publication

2025-06-18 20:00

update

2025-06-18 20:16

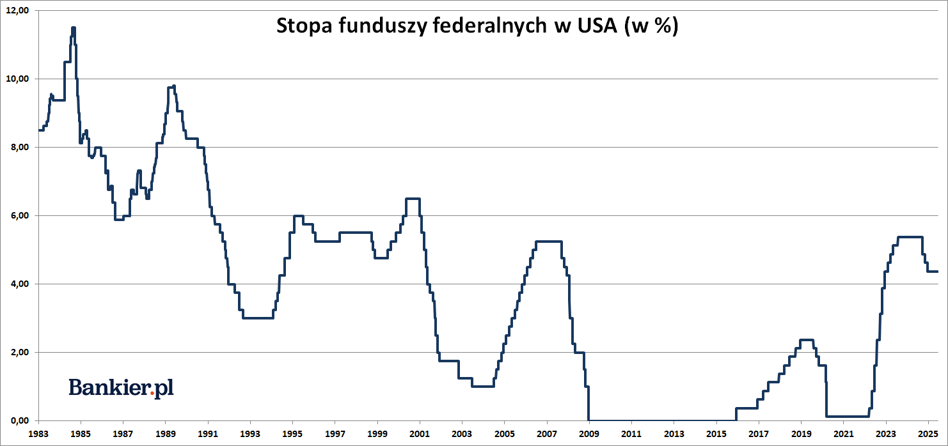

The management of the Federal Reserve did not bend under the pressure of President Donald Trump and again did not reduce interest rates despite the insistence of the head of the state. “Pause” in the cycle of interest rate reductions has been going on for half a year.

The range of federal funds remained unchanged at 4.25-4.50%

– the Federal Open Market Committee (FOMC) announced in the announcement. The June decision was made unanimously and was in line with the expectations of economists and market participants.

After the previous decision, a wave of criticism from President Donald Trump spilled into the management of the Federal Reserve. – Jerome Powell is an idiot who has no idea about anything (…) He is still late, but it doesn't matter much, because our country is strong – this is the May decision of the FOMC was commented by the Host of the White House. President Trump has already demanded further interest rate reduction from the Fed to reduce the costs of servicing the gigantic public debt of the USA.

– The committee is risky to both sides of its double mandate – This is a much milder and stripped version of the May warning against the influence of President Trump's customs policy on the US economy – Uncertainty about economic perspectives has slightly decreased, but is still increased

The committee reserved.

It is already half a year of “post -election” pause in monetary loosening

Half a year has passed since the last reduction of interest rates at the United States Central Bank. The monetary loosening cycle began in September 2024, a nervous and unjustified cut by 50 pb. This movement chairman Powell quite clumsy explained the “rectus” of monetary policy. Another reduction in federal funds – this time after 25 PB. Each – took place in October and November. The total scale of last year's reductions was therefore 100 PB. After the presidential election, the Fed Fed Fed no longer reduced.

– We do not have to hurry and we are well prepared to wait for greater clarity (regarding the policy of the Trump administration – editor's note) – said the head of the US central bank on March 7.

In addition, in March, Fomc did not change the level of interest rates, but decided to limit “quantitative strengthening” (QT) of monetary policy. Starting from April, the Federal Reserve limited the rate of reducing its balance sheet sum from USD 60 billion to USD 40 billion per month. This limitation of “quantitative strengthening” was therefore somewhat loosening monetary policy in the US.

Next cut only after the holidays?

In recent weeks, investors have limited their expectations for future interest rate reductions in Feda. Currently, the 68% termination market values the chances that at least a 25-point reduction in federal funds will take place at the latest during the September meeting of the FOMC-according to the Fedwatch Tool calculations. At the beginning of May, the chances of reduction in July were valued at 73%. Now its implied valuation is less than 15% chances.

However, by the end of 2025, “at prices” there are reduction of federal funds by a total of 50 pb. This is clearly less than barely six weeks ago, when the term market valued cuts of 75-100 PB.

– The Committee is strongly determined to support the full employment fine and bring inflation back to a 2 % goal- it was recalled in the May Federal Committee of the Open Market Square.

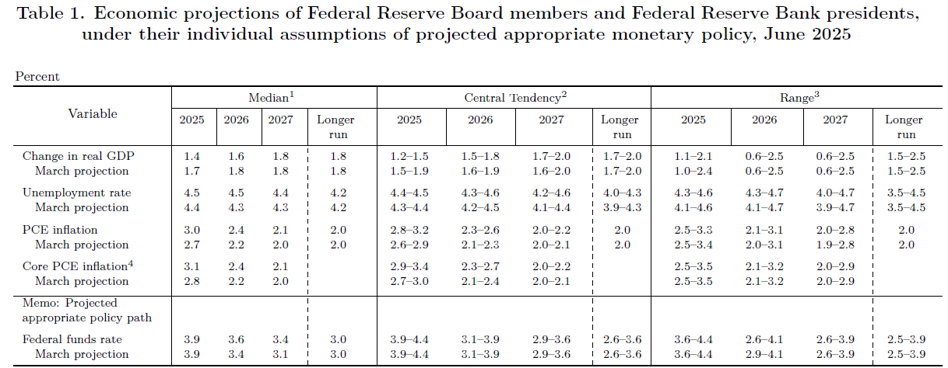

New project and “fedocrop”. Inflation up, GDP height down

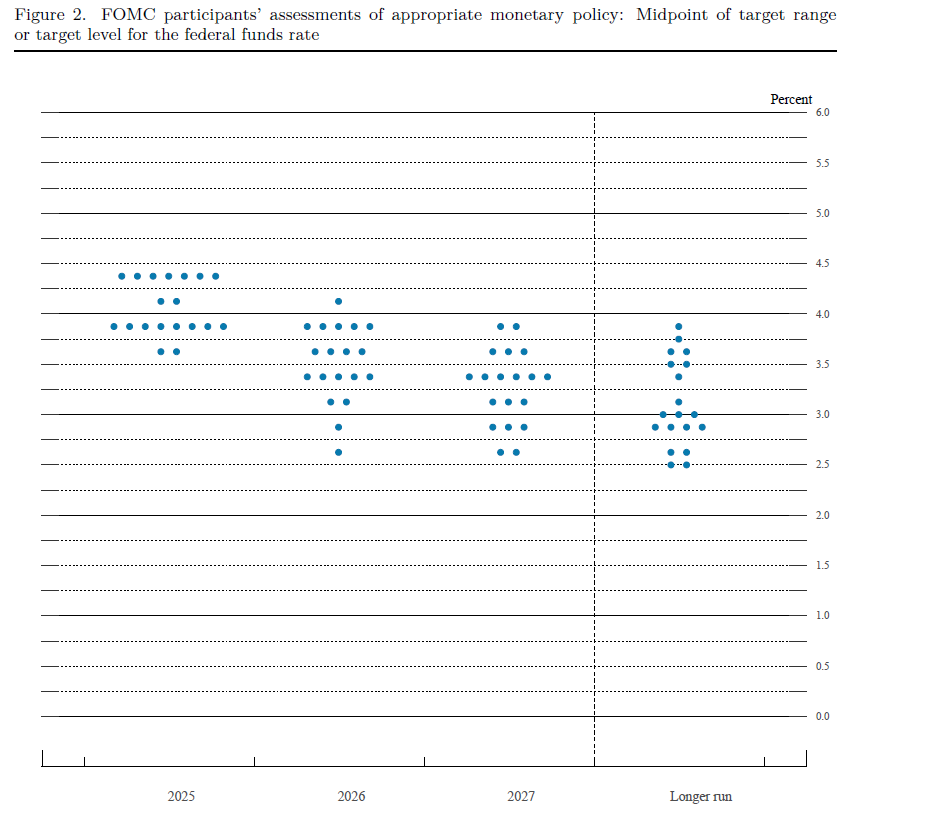

As every quarter, the members of the committee updated their macroeconomic projections. The most important conclusion of them is that Just like in March, there is a majority for only two 25-point reduction of federal funds by the end of 2025. But from 2026 one reduced foot reduced. Just like from 2027, at the end of which Fomc's majority would like to set foot at 3.4%.

Forecasts for the main US macroeconomic indicators have also deteriorated. In the June forecast, the median forecasts assume GDP growth in 2025 to 1.4% and 1.6% the following year. In March it was 1.7% and 1.7%, respectively. The forecasts of the base consumer expenditure deflator (PCE Core) went upwards: from 2.8% to 3.1% in 2025 and 2.4% and 2.2% in 2026, as well as from 2.0% to 2.1% in 2027. In this way in the entire horizon of the projection, the measure of inflation preferred by the Fed.

The next meeting of the Federal Open Market Committee is scheduled for July 29-30.