lower costs of servicing the rapidly growing public debt. However, the government does not borrow money from the National Bank of Poland (because it is prohibited by the Constitution of the Republic of Poland from doing so), but on the financial market by issuing treasury bonds.

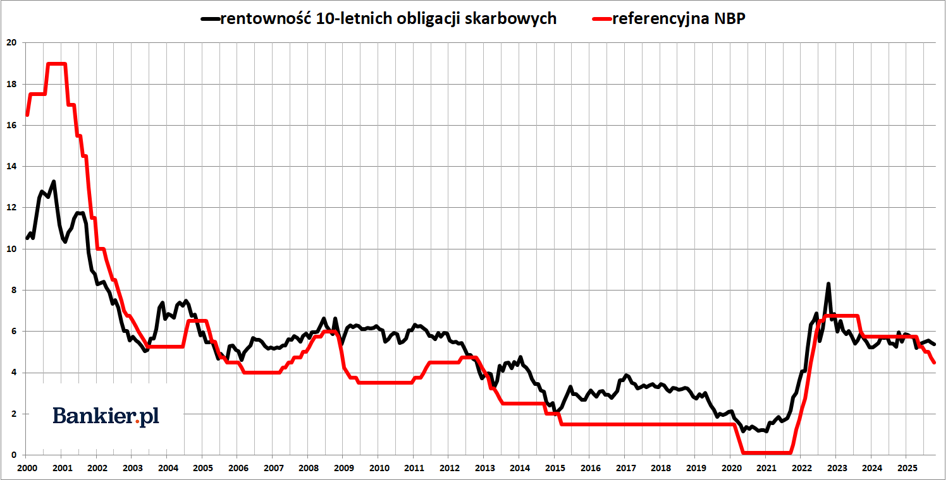

And here there is a problem. While the yields of short-term treasury bonds (e.g. two-year ones) follow the rates at the National Bank of Poland, long-term securities seem to have a life of their own. For example, the yield of Polish 2-year bonds is currently 4.13% (i.e. even lower than the current NBP reference rate), while in March it reached 5.50%. Therefore, in this “short” section of the term curve, the Ministry of Finance felt a significant relief, being able to issue new debt of almost 1.5 percentage points. percent cheaper than a few months ago.

However, the further back in time, the worse it gets. In the case of 5-year securities, the yield decreased from 5.70% to 4.76%. The same applies to 6-year bonds. But now Long-term bonds turned out to be almost completely insensitive to the Monetary Policy Council's decisions. The yield on Polish 10-year bonds is currently 5.37%. This is practically the same as in May or July, when NBP rates were significantly higher. In fact, it's only by 60 bp. less than in March, when the market did not yet know that the Council would cut short-term rates so sharply.

Looking over a longer time horizon, we see that from the spring of 2023, the profitability of Polish 10-year bonds fluctuates in the range of 5.00-6.00%. And that regardless of the current rates at the National Bank of Poland. This is not the first such case in history. Long-term market interest rates did not follow the decisions of the Monetary Policy Council in 2006, 2009-11 or 2013. Yes, a certain convergence of 10-year yields and short-term rates set by the NBP is usually noticeable, but it is not the rule.

What does the debt market want to tell us?

While the level of short-term rates at the NBP depends only on the whim of the members of the Monetary Policy Council, long-term rates (usually identified with the yield of 10-year bonds) are determined by the market. This means mainly domestic and foreign institutional investors: banks, investment and pension funds, insurance companies, etc. The market is guided by several factors here.

Firstly, the amount of expected inflation in the long term. And this is where Poland as a country has failed in recent years. For only 4 of the previous 71 months, CPI inflation was within the NBP's 2.5% target, which was permanently exceeded, both in the medium and long term. The average (geometric) CPI inflation for the last 5 years was 7.48%, for 10 years it was 4.48%, and for 20 years it was 3.35%. Therefore, debt market participants have the right to expect permanently increased CPI inflation (e.g. around 3-4%) also in the coming years.

Secondly, there is this risk of lending to the Polish government in the longer term. It has been common knowledge for over two years that the condition of Poland's public finances is in a terrible condition. Annual fiscal deficits exceed 6% of GDP for the third year in a row, and public debt is now reaching the constitutional limit of 60% of GDP. Then by 2030 it is expected to increase to 75% of GDP. Along with debt, the risk of a public finance crisis also increases and investors must include this premium in bond valuations.

Thirdly, in 2020, definitely the era of non-positive interest rates in the world has ended. In the previous decade, global capital was looking for any securities that would generate a fixed income at least close to the official CPI inflation. And now he has a choice. 10-year treasury bonds from issuers such as the US, UK and Norway pay 4% (or even more). Chilean securities, which are in the same basket as Polish securities, offer a 5.5% yield to maturity (YTM). So there is plenty to choose from. All the more so because governments are incurring massive debts and the supply of treasury bonds in the world is huge.

What can an individual investor do?

From the point of view of a Polish individual investor, this situation offers several options. If you think that we are facing an inevitable public finance crisis, get out of the domestic debt market and replace Polish “treasury bonds” with British securities (although it is not very cheerful there either), American or even Indian (currently: 6.5% YTM). However, if you think that we will manage somehow, as usual, then the almost 5.4% profitability on Polish 10-year bonds does not look that bad. Maybe not as appealing as 9% three years ago, but still decent. Of course, we are talking about a direct and independent purchase of such a bond on the Catalyst market, and not about investing in a bond fund or ETF (because this is exposure to a completely different risk profile).

Secondly, despite consistently reduced coupons in the retail treasury bond offer, we can still get a fixed 4.90% in the case of 3-year securities. It is true that this is much less than a year or two ago (by one and two percentage points, respectively), but it is probably significantly more than bank deposits will offer in the same period.

Thirdly, CPI inflation-indexed bonds offered by the Ministry of Finance are still in play. What I mean here is not only the recently unpopular “anti-inflation” retail bonds (4-year COI and 10-year EDO), but also the IZ0836 securities available on the Catalyst market. In both cases, we cannot count on a repeat of the bond Eldorado of 2022-23, but we have a good chance of beating the official CPI inflation.

To sum up, the detachment of the yield of Polish 10-year bonds from the NBP rates does not have to be excessively disturbing information. However, it is worth checking this market from time to time and seeing whether the yield of 10-year bonds will not start to increase despite the NBP rate cuts. Moreover, the Treasury debt market still offers decent rates of return for patient and long-term investors.