Despite the next interest rate discounts at the Bank of England, the profitability of British 30-year bonds reached the levels of urged since the 20th century. It is a signal that investors require a higher bonus for financing the development of public debt of Great Britain.

On Wednesday, September 3, The profitability of 30-year government bonds of Great Britain reached 5.75% and was the highest since 1998. The downward trend on the market of these long -term guilt (i.e. bond prices are falling, and their profitability rises), although we have been observing since spring 2020, but in the last three years the amount of profitability required by investors is becoming unpleasant (at least for the rulers) high.

It is worth adding that a year ago 30-year-old debt papers of his royal government paid 4.4%. At the beginning of 2025 it was over 5%, in April over 5.5%. Now the market has influenced the waters, after which only the oldest investors sailed. For investors younger than 50-55 years they are never observed in their professional life.

When your feet fall, profitability should go down

The mere fact of an increase in the profitability of Gilts would not be so sensational, were it not for the fact that it takes place in the face of decreasing short -term interest rates at the Bank of England. In August, the British Central Bank cut the interest rate by 25 PB. up to 4%. What's more, it was the fifth reduction in the previous 12 months. And yet the profitability of long -term tax bonds is still going up!

This is not a normal situation. Usually, when the central bank lowers the feet at the “short” end of the term curve (i.e. short -term, usually weekly or two -week feet), they also decrease profitability at the longer ends of this curve. This happens especially in rich and developed countries, where usually no one has doubts about the solvency of the government (otherwise the situation is on “emerging markets”, where the authorities quite regularly bankrupt on foreign debt). But that such things would happen in the cradle of capitalism, which is Great Britain?

In this arrangement, the reason for this market behavior can only be one (theoretically two, but essentially boiling down to the same). Namely it is it Erosion of trust in the long -term stability of British public finances. Creditors are afraid that in the face of fatal fiscal parameters, the United Kingdom will serve them higher inflation and thus a faster decrease in the purchasing power of the pound of Szterling. To compensate for this, they demand a higher bonus for the risk of keeping British bonds. Especially those very long-term- 20- and 30 years old.

The Uk's Bond Market is collapsing:

Today, The Yield on A 30y Bond in the UK Rose to 5.64%, ITS HIGHEST LEVEL SINCE 1998.

Yields in the uk are now 15 times thanks they were at the 2020 low, just 5 years ago.

What is happening? Let us explain.

(a thread) pic.twitter.com/qmv5aagfx1

– The Kobeissi Letter (@Kobeissiletter) Seppember 1, 2025

Budget catastrophe of British finances

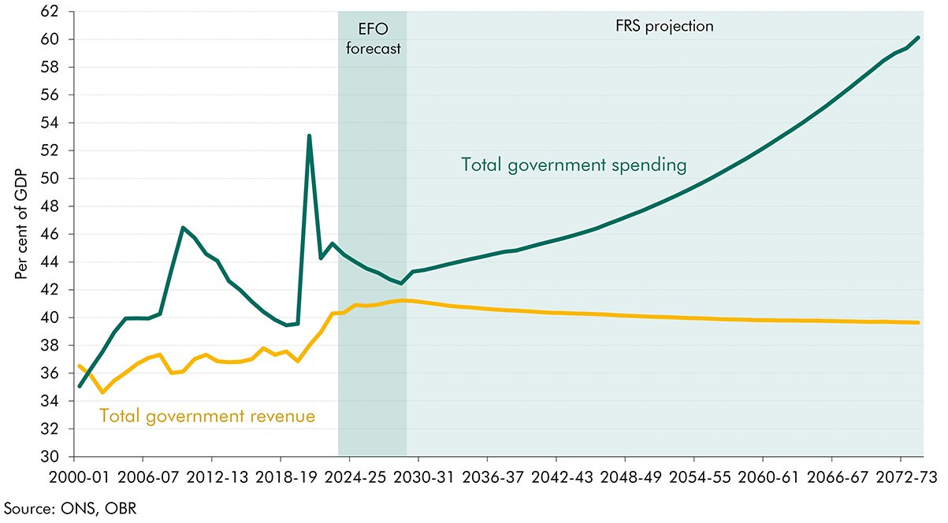

The United Kingdom is indebted at around 96% of its gross domestic product (GDP). Such a high ratio of debt to GDP has remained since 2020, when the British authorities at the time introduced one of the most authoritarian sanitary lockdown. Even worse, subsequent British governments are unable to stop the growing budget expenditure, which permanently exceeded the equivalent of 44% of GDP compared to 40% before the pandemic. As a result The United Kingdom of the Fifth Year in a row records a fiscal deficit close to 5% of GDP. And the market runs to the future, where even in the official forecasts of the government, public expenses grow near 60% of GDP with a relatively constant relationship of tax revenues to GDP. In debt at this pace, by 2073 British public debt would reach 274% of GDP.

Any attempts to change this state of affairs encounter the hard resistance of politicians governing the country. In July 2025, the world was circulated by the pictures of the treasury Chancellor Rachel Reeves. It happened when the leftist Premier Keir Starmer withdrew from support for the reform of social benefits proposed by Chancellor Reeves. Already then the debt market and the British pound reacted very negatively. Finally, can you imagine a greater fall of the former superpower?

The socialist authorities did not dare even an attempt to tame galloping social expenses, which should not surprise anyone. But he surprises that at the same time they are unable to raise taxes sufficiently. It is true that in this year's budget, the Labor Party proposed an increase in work taxes (formally paid by employers) and increasing the taxation of capital profits (up to 24%), but everything is not enough.

That is why labustists also proposed a draconian property tax increase, which would hit the already weakened British middle class. Yes, the same labustists who promised during the election campaign that under no circumstances would raise their hands to the finances of working people, excluding raising, among others social security contributions, income tax or VAT. However, there was no property tax there.

Not only Britain is financial in ruins

However, the fiscal crisis is only the tip of the Ice Mountain of British problems. The second economy of Europe is struggling with stagging. In the conditions of economic stagnation (real GDP is not much higher than it was three years ago) in the country at the same time inflation and unemployment grow. In July, CPI inflation accelerated to 3.8%, already nearly twice exceeding the inflationary of the Bank of England, which, despite this, fuels the decrease in the purchasing power of money, reducing interest rates. But at the same time, the unemployment rate increases, which rose to 4.7% and is the highest in 4 years.

Economic defeats can be seen not only in macroeconomic statistics. In the first half of 2025, the least cars were produced in Great Britain since 1953 (apart from 2020, when the government closed the factories as part of Covid's insanity). “This is not a crisis. It's the result” – this is how the immortal jelly would chop. The result of the crazy “climate policy” raising the price of energy, the growing social state discouraging from taking up work and the policy of accepting hundreds of thousands of migrants incompatible with the needs of a developed market economy. Native British are decreasing faster and faster, but in recent weeks they began to rebel against mass immigration.

However, Great Britain is not isolated in its financial, economic and demographic problems. Exactly the same – although for now less spectacular – is happening in the markets of long -term American, German or Japanese debt. While the Fed is preparing for subsequent interest rate discounts, the profitability of 30-year-old Treasuries reaches 5% and lasts close to the highest levels for several years. Therefore, also on the other side of the Atlantic, investors are afraid of permanently increased inflation, which is a consequence of huge public debt.

But in relative terms, the largest increase in profitability was recorded in Japan. There, 30-year-old samurai pay almost 3.3% profitability on the purchase time (YTD). This is the most in the history of these papers. For comparison, 5 years ago, the profitability of these papers was slightly higher than scratch. The same happens in the case of similar papers of the German government. 30 -year -old Bundy already pay 3.4% – the most in 14 years – although 5 years ago their profitability could be … negative.

The common denominator of the decrease in prices of long -term sovereign debts of the most reliable debtors on Earth is very high and rapidly growing public debt. The United States is indebted to the equivalent of 124% of GDP – the most in its post -war history. In China, the ratio of debt to GDP reaches 88%, in Japan it is an astronomical 237%, in Great Britain almost 96%, in France 113%, in Italy 135%, and in Canada 110%. Only Germans (62.5% of public debt GDP) look decent among the largest economies in the world, but the government has recently deleted fiscal brakes, which will result in a significant increase in debt.

Investors are increasingly asking two questions:

- Who will pay all this in 20-30 years in the face of a shrinking population in a working age?

- How much will the money be worth, which the rule will give us?

And it turns out that It will be much less than it seemed until recently. Hence, in the entire developed world we are observing an increase in the required profitability of long -term tax bonds. Perhaps we are witnessing the beginning of the sovereign debt and the collapse of the fiducinent currency system. At least this would be indicated by galloping gold and silver records, as well as record high valuations of the main cryptocurrencies.