After a sharp May cutting of interest rates, the Monetary Policy Council can take a break and wait for the July inflation projection – analysts say. However, the possible June Pause does not cross the chances of continuing the series of loosening of monetary policy in Poland.

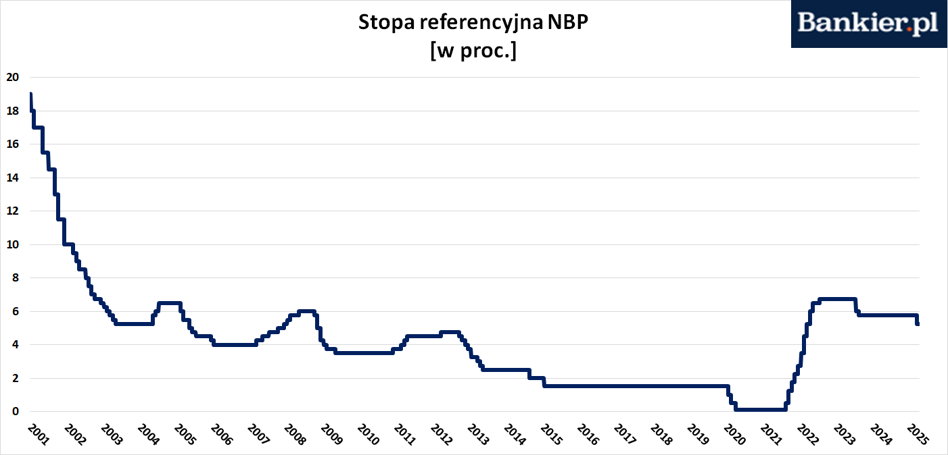

Most market economists assume that at the meeting starting on Tuesday, the Monetary Policy Council will keep interest rates at an unchanged level. In the case of the NBP reference foot, this would mean 5.75%.

A month ago, the council cut the feet with 50 base points. It was the first reduction of credit costs from October 2023 at the National Bank of Poland. NBP President Adam Glapiński described this decision as “adapting” the monetary policy to changed macroeconomic parameters.

– Adaptation does not automatically mean the beginning of the reduction cycle – said NBP president Adam Glapiński during the May press conference. He added that The MPC authorized him to say these words. – We do not exclude any scenarios, we do not announce any future interest rate path. The MPC will respond to data from the economy – noted the president of the NBP.

The cycle of reductions will start in the second half of the year?

Following the words of the chairman Glapiński, the market consensus supports the opinion that In June we will not see the change in interest rates in Poland. But already in July a cycle of regular credit cost reduction is to start. Discounts of 25 PB are expected. in July, September and November.

– We expect Pause in June and the MPC transition to a series of interest rate reductions in movements by 25 PB. In our opinion, the next foot reduction will take place in July, and the next in September and November. As a result, at the end of 2025, the reference rate should be 4.50 percent. – economists of Bank Śląski wrote in the commentary. – In 2026, we expect further foot cuts on a 75PB scale, up to 3.75 percent. at the end of next year – they added.

For the schedule of foot cuts at the NBP, the calendar is important. Over the past month, the Council has received too little information to decide on further cuts. On the other hand, an important change was the approval of the URE reduction of natural gas tariffs for households. According to economists, this decision will subtract 0.3 points. percent from CPI inflation for July.

In addition, in July, the council will receive a new inflation projection of analysts of the National Bank of Poland. This projection will probably show a clearly lower inflation path than the one presented in March. That did not give space to reduce interest rates. In August, in August, there is no way of a decision -making meeting. And another inflation projection will be published in November – hence the lack of expectations for cutting feet in October.

In addition, in July, the base effect associated with last year's gas tariffs, network heat and eclectic energy will expire. As a result, assuming the current, clearly lower than a year ago, fuel prices and weakening base inflation cannot be ruled out that CPI inflation will fall below 3%in the summer. In this way, it would finally be within the permissible deviation from the 2.5 % NBP target.

The economy in the shadow of politics

Looking only through the prism of data from the economy and inflation tendencies, there is a space in Poland to start a cycle of interest rates. The current value of the NBP reference rate (5.25%) by a good two percentage points exceeded CPI inflation forecasted in the horizon of the next few months. What's more, the July NBP projection can show the inflation descent up to 2.5% in 2026-that is, in the horizon of the impact of monetary policy (it is assumed that it is delayed in the broadcast to the real economy is 4-8 quarters).

Assuming that next year we will see CPI inflation close to 2.5%, the NBP reference rate could easily drop to 4.5% or even lower. It is assumed that the optimal real interest rate for Poland is in the range from 0% to 2%. At the same time, zero would mean a very loose monetary policy, and the value of 2% results from the old rules of its conduct (e.g. Taylor's rules).

However, the situation is complicated by the policy. Economists are visions of how Rafał Trzaskowski's election defeat complicates the plans of Donald Tusk's government. It is not just that the president has the right of veto and this way can effectively block the laws coming out of the government and supported by the current parliamentary majority. The thing is that the result of the presidential election was shown (especially in the first round) that most voters do not accept the policy of the current authorities.

And this raises the risk of failure in parliamentary elections, which, according to the schedule, should take place in the autumn of 2027 (unless the parliament and early elections are resolved). In this arrangement, the Tusk team can opt for an even more expansive fiscal policy to satisfy the social electorate.

– The results of the presidential election intensify the risk of turmoil on the Polish political scene, and high support for right -wing groups increases the likelihood of changing power in the next parliamentary elections in 2027. In such conditions, the current government may be reluctant to fiscal consolidation before the election – the economists of Bank Millennium assessed.

A detached fiscal deficit means pumping borrowed money directly into the economy, which is a pro -wing phenomenon. In such an environment, economic policy textbooks recommend sharper monetary policy. So that the central bank inhibit the economic madness of politicians. In Polish conditions, the case has a second bottom, because most of the members of the current monetary policy council were appointed by Law and Justice, and several of the MPP members are former politicians of this party. Therefore, they may be less willing to help the current government and not hurry to loosen the monetary policy.

Traditionally, we already know the day, but not an hour of publication of the MPC decision. It usually appears on Wednesday between 14:00 and 16:00. This second hour determines the planned moment of publishing the official message after the council meeting. But in the past it happened that he was not kept. In addition to the decision itself and its justification, the tons of the Thursday conference of President Glapiński will be very important.